CWS Market Review – December 3, 2024

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Before I get into today’s email, I have to apologize for some snafu that prevented last week’s premium issue from being emailed out. Perhaps I had too much turkey. In any event, paid subscribers can see that issue here.

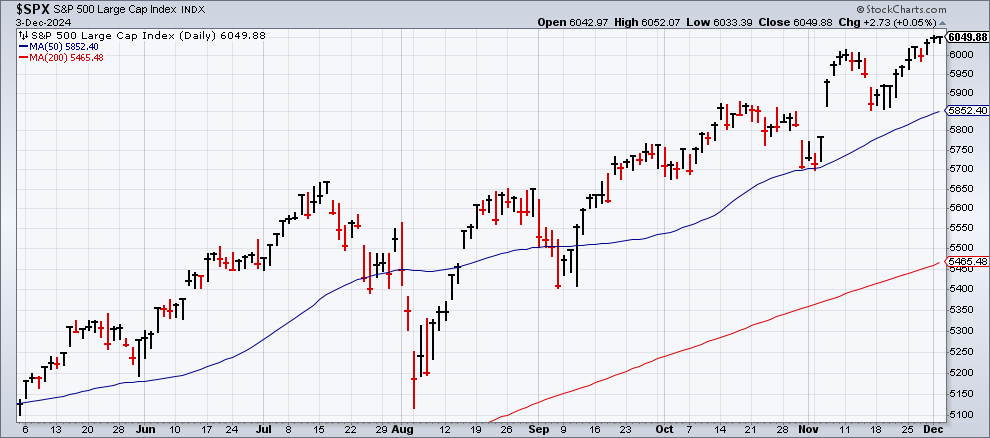

The S&P 500 continues to have a great year. This looks to be Wall Street’s best year since 2021. It’s odd how many people get upset by a rising market. As I’ve often said, “nothing gets people angry quite like good economic news.” That’s even my pinned tweet on X.

Citigroup said that things are getting so bad for the bears (meaning good), that many hot shot short sellers are finally throwing in the towel. The more they’ve held out against the bulls, the worse they’ve done.

European stocks, in particular, have lagged badly versus the U.S. Wait, let me rephrase that—they’re lagging horribly versus the U.S.

Valuations in the U.S. are far higher than what we see across the pond. To be fair, this is like comparing apples to Müeslix. The U.S. markets are much more heavily weighted toward tech stocks, so perhaps they should command higher valuations.

Although it’s just started, the last month of 2024 is proving to be a very good one for growth stocks. On Monday, growth creamed value: +0.79% to -0.76%. The gap between high beta and low vol was even greater: +1.87% to -0.96%. Growth beat value again today.

In plain English, this means that investors are willing to shoulder great risk in search of greater returns. This kind of market typically aligns with rising interest rates. Or in this case, rates that may not be going lower as rapidly as expected.

