CWS Market Review – July 2, 2024

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Wall Street Wraps Up an Historic First Half

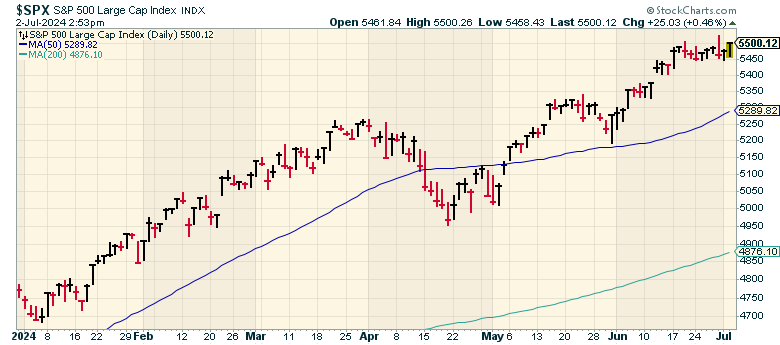

On Friday, the stock market closed out a very good June along with a very good first half of 2024. The S&P 500 gained 14.48% for the first half of this year. Including dividends, the index was up 15.29%. This makes 2024 one of the best starts to an election year in the last century.

The S&P 500 closed today at another all-time high.

Historically, this has been a good time for stocks. From June 27 to July 17, the S&P 500 has gained an average of 1.97%. That’s a good amount for an average of 70 years.

The market was up again yesterday. The stock market has a nice habit of starting out the second half of the year on a good note. Here’s a remarkable stat via Ryan Detrick: the S&P 500 has been higher on the first trading day of July for 14 years in a row, and for 18 out of the last 19. I should also remind you that that the S&P 500 still hasn’t posted a daily drop of more than 0.75% since April.

As I’ve mentioned many times, this year has been a tale of two markets. Growth stocks have done very well, but value stocks are only up modestly. For the first half of this year, the S&P 500 Growth ETF (SPYG) gained 23.54% while the S&P 500 Value ETF (SPYV) was up 5.69%.

Monday’s trading saw another wide gap between growth and value. Alas, what’s been going on is still happening, only more so.

I don’t want to give the impression that value stocks have done poorly. Quite the opposite. Value has done well in historical terms. The problem is that a small number of stocks have distorted the whole market. If we were to take Nvidia out of the S&P 500, then the index would still be up close to 11% this year. If we were to exclude the entire Mag 7, then the S&P 500 would be up 6% this year. On average, that’s not bad.

The Rate Cuts That Never Came

The important point to understand is that the driver of this two-tiered market is interest rates. Or, to be more specific, it’s the interest rate cuts that never came. A little over a year ago, in May 2023, the yield on the two-year Treasury fell to 3.75%. That’s a good indication of how widely rate cuts were expected. Well, they never came. Instead, the two-year currently yields about 4.7%.

Years from now, investors will look at a chart of interest rates for the last year and wonder what the big deal was. Nothing changed! We’ve nearly gone a full year without any changes to interest rates. While this is superficially accurate, it eludes the fact that nearly everyone thought the Fed would be madly cutting by now. Instead, it hasn’t done any.

The reason that interest rates haven’t changed is that inflation is still a problem. True, inflation is not as severe as it was two years ago, but inflation is still above the Federal Reserve’s target.

