CWS Market Review – August 27, 2024

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

“The time has come for policy to adjust.”

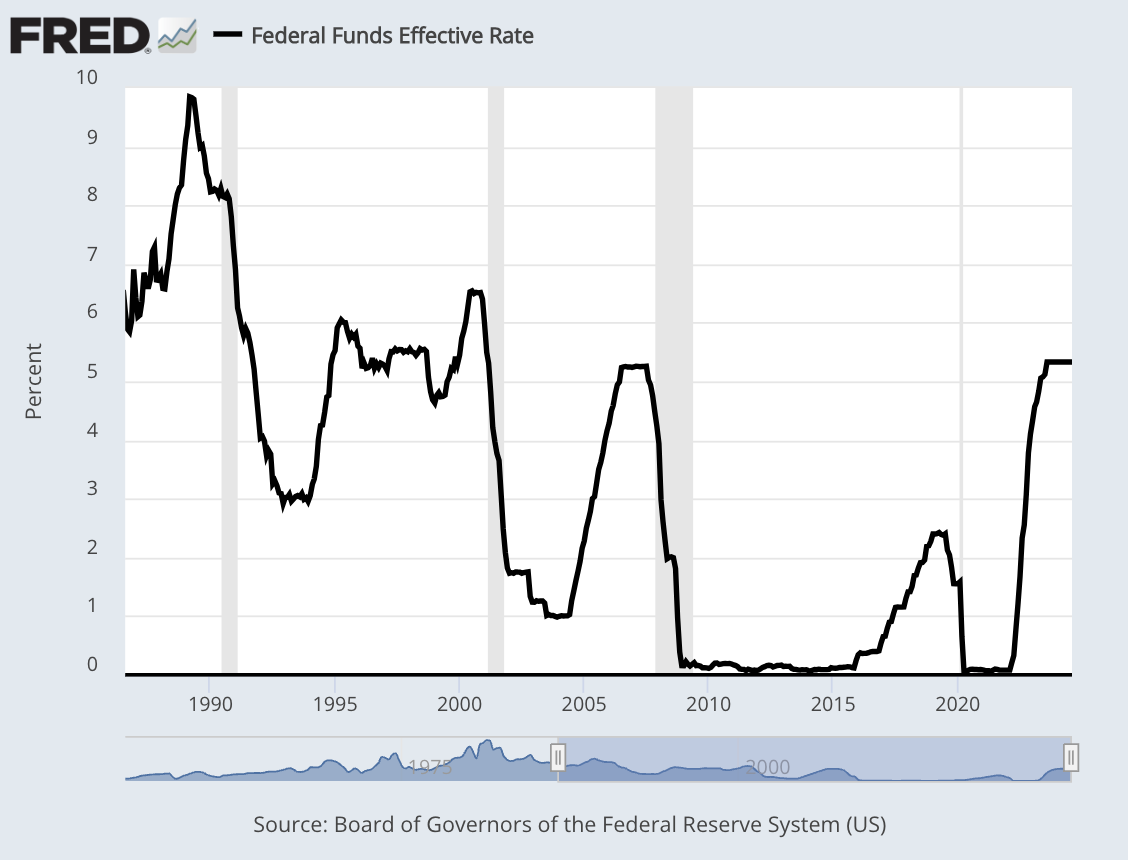

So said Fed Chairman Jerome Powell last Friday at his highly anticipated speech at the Fed’s annual conference in Jackson Hole, Wyoming. He basically said what everyone expected him to say: the time has come to lower interest rates.

This is a big deal. After all, the Fed hasn’t lowered interest rates since Covid. If you exclude that since Covid was a very unusual event, then the Fed hasn’t cut rates for pure economic reasons in 15 years.

The only questions now are when and by how much. Powell left both unanswered but Wall Street expects action soon. In his remarks, Powell noted how much the economy has improved:

“Inflation has declined significantly. The labor market is no longer overheated, and conditions are now less tight than those that prevailed before the pandemic. Supply constraints have normalized.”