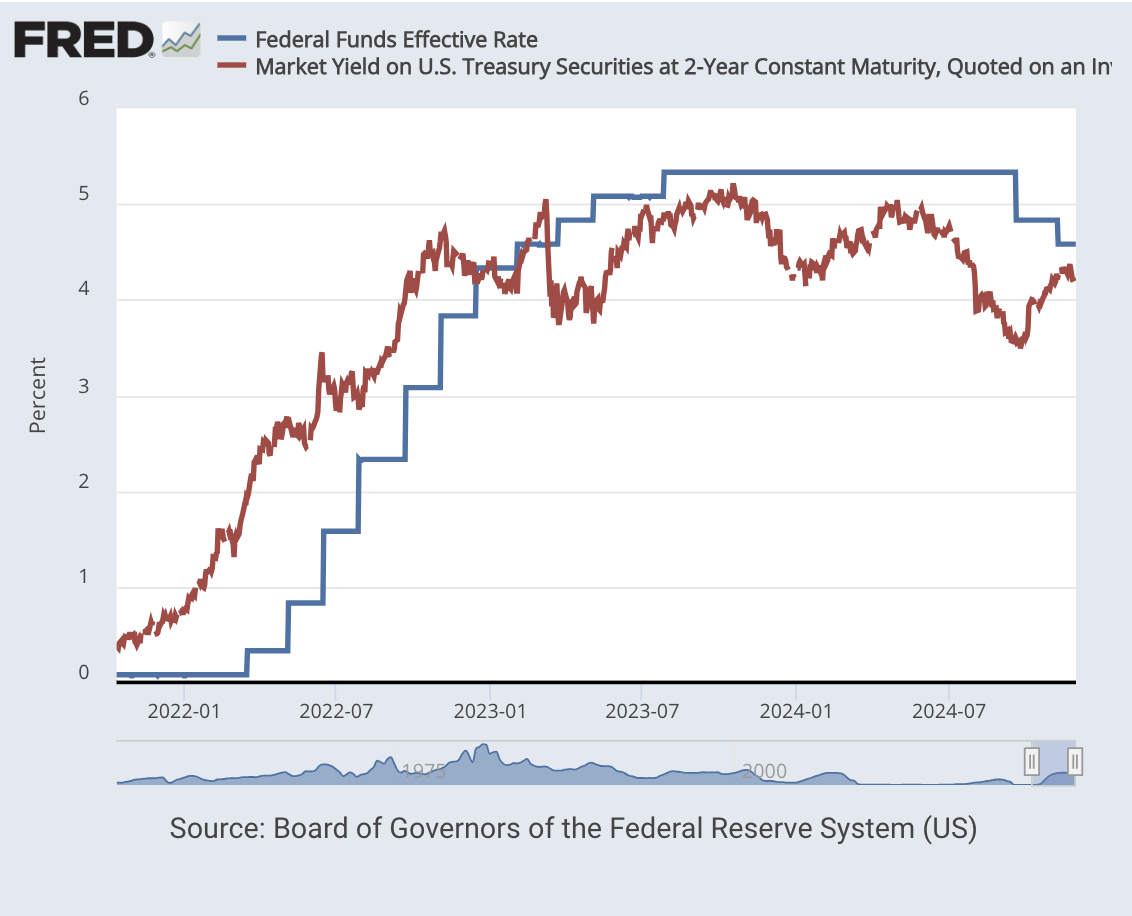

This is a part of a growing gap between what the Federal Reserve has said and what the markets expect. The Fed has consistently said that it’s looking to bring down rates, or in their view, take back the previous rate hikes.

Wall Street doesn’t buy it. Traders think the Fed will cut rates again when it meets in two weeks. That’s not that controversial. The murky part is what comes next. For all of next year, Wall Street only expects two 0.25% cuts from the Fed.

Here’s a cool chart.

This shows the where the Fed is in blue, and the market’s take on the two-year Treasury in red. I like this chart because you can see how the red line anticipates the blue line. It’s like the red is the blue line, just faster.

Notice how the red line has been moving up recently. That shows you how Wall Street is growing less confident in the Fed’s rate-cutting agenda. That’s also what’s driving the sector rotation I described earlier.

Whom to believe? When in doubt, I side with the market’s expectations rather than a roomful of economists. Still, you never know.

What Happened to the Recession We Were Promised?

I feel as if I was promised a recession for this year, and we’re not going to get one. That news is far more upsetting to some folks than I would have expected.

We still have one more month left of this year and of Q4. Goldman Sachs currently pegs Q4 GDP growth at 2.4%. The Atlanta Fed’s model is at 2.7%.

Yesterday we got the ISM Manufacturing Index for November. I tend to like this report because it comes out quickly, usually on the first business day of the month. The GDP reports are great, but they tend to come out long after the fact.

For November, the ISM was 48.4. That’s up from 46.5 for October. Any number below 50 means the factory sector of the economy is shrinking. This was the eighth month in a row that the ISM came in below 50, and it was the 24th time in the last 25 months that it was under 50.

