CWS Market Review – June 18, 2024

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

The stock market closed at another all-time high today. This is the S&P 500’s 31st new high this year. The Nasdaq rose for its seventh day in a row.

The stock market also reached another milestone. Nvidia passed Microsoft to become the world’s most valuable public company. The chipmaker now has a valuation of $3.3 trillion. It’s larger than every company in the Russell 2000 combined.

Ten years ago, Nvidia was worth $10 billion. CEO Jensen Huang’s first job was as a busboy at Denny’s. Now he’s worth $117 billion. Not bad.

As I’ve mentioned many times before, this market has been heavily tilted toward growth stocks. In fact, today snapped an 11-day winning streak of the S&P 500 Growth ETF (SPYG) outpacing the S&P 500 ETF (SPY).

As strong as this market has been, it’s been very narrow. Despite being at a new high, only 50 stocks in the index touched 52-week highs today.

Soaring markets can be surprisingly tricky for investors. Watching share prices march steadily higher can induce intense fear in some investors. They tend to think that we must be getting near a cliff and that it would therefore be best to cash out now.

That’s a mistake. A rising market doesn’t necessarily mean we’re in a bubble. It only means that share prices are higher than where they were. Rallies can go on for longer than you think. Peter Lynch said, “Far more money has been lost by investors trying to anticipate corrections, than lost in the corrections themselves.”

A few years ago, I looked into the data and found that the stock market does very well when it’s at an all-time high. Not only that, but the market is significantly less volatile when it’s at a new high. It’s pretty rare that the market rallies by more than 1% in a day following an all-time high.

Where do we go from here? That’s hard to say but I’ll note that July has been up for the last nine years in a row.

Let’s look at the market’s current valuation.

The S&P 500 closed Monday at 5,473.23. Wall Street currently expects the S&P 500 to earn $240.78 per share this year. That gives the market a forward price/earnings ratio of 22.7.

That works out to an earnings yield of 4.40% (i.e., the inverse of the p/e ratio, it’s the e/p ratio). To get an idea of how expensive that is, we want to compare the S&P 500’s earnings yield with the current yield on the long-term Treasury bonds. The 10-year Treasury currently yields 4.22%.

In other words, investors are getting a very mild safety cushion of 20 basis points by being in Treasury bonds. That’s not much. The risk/reward balance still leans towards stocks.

There are some important caveats. The market’s forecast for earnings this year is just that, a forecast. Wall Street analysts have often been wrong, and sometimes by a lot. Wall Street has already lowered its earnings forecast for this year, and it can do it some more.

We also don’t know where interest rates will go. If inflation comes back, that would send yields soaring. It was only eight months ago that the 10-year Treasury was yielding close to 5%. Right now, the bigger fear is that the economy will turn south.