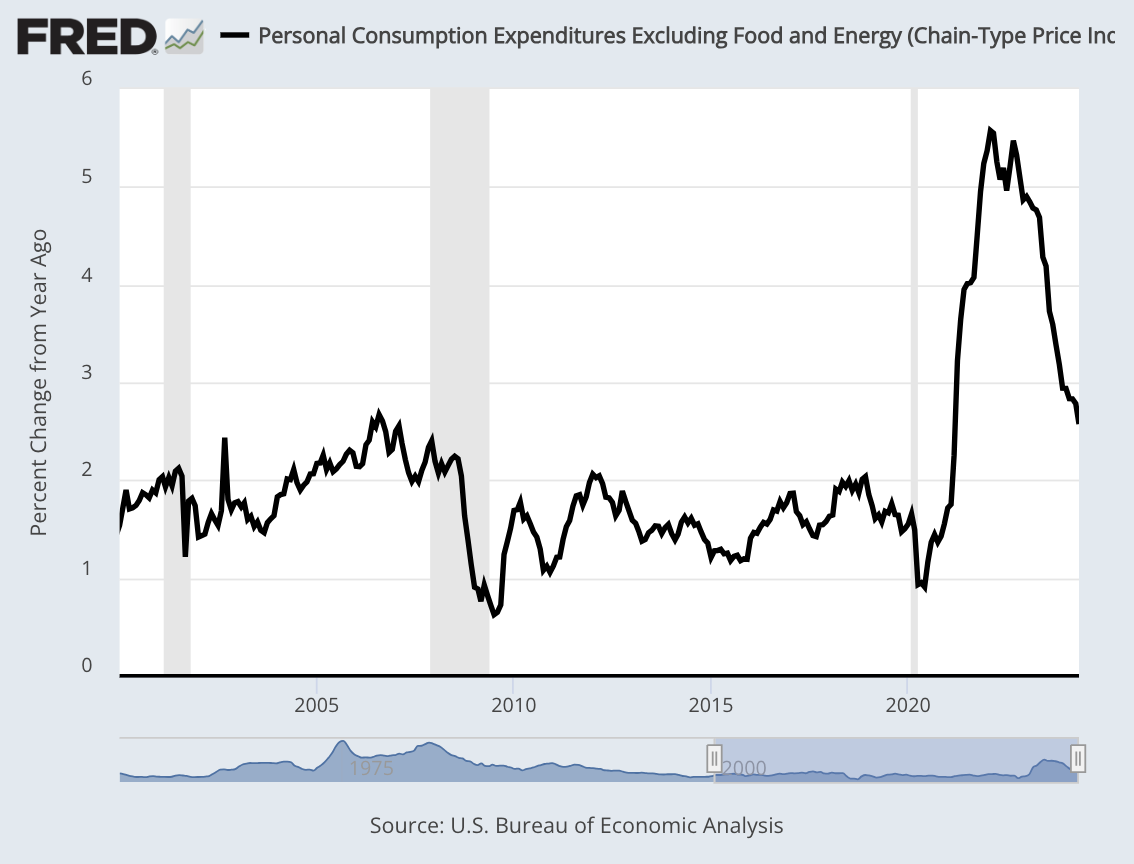

On Friday, the Commerce Department said that the Core PCE Price Index rose by just 0.1% last month. This is an important number to watch because it’s the Federal Reserve’s preferred measure of inflation. The reason to favor the PCE is that it’s a “broader inflation measure and accounts for changes in consumer behavior, such as substituting their purchases when prices rise.”

Over the past year, the Core PCE Price Index is up by 2.6%. That’s the lowest year-over-year rate in three years. The non-core rate, which includes food and energy, was flat last month. Both numbers matched Wall Street’s expectations.

The good inflation news hasn’t gone unnoticed. Earlier today, Federal Reserve Chair Jay Powell said he’s encouraged by the inflation numbers, but he wants to see more evidence that inflation is under control before the Fed acts.

Powell said that the last two inflation reports “suggest that we are getting back on a disinflationary path.” That’s unusually optimistic language from a Fed chair. Bear in mind, central bankers are paid to look dour and concerned.

Powell was asked if the Fed is going to raise rates in September. He elegantly sidestepped the question, but he said the Fed will be focused on more data. The Fed meets again at the end of this month, and you can forget about any rate hikes, but there’s a good chance we’ll see one in September. Futures traders currently think there’s a 70% chance that the Fed will cut in September. They see two cuts before the end of this year.

Manufacturing Has Declined 19 Out of 20 Months

Ideally the Fed can raise interest rates without damaging the economy. However, the evidence suggests that won’t happen. We’re getting some small signs that the economy may be getting stretched thin. I don’t want to overstate this, but there are some concerning signs.

On Monday, for example, the latest ISM Manufacturing Index said that the factory sector of the economy contracted. For June, the ISM Manufacturing Index was 48.5 which is down a tad from 48.7 in May.

From Reuters:

Manufacturing is being pressured by higher interest rates and softening demand for goods, though business investment has largely held up.

“We expect the manufacturing sector to remain weak over the next couple of quarters,” said Oliver Allen, senior U.S. economist at Pantheon Macroeconomics. “The retreat in corporate bond yields since late last year … seems to have provided some support to investment spending, but not enough to get manufacturing growing again. A much more significant loosening in financial conditions is required to change that.”

The ISM Manufacturing Index has been below 50, meaning it’s contracting, 19 times in the last 20 months.

