CWS Market Review – September 10, 2024

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

“The idea that a bell rings to signal when to get into or out of the stock market is simply not credible. After nearly fifty years in this business, I don’t know anybody who has done it successfully and consistently. I don’t even know anybody who knows anybody who has.” – Jack Bogle

The Market Stumbles Into September

How things change after Labor Day! In last Tuesday’s issue, I told you that Labor Day has often marked a tone shift on Wall Street, Historically, September and October have been tough times for the market. Well, we certainly learned that lesson again this year.

Presidential election years have been especially difficult for the stock market. From September 7 to October 12 in presidential election years, the Dow has lost an average of 2.72%.

On the Friday before Labor Day, the S&P 500 closed very close to a new all-time high, but last week, the index had its worst week of the year. That’s even more impressive when you recall that last week only had four trading days. The S&P 500 fell lower on all four days, and it culminated in last Friday’s underwhelming jobs report (more on that in a bit).

The market rebounded nicely yesterday and today. The market’s thinking seems to have shifted from, “Good news! The Fed will soon be cutting rates,” to “Bad news, the economy is getting weak, and the Fed will soon be cutting rates.”

The next test for the market will be tomorrow’s CPI report. The inflation numbers have been getting better but at a very slow pace. The consensus on Wall Street is that the headline and core rate of inflation increased by 0.2% last month.

Weak Jobs Report Drags Down Stocks

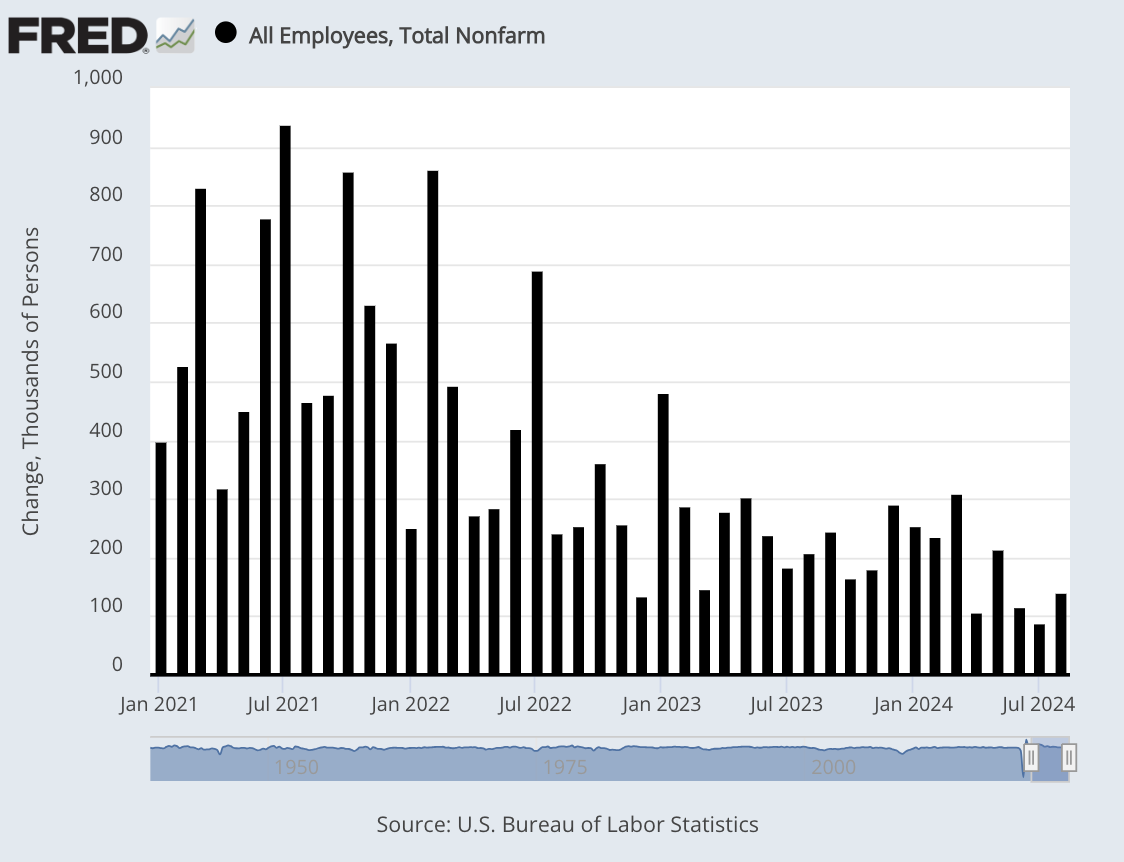

On Friday, the government said that the U.S. economy created 142,000 net new jobs last month. That’s not that good. It missed consensus by 19,000. For July, the economy created 89,000 new jobs.

