Archive for September, 2024

-

Morning News: September 4, 2024

Eddy Elfenbein, September 4th, 2024 at 7:03 amOil Prices Fall Below $70 a Barrel. OPEC+ and Libya Expected to Increase Output

Climate Losses Batter Insurers While Reinsurers Step Back

Japan’s Era of ‘Free’ Mortgages Is Coming to an End

Glynn’s Take: Australian Consumers May Be Down, But Not Out

High Rates Expose Global Banking’s Multi-Trillion-Dollar Weak Spot

China Weighs Cutting Mortgage Rates in Two Steps to Shield Banks

Bank of France Chief Sketches Out Path to Budget Credibility

Bond Volatility in US Eclipses Europe as Recession Angst Rises

US Jobs Data Will Decide the Size of Fed’s Rate Cuts

Credit-Rating Providers Settle With SEC Over Off-Channel Communication Violations

September Gets Started With Déjà Vu From August

Traders Weigh ‘Buy the Dip’ Opportunities Amid Stocks Selloff

Nvidia’s Huang Loses $10 Billion in His Biggest Wealth Wipeout

Intel’s Money Woes Throw Biden Team’s Chip Strategy Into Turmoil

Hewlett Packard to Pursue $4 Billion Claim Against Mike Lynch’s Estate

Blackstone to Buy Australia’s AirTrunk in A$24 Billion Deal

Temu’s Parent, a Victim of Competition or Its Own Success?

U.S. Steel Warns of Plant Closings if Sale Collapses

How Immigration Remade the U.S. Labor Force

US Port Talks Kick Off in Bid to Avoid Economy-Disrupting Strike

For Volkswagen, the Bumpy Road to Electric Vehicles Starts to Hit Home

VW Defends Plan to Shut German Factories With Plunging Sales

GoTo Exits Tough Vietnam Market to Focus on Reaching Profit

NYC’s Biggest Taxi Insurer Is Insolvent, Risking Transit Meltdown

Cargill, America’s Largest Private Company, Faces Leaner Times

Walmart Bets on Collectible Sneakers to Grow Marketplace Service

Be sure to follow me on Twitter.

-

CWS Market Review – September 3, 2024

Eddy Elfenbein, September 3rd, 2024 at 6:05 pm(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

“The expectation of an event creates a much deeper impression on the exchange than the event itself.” – Jose de la Vega, 1688

On Friday, the S&P 500 closed out August with a gain of 1.01%. It’s interesting that last month turned out to be a decent month for the market. For a while, it didn’t look that way.

From July 16 until August 5, the stock market had a minor dustup. Of course, we didn’t know it was going to be minor at the time.

What I find interesting is that if you had only paid attention to the stock market’s monthly closing price, you would have had no idea that at one point, the stock market dropped more than 8% this summer.

Ignoring the sound and fury of the daily market not only makes you a better investor, but it also gives you a better sense of what the market is really doing.

The recent monthly data has been entirely uninteresting. For August, the S&P 500 gained 2.28%. This was the index’s fourth monthly gain in a row, and its ninth gain in the last ten months.

This has been a very good time for individual investors. JPMorgan said that stocks currently make up 42% of Americans’ total financial assets. That’s the highest on record since 1952. Fidelity said that the number of its 401k accounts worth more than $1 million is up 31% in the last year.

Will the good times last?

It’s true that historically, Labor Day has marked a change in sentiment on Wall Street. Traditionally, September and October have been weak months for the stock market. We’ve even had some of our worst markets in history come at this time of year. I’m not sure why. Perhaps traders are eager to take profits after a strong summer rally.

This year, it didn’t take long for September to get off to a slow start. The market had a lousy day today. The Dow was off more than 6000 points, and the Nasdaq was down over 3%.

Today’s trading is also a good example of how Nvidia has come to dominate the entire market. The tech giant opened lower, and it pulled nearly the entire tech sector with it. At its low, NVDA was down more than 7.5% today.

