CWS Market Review – July 30, 2024

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Q2 Earnings Are Still Looking Good

We’re getting to the heart of Q2 earnings season and so far, the results are pretty good. I would have expected to see more damage from elevated interest rates, but Corporate America seems to have weathered the threat fairly well.

According to numbers from FactSet, 41% of companies in the S&P 500 have reported so far. Of those, 78% have beaten their earnings estimates – that’s very high – and 60% have topped their revenue estimates.

FactSet said we’re currently tracking earnings growth for Q2 at 9.8%. If that’s right, it will be the best quarter for earnings growth since Q4 2021. That’s a lot better than was expected. On June 30, Wall Street had been expecting earnings growth of 8.9%.

Here’s a look at the S&P 500 (black line, left scale) along with it earnings (blue line, right scale). The two lines are a scale ratio of 18 to 1 so whenever the lines cross, The P/E ratio is exactly 18.

The net profit margin for companies is 12.1% which is high by historic standards. Interestingly, Wall Street expects margins to go even higher. Analysts see margins of 12.4% for Q3 and Q4.

I’ve also looked to see if there’s any trend in guidance. As of now, guidance is perfectly even. For Q3, 16 companies have issued positive EPS guidance, and 16 have issued negative guidance. Overall, stronger earnings can support higher share prices. Also, lower interest rates can give a boost to valuations. This is the one-two punch that the market needs.

The stock market had a brief misstep recently when it fell six times in seven trading sessions. The S&P 500 even dropped below its 50-day moving average, which is often an omen of bearish sentiment.

Are we out of the woods? I’m afraid it’s too early to say. The S&P 500 was up very modestly on Friday and Monday, and it was down again today. The big story on Wall Street is the summer rotation, and it’s still unfolding. The plot is easy. Investors are fleeing large-cap tech stocks and seeking safety in smaller value stocks. Microsoft will report earnings after today’s close while Amazon, Facebook and Apple are due to report later this week.

Today’s trading was another example of the rotation. The Nasdaq was down over 1% today while the Russell 2000 Small-Cap Index was up.

It’s hard to convey how dramatic this turn has been. All those big-name tech stocks have gotten battered. Nvidia is now 26% below its 52-week high. That’s a loss of $900 billion in a little over one month. Meanwhile, those overlooked small names are doing quite well. This has been an especially good time for our Buy List, and CWS.

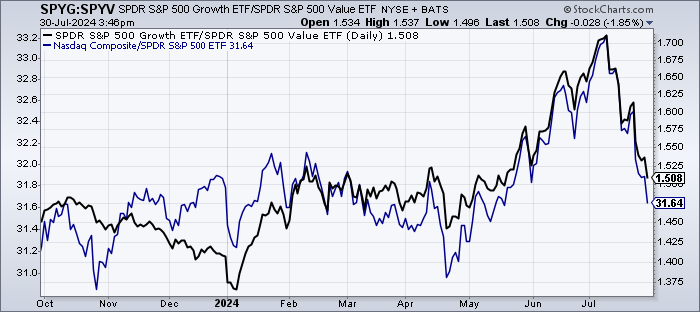

There are several ways to show the rotation on a chart. They all basically illuminate the same phenomenon.

In this chart, I have the S&P 500 Growth ETF divided by the S&P 500 Value ETF (black). The other line is the Nasdaq Composite divided by the Russell 2000 (blue). Notice how the two lines went from a low correlation to a very high one.

Don’t Expect Any Changes Tomorrow from the Fed

Last Thursday, the government released its first estimate for Q2 GDP growth. I have to confess that my expectations were way off. I thought the U.S. economy had grown in real annualized terms of about 1%, maybe a little higher. Instead, the economy grew by 2.8% for Q2.

To be fair, I wasn’t alone. The consensus on Wall Street had been for growth of 2.1%. The economy did a lot better than it did during Q1 when it grew by 1.4%.

Digging into the details, this was a solid report.

Personal consumption expenditures, the main proxy in the Bureau of Economic Analysis report for consumer activity, increased 2.3% for the quarter, up from the 1.5% acceleration in Q1. Both services and goods spending saw solid increases for the quarter.

Inventories also were a significant contributor, adding 0.82 percentage point to the total gain. Government spending added a tailwind as well, rising 3.9% at the federal level, including a 5.2% surge in defense outlays.

On the downside, imports, which subtract from GDP, jumped 6.9%, the biggest quarterly rise since Q1 of 2022. Exports were up just 2%.

On Friday, the government released the PCE price data for June. This data is important to keep an eye on because it’s the Fed’s preferred measure of inflation.

For June, the headline price index rose by 0.1% which matched expectations. Over the last year, headline PCE is up by 2.5%. That’s still above the Fed’s target of 2%, but it’s getting close.

We also want to look at the core PCE which excludes volatile food and energy prices. For June, the core PCE was up by 0.2% which also matched expectations. Over the last year, core PCE is up by 2.6. Again, it’s above the Fed’s preference but it’s a lot better than where it was two years ago.

The Federal Reserve started its two-day meeting today. The central bank’s policy statement will be released tomorrow afternoon at 2 p.m. ET. I’ll break the suspense: the Fed won’t make any changes to interest rates at this meeting, but this will be the last time. We can almost certainly expect the Fed to cut rates at its September meeting.

Wall Street currently thinks there’s a 4% chance of a rate cut tomorrow, but there’s an 85% chance of a 0.25% rate cut in September, and a 13% chance of a 0.50% cut. I doubt the Fed will give us a 0.50% cut, but it’s not unthinkable. Traders currently expect two more rate cuts before the end of the year.

I’m skeptical of looking at data that goes too far out, but futures traders expect the Fed to cut three more times in the first half of 2025. They may or may not be right, but it’s the change in interest rate expectations that’s driving the big rotation.

The labor market is mostly healthy for now, but I’m not sure how long that can last. As the New York Times noted, “Job openings have come down sharply, part-time employment is up, fewer companies are turning to temporary help to fill gaps and fewer workers are job hopping.”

I’ll also point out that historically, this has been a good time to be in the market. From July 28 of an election year until the end of the year, the Dow has gained an average of 10.07%. Citigroup said that stocks and bonds have generally done well around Fed meetings.

Stock Focus: Flowers Foods (FLO)

Many of the stocks I tell you about aren’t widely followed on Wall Street. This week, we’ll look at Flowers Foods (FLO) which does have some coverage. I see that eight Wall Street analysts follow the stock.

Flowers makes a wide range of packaged bakery products including “fresh breads, buns, rolls, snack items, bagels, English muffins, and tortillas, as well as frozen breads and rolls under the Nature’s Own, Dave’s Killer Bread, Wonder, Canyon Bakehouse, Mrs. Freshley’s, and Tastykake brand names.”

Flowers is a good example of a defensive stock. It’s been a wonderful stock for decades. Since October 1990, the stock is up 12,000%. Would you have guessed that Flowers Food outperformed Intel over that time? I wouldn’t have.

Flowers’s next earnings report will probably be in about three weeks. I’d stay away from the stock right now, but if there are signs that the business is improving, then Flowers could be a very good buy.

There could be an opportunity for shareholders. Flowers hasn’t done well lately, and it missed its last two earnings reports. The company announced plans to shut down a bun-making plant. Last month, the board increased the quarterly dividend by one penny to 24 cents per share. The shares currently yield a little over 4%.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on July 30th, 2024 at 9:31 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His