CWS Market Review – October 15, 2024

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

The Stock Market Rally Turns Two Years Old

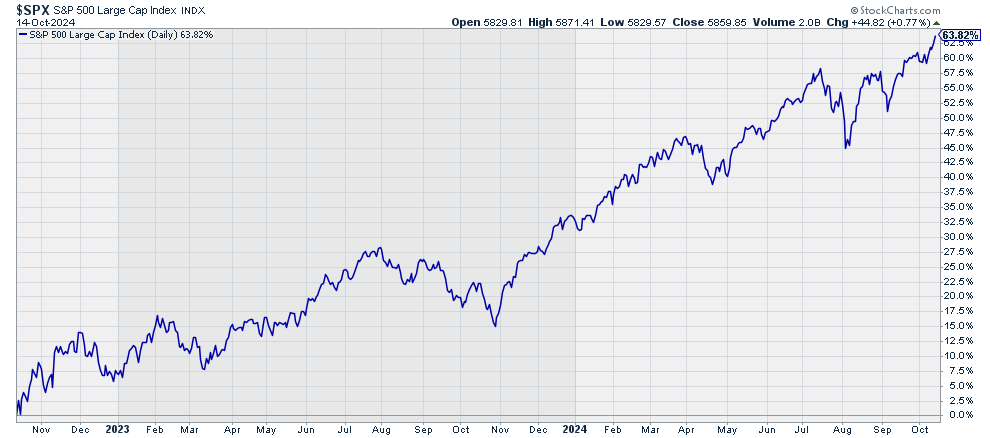

The bond market was closed on Monday in honor of Columbus Day, but the stock market was open, and it was a good day. The S&P 500 rallied to another all-time high. This was our 46th new high of this year. The market gave back some of those gains today, but we’re very close to more new highs.

Interestingly, we just passed the two-year anniversary of the market’s last major low. That came on October 11, 2022 when the S&P 500 closed at 3,577.03. From there to Monday’s close, the S&P 500 has gained more than 63%, not including dividends.

It’s been a remarkable rally, but what’s impressed me about the last two years, on top of the impressive gain, is how steady it’s been. To be sure, there have been bumps and turns like last August, but for the most part, this has been a smooth and steady 63% run.

I was also pleased to see several of our Buy List stocks hit new highs today like Broadridge Financial Solutions (BR), FICO (FICO), Fiserv (FI), Intercontinental Exchange (ICE) and Science Applications International (SAIC).

We’re in the early stages of earnings season and so far, the results look pretty good. According to Bloomberg, “analysts expect S&P 500 firms to report a 4.2% increase in third-quarter earnings versus a year earlier, down from a 7% forecast in mid-July.”

It’s early but so far, 30 companies in the S&P 500 have reported results. Earnings are coming in at an average of 5% better than estimates. At this time last quarter, earnings were running 3% higher than expected.

As we know, Wall Street’s usual game is to be as downbeat as possible going into earnings season thereby getting Wall Street analysts to lower expectations. Then, when earnings day comes, they announce a big earnings beat and hopefully, the stock will rally.

That’s pretty much what happened last week when the first earnings reports came out. Usually, the big banks are the first to report and that sets the tone for earnings season.

On Friday, JPMorgan (JPM) reported Q3 earnings of $4.37 per share. That easily topped the consensus of $4.01 per share. JPM is the biggest boy of a lot of big boys on Wall Street, and its results are very influential. It’s a Dow component and one of the largest companies by market value on Wall Street. If JPM is doing well, that’s probably a good sign for all banks.

JPM is particularly good at steering Wall Street’s outlook. Two months ago, the Street was expecting JPM to make $17.05 per share for next year. That’s now down to $16.73 per share.

JPM had a very good quarter for Q3, and lower rates will serve them well. More good news is that JPM said its net interest income will be about $92.5 billion this year. That’s up from its previous guidance of $91 billion. About geopolitical risks, CEO Jamie Dimon said, “Recent events show that conditions are treacherous and getting worse.”

Also on Friday, though not nearly as big, Wells Fargo (WFC) said it had particularly good results. For Q3, Wells made $1.52 per share which was 24 cents better than expected. The stock got a nice 5.6% pop on Friday, and the shares have continued to rally since then. Until a month ago, Wells looked like it was one of the weaker banks.