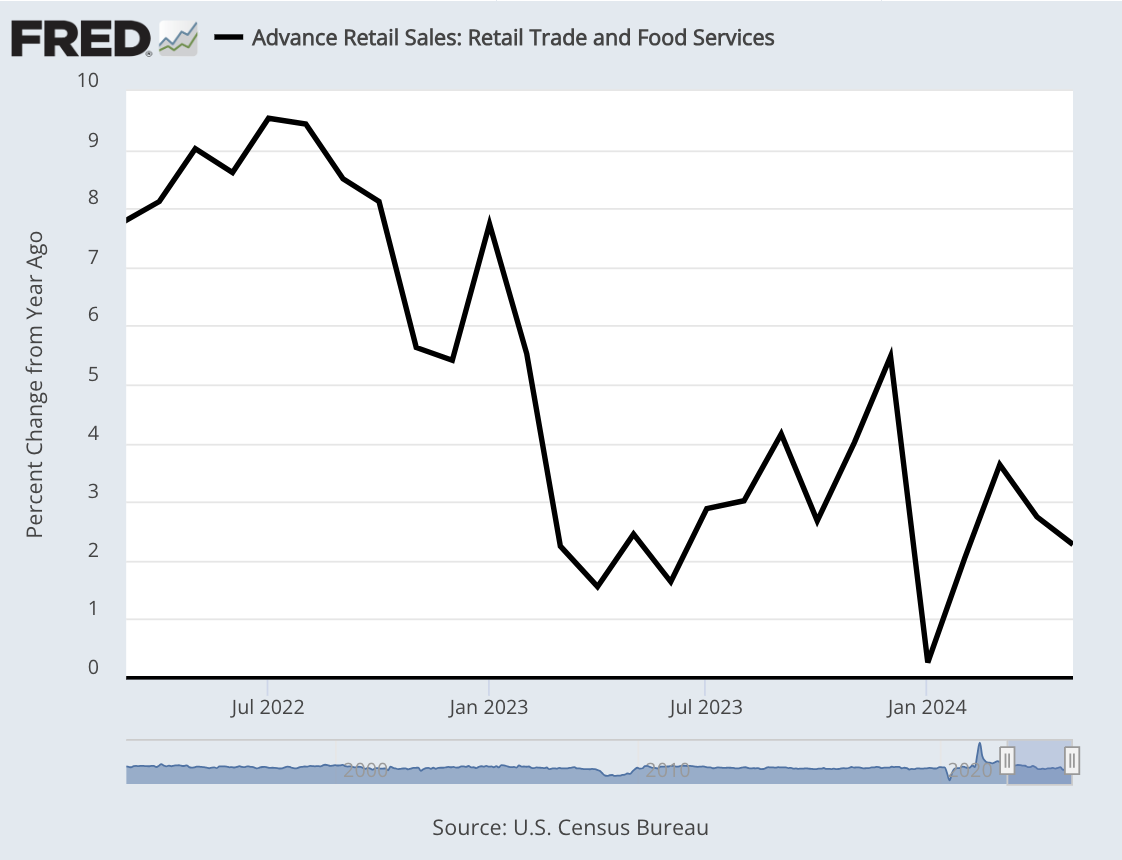

Retail Sales Were Weak Last Month

Americans haven’t been shopping as briskly as expected, which is odd since you might think that shopping was our national pastime.

To be fair, this morning’s retail sales report was only a little weaker than expected. Last month, retail sales rose by 0.1% which was 0.1% below expectations. Over the last year, retail sales are up by 2.3%. That’s not adjusted for inflation. The number for April was revised to a decline of 0.2%.

Here’s the year-over-year growth in retail sales:

If we don’t exclude autos, then retail sales for May fell by 0.1% whereas Wall Street had been expecting an increase of 0.2%. So what caused the sluggish shopping numbers?

Moderating gas prices helped hurt receipts at gas stations, which reported a 2.2% monthly decline. That was offset somewhat by a 2.8% increase at sports goods, music and book stores.

Online outlets reported a 0.8% increase, while bars and restaurants saw a 0.4% decline. Furniture and home furnishing stores also reported a 1.1% drop.

The retail sales report is important because consumer spending makes up about 70% of the economy. The good inflation news has come at the same time that consumer spending has apparently weakened.

Following the report, the odds of a September rate cut edged up from 61.5% yesterday to 67% today. Futures traders think there’s a 66% chance that the Fed will cut rates twice this year.

The most troubling news today came from the Congressional Budget Office. The CBO increased its estimate for the U.S. budget deficit by 27% to nearly $2 trillion. The new estimate is $400 billion higher than the previous estimate in March. Last year, the deficit was $1.69 trillion. For this year, the CBO sees it reaching $1.92 trillion.

As a percent of GDP, the CBO sees the deficit getting to 6.7%. That’s up from the prior estimates of 5.3%. Last year’s deficit was 6.3% of GDP.

According to Bloomberg, “Over the coming decade, the CBO sees US deficits totalling $22.1 trillion, up more than $2 trillion from February’s report.”

The CBO listed four major reasons for the budget revisions: President Biden’s student loan forgiveness plans, aid to Ukraine, Israel and Taiwan, FDIC payments for bank failures and heightened Medicaid spending. What’s frustrating is that the CBO sees higher revenues incoming but not enough to offset the higher spending.

If world markets become convinced that the U.S. is too much of a risk to invest in, that would hit the dollar and our ability to borrow money. So far, the market doesn’t seem too concerned. I don’t know how long that can last.

Stock Focus: Nathan’s Famous

With July 4th coming up, I wanted to highlight one of my favorite unfollowed stocks which is Nathan’s Famous (NATH), the hotdog stand.

Not many people realize that the Coney Island mainstay is publicly traded, but it is. Not only is Nathan’s listed on the exchange, but it’s been a great stock for decades.

Nathan’s is currently priced at $67.65 per share. That’s not a bad valuation. Nathan’s Enterprise Value/EBITDA is currently 9.73 which isn’t bad.

The company has a market value of $282 million. Last week, Nathan’s reported earnings for fiscal 2024 of $4.81 per share. That was up by one penny per share from one year before. Sales growth is low but positive.

Currently not a single analyst follows Nathan’s. Since December 31, 1999, Nathan’s is up 3,846% while the S&P 500 is up 493%.

That’s all for now. The stock market is closed tomorrow for Juneteenth. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on June 18th, 2024 at 6:25 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His