It seems like every day, NVDA calls the tune. If it rallies, a mass of growth stocks rallies in its wake. But on a bad day, like today, NVDA is one of the worst performers in the S&P 100, and many others will get pulled under, too. The market is the east and Nvidia is the sun.

Over the last four trading sessions, shares of NVDA have lost roughly one-sixth of their value. That’s half a trillion dollars. For today, I suspect it was a case of some NVDA longs looking for a good chance to book some very nice gains.

This was an unusual trading day because outside tech, most defensive stocks had a quiet day. In fact, many defensive stocks posted decent gains today and more than a few, like Walmart, Coca-Cola and Stryker, made new 52-week highs today.

The S&P 500 High Beta Index was down over 4.2% today while the S&P 500 Low Vol Index was up 0.04%. The Nasdaq lost almost as many points as the Dow did today, despite having less than half the nominal point value.

There’s not much news from Wall Street at the moment, but that will change soon. This Friday, we’ll get the jobs report for August. In the July report, the unemployment rate reached a 33-month high.

After the jobs report, we’ll get the CPI report for August the following Wednesday, which is the 11th. To be fair, the inflation numbers have improved but at a very slow rate.

We’re now two weeks away from Rate Cut Day. This day has been three years in the making. This is when the Federal Reserve will finally lower interest rates.

There’s little doubt that the Fed will cut rates. The only question is, by how much? Going by prices in the futures pits, traders think there’s a 63% chance of a 0.25% and a 37% chance of a 0.50% cut. The odds of the Fed doing nothing are at 0%. I’m not exaggerating.