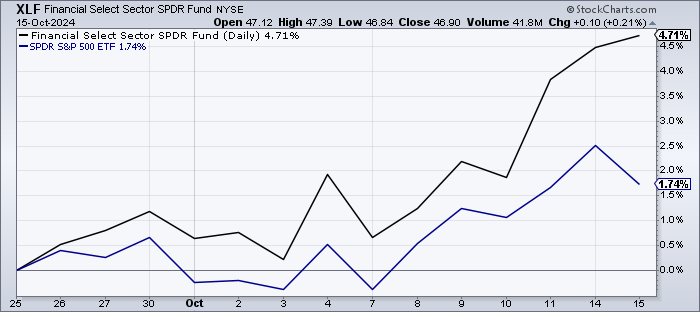

Thanks to the good earnings reports from many Wall Street banks, financial stocks have been doing well of late. Here’s the S&P 500 Financial Index compared with the S&P 500.

The financials hit a new high yesterday, and 36% of its members made new 52-week highs.

We had more good reports today. This morning, Goldman Sachs (GS) released a very good earnings report. For Q3, the bank’s profits increased 45% to $8.40 per share. That was above Wall Street’s consensus for $6.89 per share. Quarterly revenue was $12.70 billion. Wall Street has been looking for $11.8 billion.

Lower rates will be good for Goldman, as well. Last quarter, Goldman’s investment banking revenue rose 20% to $1.87 billion. Equities trading was up 18% to $3.5 billion.

Also on Tuesday, Bank of America (BAC) said it made 81 cents per share for its Q3. That was a four-cent beat. Compared with last year, the bank’s net income was down 12%. Revenue rose a bit to $25.49 billion.

In addition to traditional banking activity, BAC did very well last quarter with Wall Street operations like trading. BAC’s net interest income fell 2.9% to $14.1 billion.

In BlackRock’s (BLK) earnings report, the company said that its assets under management rose to $11.5 trillion. That’s staggering. In Q3, BLK had inflows of $221 billion. For the quarter, BlackRock made $10.90 per share which beat expectations by 92 cents per share.

Citigroup (C) has been trying to turn itself around, and the early results look favorable. The bank’s traders had their best Q3 performance “in at least a decade.” Revenue for its markets division rose a tiny bit to $4.82 billion. Trading revenue rose by 32%.

Citi’s credit card business is dragging along, but its other businesses are helping to make up for the weakness. CEO Jane Fraser is trying to engineer a major about-face for the Wall Street giant. While Citi is looking better, it still has a way to go to get back to full health.

Last quarter, the bank’s fees from investment banking increased 44%. Citi’s EPS fell to $1.51. Bloomberg noted that the “quarter included a provision of $2.7 billion, which was driven by the higher losses in the company’s card business.”

After today, we’ll see more of the non-banks report earnings. Wall Street is mostly optimistic.

Steer Clear of Boeing

I mentioned the turnaround efforts at Citigroup which leads me to an important lesson with investing. One kind of stock I generally steer clear of is the turnaround play. These are companies that have fallen on hard times. With the poor performance, the companies now have the latitude to make dramatic changes to right the ship.

However, in my experience, the problems usually run very deep, and the proposed changes are largely cosmetic. Turnaround stocks rarely turn.

The problem for investors is that the stocks can often appear to be value stocks. The prices are low relative to the company’s recent performance. The problem is that these ratios are backward looking, and it’s the future that’s worried the market.

A good recent example is Boeing (BA). The airplane maker has been in a mess recently. Today the company said it may turn to Wall Street to raise a heap of cash in stock or debt. Boeing said it could raise as much as $25 billion. That could stem some of the short-term financial issues, but Boeing is far from being a strong company.

In a separate filing, Boeing said it reached a $10 billion credit agreement with banks. Some of the credit agencies have warned Boeing that its credit may be downgraded. That would be very costly to Boeing.

Last week, CEO Kelly Ortberg said Boeing could lay off 17,000 workers which is about 10% of its workforce. On top of that, Boeing faces a strike from 33,000 of its machinists. S&P said the strike is costing Boeing more than $1 billion a month.

In January, a Boeing 737 Max 9 suffered “uncontrolled decompression.” A door plug flew off the airplane. Fortunately, no one was hurt but it was not favorable for Boeing. The FAA told Boeing that it’s under investigation.

Boeing’s stock is currently going for 1.24 times sales. In normal times, that could be considered cheap, but not now. Boeing has lots of problems that need to be addressed. I hope the company can turn itself around, but I caution investors that any value in Boeing may be a mirage.

This week will will be dominated by earnings news. Later this week, our first Buy List stock will report its earnings. I’m expecting more good results from our stocks.

I’ll be paying attention to the actual results, but I also want to hear what our stocks have to say about guidance. Typically, our stocks start out the year conservative with guidance and then will gradually raise guidance as the year goes on.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on October 15th, 2024 at 5:24 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His