CWS Market Review – August 20, 2024

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

“All money is a matter of belief.” – Adam Smith

Today, the stock market snapped its eight-day winning streak. Frankly, the loss was small potatoes, just 0.20%, but I was hoping for another up day, and not just for wealth’s sake, but because the S&P 500 hasn’t rattled off a nine-day streak in nearly 20 years.

Honestly, Wall Street is pretty quiet right now. The volatility index has settled back to the complacent zone, and much of the financial world has zoomed off to the Hamptons or Martha’s Vineyard. At least, the fat cats have. The last two weeks before Labor Day are usually sedate on Wall Street.

The big event on everyone’s mind right now is the Fed’s annual conference in Jackson Hole, WY. In previous years, the Fed has used the Jackson Hole conference to announce major policy changes. In fact, it was at Jackson Hole two years ago that Fed Chairman Jerome Powell made it clear that he intended to crush inflation.

I doubt we’ll see anything so dramatic this time. This year’s conference is titled “Reassessing the Effectiveness and Transmission of Monetary Policy.” (Yawn!)

Chairman Powell is scheduled to speak on Friday morning. I assume he’ll preemptively justify the case for a 0.25% rate cut at the September FOMC meeting. I’m imagine he’ll be vague about plans after that.

Traders see the Fed lowering rates by 100 basis points before the end of the year. That’s a bold outlook. It implies that the Fed will cut by 50 basis points at the November or December meeting. Traders see the Fed cutting by another 100 points within the first seven months of 2025.

The stock market has rebounded impressively from its downdraft last month. In retrospect, the August swoon appears to be quite silly. Traders were panicking over mostly sideshow issues like the carry trade. The Q2 earnings season was mostly good for corporate America.

The S&P 500 is getting close to a new all-time high. In fact, if we were to exclude the Magnificent 7, then the index —the S&P 493— would already be at an all-time high. The hitch is that the losses in the Mag 7 reflect the tremendous sector rotation we’ve seen.

I want to discuss that in a little more depth because in my mind, that’s been the big story. What happened is that growth stocks were crushing value stocks until early July. Once the stock market peaked in mid-July, investors rushed out of growth stocks while value stocks largely sidestepped the damage. That’s the role of value stocks: provide a safe haven when everyone else gets rattled. All told, the selloff wiped off $6.4 trillion in market value.

The rotation was relentless but brief. In a few days, the market unwound the pro-growth undercurrent of the previous three months. The S&P 500 eventually hit bottom on August 5. Since then, the stock market has regained a lot of lost ground.

Here’s where it gets interesting. Growth has indeed led value in this latest rally but it’s nowhere close to the degree of the previous sector rotation.

Think of the rotation this way. The stock market has gone from Trend X to very strongly anti-X and now back to a watered-down X. I suspect that many investors are conflating this watered down X with the original trend. It’s not. It’s not even close.

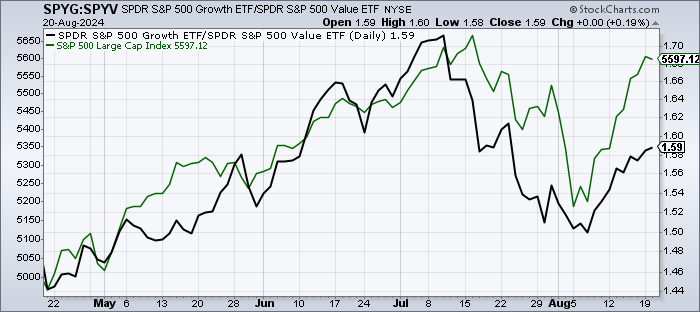

Here’s a chart showing the S&P 500 Growth ETF (SPYG) divided by the S&P 500 Value ETF (SPYV). That’s the black line. I’ve also included the S&P 500 ETF (SPY) in green so you can see what the overall market was doing.

You can see that growth is leading value, but that’s after growth was demolished in July and August.

In this case, I’ve used growth and value, but you can use one of several different charts like Nasdaq versus Russell 2000 or S&P 500 equal weight versus not equal weight. They all show the same effect, Wall Street’s changing tolerance for risk. In turn, that’s related to the Fed’s outlook for interest rates. To quote from Lester Freamon, “all the pieces matter.”

I think the move to value stocks is far from over, but it may not be as dramatic as it was earlier this summer. There’s still a lot of uncertainty in this market.

Lowe’s Cuts Guidance

Speaking of which, I like to watch what big retailers have to say because that can often be a good bellwether for the overall economy.

On Tuesday, Lowe’s (LOW) said that it beat its Q2 earnings estimate ($4.10 vs. $3.97), but that was about the only good news. The home improvement company missed on sales expectations ($23.59 billion vs. $23.91 billion), and it lowered its full-year outlook. Lowe’s is not alone. Last week, Home Depot (HD) lowered its outlook for the second half of this year.

Previously, Lowe’s said it was expecting full-year revenues of $84 billion to $85 billion. Now it dropped that to a range of $82.7 billion to $83.2 billion. The company expects comparable store sales to fall by 3.5 to 4%. That’s down from the prior forecast for a decline of 2% to 3%. Lowe’s made $4.56 per share for the same quarter one year ago.

What’s going on? The CEO said shoppers are waiting for the Fed to lower rates. While that may be true, I’m always a bit skeptical when management says outside forces are to blame. Comparable sales fell by 5.1% last quarter.

There are some key differences between the business models of Home Depot and Lowe’s. For example, HD gets a larger share of professionals. About half of HD’s sales are to home professionals while it’s only 25% for Lowe’s.

Lowe’s is just one data point. Last week, Walmart posted good earnings and raised guidance. Goldman Sachs recently raised its odds for a recession from 15% to 25%, and now it’s lowered the odds to 20%.

Tomorrow Is Benchmark Revision Day!

Let me warn you. Tomorrow morning, about one million American jobs will disappear in an instant. Well, let me be a little more accurate—the government’s official count of American jobs will be lowered by a lot.

This is the time of year when the government bean-counters issue their preliminary benchmark jobs revision. This is real technical stuff, but this year, the revision will likely show that job growth has been weaker than originally reported. It could be by a lot.

There’s no need to panic because the time period has long since passed. The revision covers the 12 months through March. The BLS originally said that nearly three million jobs were created in those 12 months. Even after a big revision, jobs growth was going well.

Wall Street has no idea what the revision will be. Goldman and Wells Fargo said the revision will be by 600,000 jobs. It’s all just a guess. JPMorgan said it will be by 360,000. Goldman said it could be as high as one million.

Here’s how Bloomberg describes the revision:

Once a year, the BLS benchmarks the March payrolls level to a more accurate but less timely data source called the Quarterly Census of Employment and Wages, which is based on state unemployment insurance tax records and covers nearly all US jobs. The release of the latest QCEW report in June already hinted at weaker payroll gains last year.

The revision will tell us how robust the jobs recovery was. Since this is an election year, it will certainly get some attention. (And no. No one “cooked the books.”) As to what the Fed is planning, the revision is largely irrelevant.

There’s more to look forward to this week. Of course, Jerome Powell will be speaking at 10 am ET on Friday morning. Tomorrow, the Fed will release the minutes of its most recent meeting. On Thursday, we’ll get the last initial claims report and the report on existing-home sales. That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on August 20th, 2024 at 6:16 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His