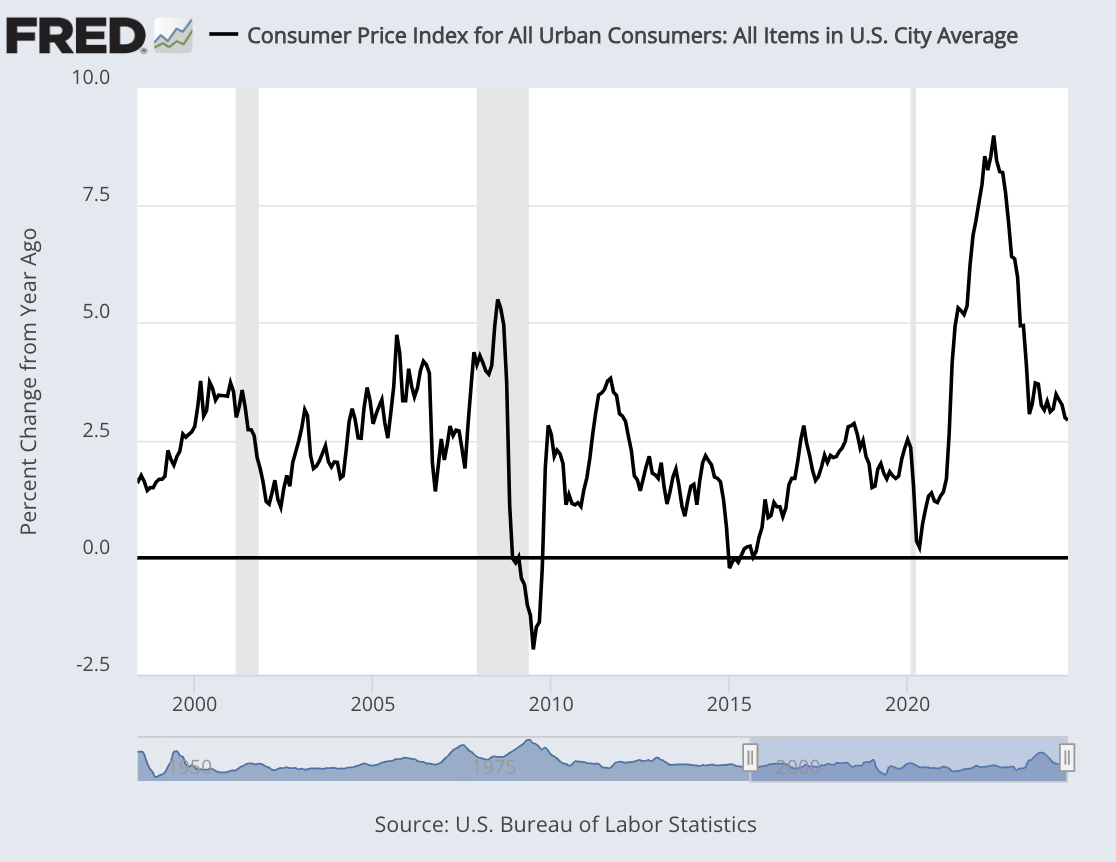

The story is not a complicated one. The Fed responded to Covid by dropping interest rates to the floor. That, and a lot of government money, helped spark the worst bout of inflation in 40 years. Even the lower rate is still higher than where it was during much of the 2010s. Here’s a look at the CPI:

The Fed responded to inflation by jacking up interest rates by 5.25% in 16 months.

It worked. After peaking two years ago, inflation has gradually retreated – not that prices are down – but the rate of increase is down.

“After a pause earlier this year, progress toward our 2 percent objective has resumed. My confidence has grown that inflation is on a sustainable path back to 2 percent.”

Maybe. I have to confess that the Fed’s rate hikes did less damage to the economy than I expected, and higher rates certainly haven’t stopped the stock market. As you may recall, Powell and the Fed initially believed the uptick in inflation was “transitory.” The feeling was that as long as inflation expectations were low, then inflation would be low. That turned out not to be the case, and inflation was anything but transitory.

Why Interest Rates Are So Important for Stocks

I know I spend a lot of time going on about the Fed and interest rates, and I do so because it’s central to the stock market. Interest rates are important for two reasons. One is that interest costs are a major portion of a company’s income statement. Higher rates take a big bite out of the bottom line.