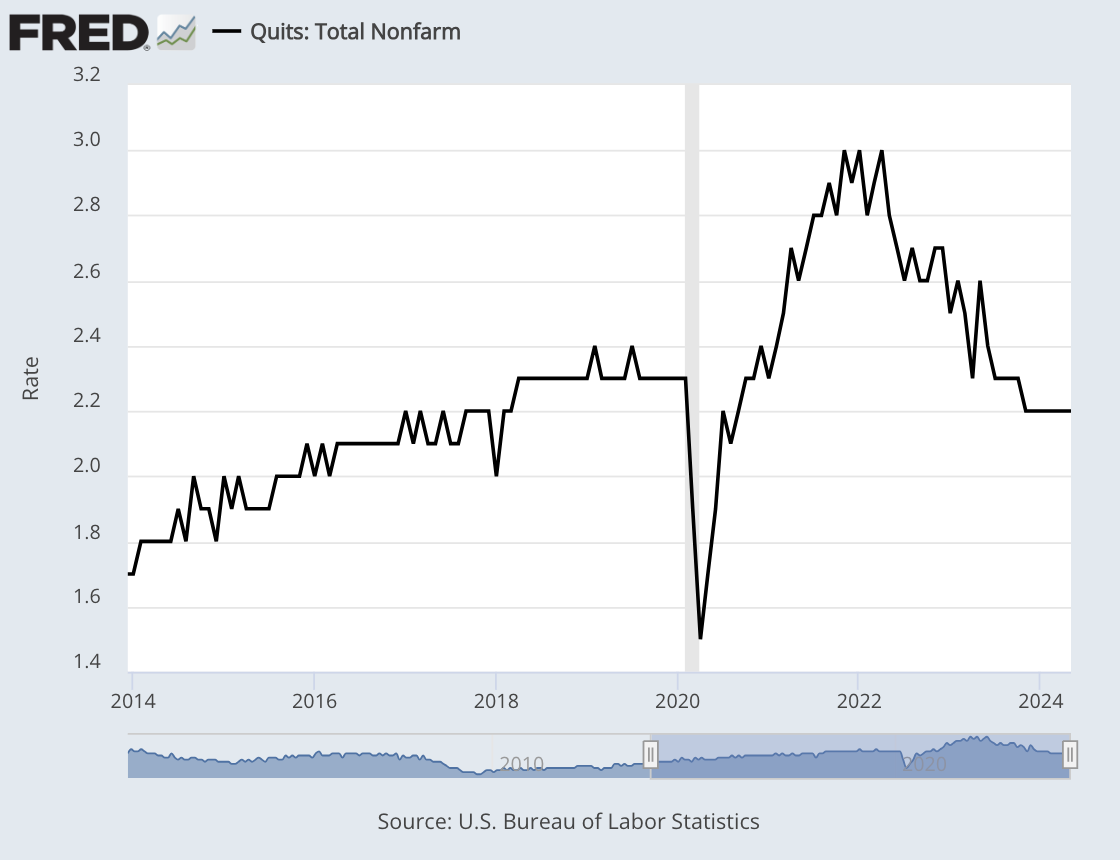

We’re also seeing some signs of weakness in the labor market. For example, the number of job openings per each unemployed person has fallen sharply over the past few months. Tuesday’s JOLTS report showed 1.2 job openings for each unemployed person. Two years ago, the ratio peaked at 2.0. Also, the “quick rate” has fallen. That suggests that workers are less optimistic that they can easily find a new job.

The next big test for the market will come this Friday when the government releases the June jobs report. Wall Street is cautious. The consensus is that the economy added 200,000 net new jobs last month and that the unemployment rate stayed at 4%.

Stock Focus: Constellation Software

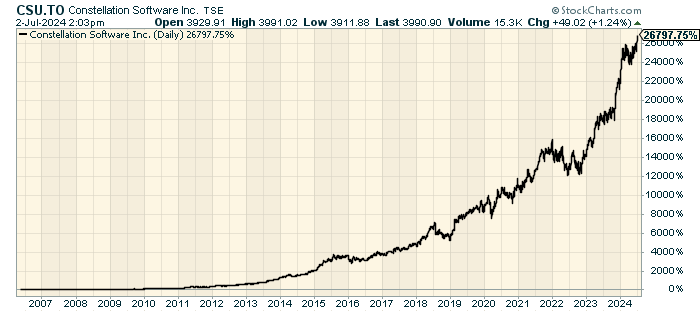

Yesterday was Canada Day so in honor of our friends in the north, I wanted to feature a Canadian stock this week that’s not well-known south of the border. The company is Constellation Software (CSU.TO) of Toronto. The ticker symbol is CSU, and it trades on the Toronto Stock Exchange.

Officially, Constellation Software describes itself as a diversified software company, and that’s accurate, but the company is also like a publicly-traded venture capital firm that buys up smaller software companies. It’s hard to find a company that’s grown that consistently for that long.

Most of Constellation’s purchases are small. Since the company was founded 30 years ago, it’s bought up more than 500 companies. I can’t think of a company that’s been such an astute investor.

Constellation had its IPO in 2006, and it’s been a big success since then. Since then, the stock has gained 26,800%.

Constellation is run by Mark Leonard who prefers to keep a low profile—a very low profile. Outside of his shareholder letters, there’s not much info on him.

What we do know is that Leonard tries to keep Constellation very decentralized. He prefers to have small business units. The company aims to buy niche businesses and it owns them for a long time.

Leonard is a fan of Illinois Tool Works (ITW) because that company has been able break down larger acquisitions into smaller business units.

Constellation is currently followed by five analysts. For 2025, the consensus expects Constellation to earn $136.89CDN per share. That means the shares are going for 29 times earnings.

That’s all for now. The stock market will be closed at 1 p.m. ET on July 3, and it will be closed all day on July 4 for Independence Day. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on July 2nd, 2024 at 5:51 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His