The unemployment rate dropped by 0.1% to 4.2%, but the broader U-6 rate increased to 7.9% which is close to a three-year high.

The government also revised previous jobs reports lower. The total for July was cut by 25,000, and the June number was lowered by 118,000. Here you can see the steady decline in non-farm payrolls gains.

One bright spot in the report was average hourly earnings. That increased by 0.4% last month while the estimate was for a gain of 0.3%. Over the last year, average hourly earnings are up by 3.8%. That’s good to see, but it’s nearly in line with inflation.

The labor force participation rate was unchanged at 62.7%. It seems that more workers are shifting from full-time work to part-time. The household survey said that part-time employment increased by 527,000 and full-time decreased by 438,000.

From a sector standpoint, construction led with 34,000 additional jobs. Other substantial gainers included health care, with 31,000, and social assistance, which saw growth of 13,000. Manufacturing lost 24,000 on the month.

The Federal Reserve meets again next week. The policy statement will be released on Wednesday, September 18. According to the futures market, there’s a 100% chance that the Fed will cut rates. The only question is by how much.

Currently, the market thinks there’s a 67% chance of a 0.25% cut and a 33% chance of a 0.50% cut. Going by what Jerome Powell has said, I think the Fed is leaning towards a 0.25% cut. The futures market thinks there will be a 50 basis-points cut at the November meeting which will be two days after the election.

Investors should understand that the market is becoming more conservative. Value stocks and low-volatility stocks has been leading the market while many of the growth names have been lagging. Several prominent stocks are more than 20% off their highs. This will probably continue as rates head lower. I’m pleased to see that our Buy List has outperformed by a wide margin over the last two months. (It hasn’t always been that way!)

Stock Focus: Cass Information Systems

This week, I want to tell you about Cass Information Systems (CASS). Cass is a business services company based in St. Louis, Missouri. You probably have not heard of them, but Cass is crucial to many companies. Cass processes and pays 50 million invoices each year.

Cass wants to pay your company’s bills. The information services firm provides freight payment and information processing services to large manufacturing, distribution, and retail companies across the U.S.

Its offerings include freight bill payment, audit, and rating services as well as outsourcing of utility bill processing and payments. Its telecommunications division manages telecom expenses for large companies. Cass grew out of Cass Commercial Bank (now a subsidiary), which provides banking services to private companies.

The company’s international reach is truly impressive. Cass pays invoices in 185 countries and in 114 different currencies. Cass lets companies have complete visibility into every detail of their transportation spending with total trust in the data.

Cass helps save millions in telecommunications costs thanks to an expense management partner who studies the data and recommends savings initiatives. Cass helps pay utility bills reliably on time. Cass can also leverage benchmarking data for waste removal costs to negotiate new contracts. This helps save time and money.

This is a superb company that is largely ignored by Wall Street. This is an especially good time to look at Cass because it’s operating in a difficult environment.

In July, Cass reported Q2 earnings of 32 cents per share. That’s down from 52 cents for last year’s Q2. According to the company, Cass lost over “$100 million of non-interest-bearing funding due to a cyber event at a client and incurring an aggregate of $3.4 million of one-time expenses.”

CEO Martin Resch said, “We successfully onboarded several large facility clients, increasing year over year facilities transactions by 25.1%, with a full queue of additional signed deals still to implement.”

Now here are some important details on why I like Cass. The dividend currently yields close to 3%. That’s not bad in a lower-rate environment. Cass has very little long-term debt, and it’s sitting on a mountain (well, small hill) of cash. At last count, Cass’s cash comes to $223 million. That works out to $16.41 per share. This is important because it tells us that Cass is more efficient than it initially appears to be.

The stock hasn’t performed very well recently which catches my attention. By conventional metrics, Cass is reasonably priced. However, if Cass can return to the kind of growth it used to have, then this could be a very profitable position.

Historically, Cass has favored doing several small stock splits every few years. That may lead people to think that Cass hasn’t done as well as it has. Cass currently has over 1,000 employees and a market cap of $550 million.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. There will be no Tuesday issue next week. I’m going to be at the Future Proof Conference in Huntington Beach, CA. If you’re around, please come by and say hello. We’ll be at booth #702.

Posted by Eddy Elfenbein on September 10th, 2024 at 6:03 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His