When rates are low, it’s easier for companies to finance expansion plans or to buy out other companies. Higher rates grind that to a halt. Not only are companies impacted but so are consumers. A company like a homebuilder can see its business evaporate when mortgage rates get too high.

The other key reason is that interest rates are in competition for investors’ money. In 1981, you could have locked in a 15.8% yield in a 10-year Treasury. Why buy stocks when you can get a low-risk return that high? Indeed, stocks had to plunge in value just to keep pace. Around that same time, the S&P 500 was trading for less than 6.5 times earnings.

In retrospect, I think the Fed responded to inflation the way it should have responded to the financial crisis of 2007-2008. The Bernanke Fed was very careful when it should have acted earlier and more aggressively. It was two years ago at Jackson Hole that the Powell Fed finally rejected the transitory idea and made it clear that the Fed would do whatever it takes to beat inflation.

On Friday, Powell also noted that the jobs market is cooling off, but what’s interesting is that it’s not dropping as it would normally ahead of a recession. Instead, the jobs market is seeing “a substantial increase in the supply of workers.” What this means, in the Fed’s view, is that the jobs market probably won’t be a driver of inflation anytime soon. I think that’s the key in why the Fed decided to alter course.

Powell also defended himself with some excuses that might be considered a little convenient. For example, Powell said that once inflation broke, it became a global issue because it rested on “rapid increases in the demand for goods, strained supply chains, tight labor markets, and sharp hikes in commodity prices.” In other words, things were affecting everyone.

Powell strongly wants to prevent the public from having higher inflation expectations. That’s what happened in the 1970s. If people expect inflation to rise, then it’s easier for prices to rise. Once the expectations take hold, they get embedded and it’s not easy to change them. I think Powell is particularly sensitive to the issue of expectations.

By 2022, we had a very unusual economy. The labor market was very tight and there were twice as many jobs as there were unemployed people. So, how come the jobs market wasn’t wrecked by the Fed’s anti-inflation crusade? That’s a puzzle to me.

According to Powell:

“Pandemic-related distortions to supply and demand, as well as severe shocks to energy and commodity markets, were important drivers of high inflation, and their reversal has been a key part of the story of its decline. The unwinding of these factors took much longer than expected but ultimately played a large role in the subsequent disinflation.”

Powell was very reticent on what the Fed has planned. The next FOMC meeting is in three weeks and market participants overwhelmingly expect a rate cut. Right now, the odds are at 65% for a 0.25% cut and at 35% for a 0.50% cut.

The following meeting is in November, shortly after the election. At that meeting, traders narrowly expect a 0.5% cut. Traders expect another 0.25% at the December meeting. Add it up and the Fed is expected to slash rates by a full 1% before the end of the year. For 2025, Wall Street expects more cuts of 1.25% to 1.50%.

Overall, lower interest rates should be good for the stock and the housing markets. Not only are lower rates good for the market, but I expect value stocks to continue to prosper. Many of these issues lagged the market as investors fell in love with the Mag 7. That love affair may have run its course. Tesla (TSLA) hasn’t made a new high in close to three years. Amazon (AMZN), Google (GOOGL) and Microsoft (MSFT) are all off more than 10% from their highs.

Heico: The Quiet 83,000% Winner

One of our Buy List stocks, Heico (HEI), issued a very good earnings report after yesterday’s close.

Heico has been a great stock for us this year. The shares are up more than 38% YTD. I’ll discuss Heico’s results in greater detail in Thursday’s premium issue, but I’ll highlight a few key stats for you (you can sign up for our premium issues here).

For its fiscal Q3, Heico’s EPS increased 31% to 97 cents per share. That beat Wall Street’s consensus of 92 cents per share. For the first nine months of this fiscal year, Heico’s earnings are up 23% to $2.67 per share.

For the quarter, Heico’s sales were up 37% to $992.2 million. Their operating income increased 45% to a record $216.4 million. I was impressed to see Heico increase its operating margin by 1.1% to 21.8%. Q3 EBITDA rose 45% to $261.4 million.

Heico is a great example of a niche business that’s not well-known. In 30 years, the stock is up 83,000%.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on August 27th, 2024 at 5:29 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His