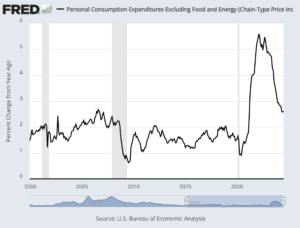

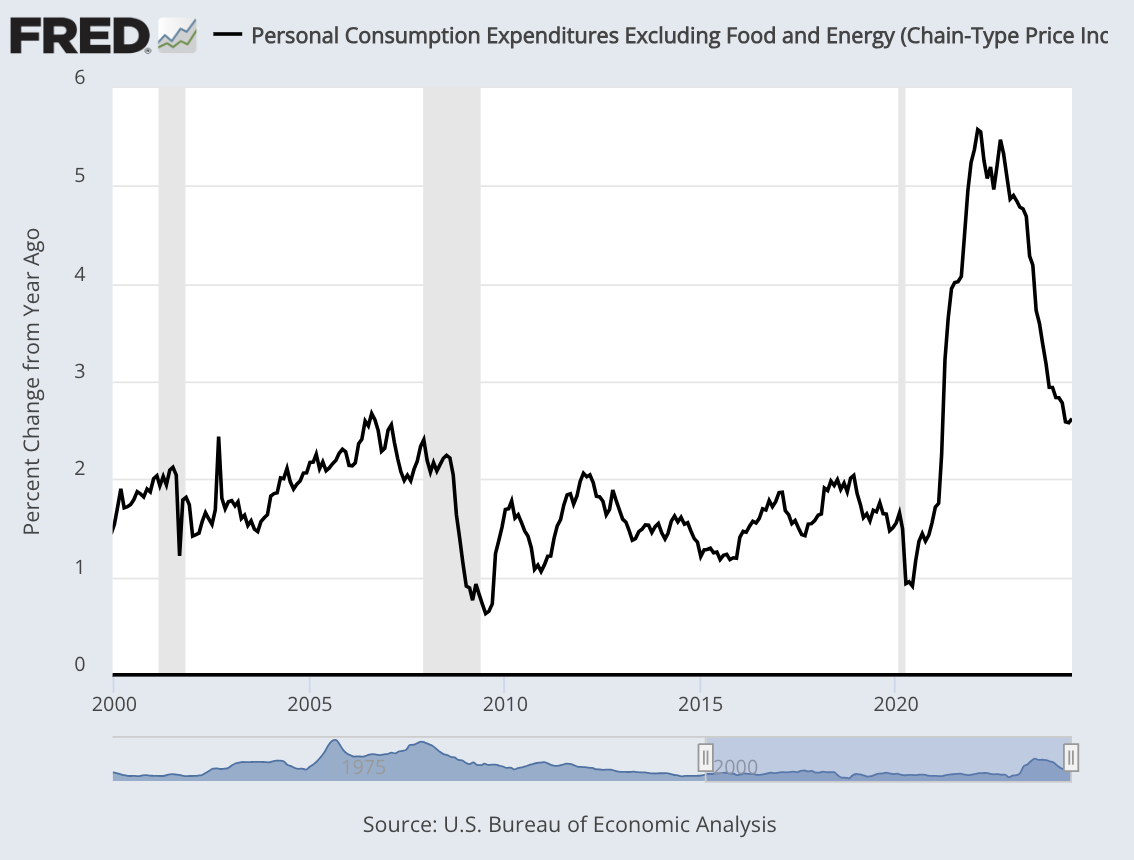

We still have data coming in. On Friday, the Commerce Department said that the personal consumption expenditure price index, or PCE, rose by 0.2% last month which matched expectations. This is important because it’s the Federal Reserve’s preferred measure of inflation. Over the last year, the PCE Index has increased by 2.5%.

The core PCE, which doesn’t include food or energy prices, was also up by 0.2% last month, and also matched expectations. Over the past year, the core PCE is up 2.6% (see above).

Core prices less housing, another key metric for the Fed, increased just 0.1% on the month. As other inflation components ease, shelter has proven to be stubborn, again rising 0.4% in July, according to Friday’s report.

Elsewhere in the report, the department’s Bureau of Economic Analysis said personal income increased 0.3%, slightly higher than the 0.2% estimate, while consumer spending rose 0.5%, in line with the forecast. Spending continued at a solid clip even though the personal savings rate fell to 2.9%, the lowest since June 2022.

From a component standpoint, inflation changed little over the past month. The BEA said that goods prices fell by less than 0.1% though services increased 0.2%.

On a 12-month basis, goods also were off by less than 0.1%, while services jumped 3.7%. Food prices were up 1.4% and energy accelerated 1.9%.

One weak spot today was the ISM Manufacturing report. I tend to favor the ISM report for a few reasons. One is that it’s a survey, so it’s not specifically placed on economic activity. I also like that the report comes early, usually on the first business day of the month. So much econ data is lagging.

The ISM also tends to line up well with recessions. Whenever the ISM Manufacturing Index dips below 45, then there’s a good chance that we’re in a recession.

This morning, we learned that the ISM for August came in at 47.2. Any number below 50 indicates that the economy is contracting; above 50 and the economy is expanding. Today’s report was below expectations which were for 47.9. The ISM for July was 46.8.

The weak July report, which came out in early August, helped cause the market to have a minor downdraft this summer. We’ve recovered most of what we lost, but not all of it.

Stock Focus: Winmark (WINA)

This week, I wanted to tell you about a fascinating small-cap company called Winmark Corp. (WINA). It has a market value of $1.25 billion and it’s only followed by one analyst on Wall Street.

I’m not recommending it, but it’s an interesting company to put on your radar screen. The company franchises five different types of retail stores: Style Encore, Plato’s Closet, Once Upon a Child, Play It Again Sports and Music Go Round.

While the stores are different, they share a common theme: they buy and sell slightly-used merchandise. Winmark also provides leasing for its business partners.

Since March 2000, the stock is up more than 13,000%.

Because of the company’s unusual structure, they do about $80 million in sales despite having about 85 full-time employees.

From 2000 to 2016, Winmark was led by John Morgan, who turned the ship around. It’s difficult to describe Winmark. I suppose it’s like what eBay would be if they had stores.

WINA looks rather pricey at the moment but it’s worth following.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

-

Morning News: September 3, 2024

Eddy Elfenbein, September 3rd, 2024 at 7:07 amNew Argentine Currency Launched to Offset Milei’s Shock Therapy

Why It’s So Hard for China to Fix Its Ailing Economy

China Policy Outlook Hinges on the Definition of ‘About’

Russia’s Sberbank Says India Business Booming Despite Western Sanctions

Japan Bank Shares Rise as 10-Year JGB Yield Hits Nearly One-Month High

Wall Street Strategists Face Their Own Short Squeeze

Gold Is Rising Because of Demand for ‘Fallback Money’

Americans Are Really, Really Bullish on Stocks

Moody’s Upgrades Outlook on Global Reinsurers to Positive from Stable

Citadel Securities, Jane Street on Track for Record Revenue Haul

The New Rules of Debt Are Totally Cutthroat

Rise of the Pint-Size Startup Is Reshaping the U.S. Economy

Can Democrats Stop the ‘Tax Doom Loop’?

Claudia Sahm: The Jobs Numbers Went Down, But Trust in Them Shouldn’t

Delivery Hero Lines Up Banks for Talabat’s Dubai Listing

When Property Investors Want Out, These Bargain Hunters Rush In

This Once Hot Real-Estate Type Is Now Being Offered as Office Space

Shutting Off Elon Musk Won’t Help Brazil’s Democracy

Shorts Are Circling Some of the AI Boom’s Biggest Question Marks

China Needs More Factory Robots. Can It Build Its Own?

VW Turns on Germany as China Targets Europe’s EV Blunders

Uber Smells Opportunity in South Korean Internet Upheaval

Korea to Impose Stricter Emissions Trading Rules to Boost Prices

Kamala Harris Says U.S. Steel Should Stay American-Owned

Ryanair, Wizz Air August Passenger Numbers Reach New Records

The Day Delta’s ‘On-Time Machine’ Broke, and the Blame Game It Sparked

Be sure to follow me on Twitter.

-

Morning News: September 2, 2024

Eddy Elfenbein, September 2nd, 2024 at 7:09 amChina-Philippines Row Opens New Flashpoint in South China Sea

China Warns Japan of Retaliation for Possible New Chip Curbs

China’s Bulging Commodity Stockpiles Show Depth of Economic Woes

Asia Manufacturing PMIs Show Some Weak Spots But Keep Signaling Growth

Leveraged Finance More Than Doubles in Europe Despite ECB Probe

Swiss Franc Carry Trade Comes Fraught with Safe-Haven Rally Risk

Markets’ Summer Vacation Is Over

Treacherous September Is Leaving Traders Everywhere on Edge

Emerging Stocks Drop as Traders Watch China’s Economy, US Data

Hedge Funds Bet Against Banks, Insurance and Property, Says Goldman Sachs

Silicon Valley Bank Exits China Joint Venture, Local Partner Takes Full Control

Blackstone Is Said to Near $13 Billion Deal to Acquire AirTrunk

Nvidia CEO Jensen Huang Surprised by Skeptics

China EV Sales Rise on Government Subsidies, Inventory Buildup

Car Carriers With Greener Ships Face Higher Costs

About 10,000 Hotel Workers Walk Off the Job on Labor Day Weekend

Has the Spread of Tipping Reached Its Limit? Don’t Count on It.

A Funnel Cake Macchiato, Anyone? The Coffee Wars Are Heating Up.

Bayer Kidney Drug Helps Treat Common Form of Heart Failure

News Corp’s REA Mulls Offer for Rightmove

Musk’s Starlink Defies Order to Block X in Brazil

Mark Cuban Says Elon Musk’s ‘Biggest Power Play’ on X Is Letting Users Think They Have Free Speech

ESPN and ABC Go Dark on DirecTV in Feud With Disney

Netflix Is Trying to Get You Hooked on More Reality TV With Better Dubbing

$13 for a Video Call. $25 for a Movie. Tablets Connect Prisoners—at a Steep Price.

America’s Cup: The Billionaire’s Trophy Where $135 Million Disappears in Days

Be sure to follow me on Twitter.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His