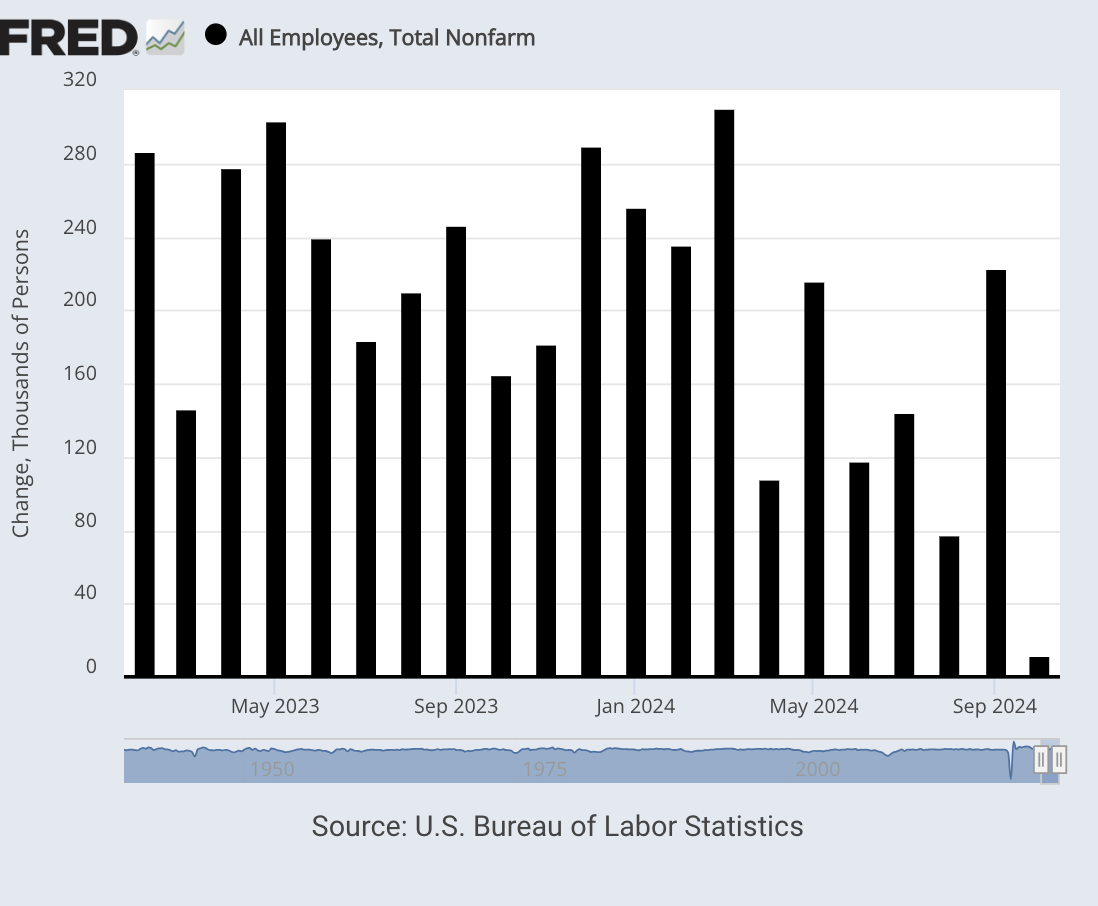

This Friday, we’ll get the November jobs report. Last month, the report for October said that only 12,000 jobs were added to the economy. That number was probably distorted by the storms down south. For Friday, Wall Street is expecting a gain of 214,000 new jobs.

This morning, the Labor Department released its JOLTS report (Job Openings and Labor Turnover Survey) and it said that job openings rose in October by 372,000 to 7.744 million.

There are now 1.11 job openings for each unemployed person. That’s up from 1.08 jobs for September. While that’s nice to see an increase, job openings are still down over the past year by 1.3 million.

Economists polled by Reuters had forecast 7.475 million vacancies. The increase in job openings was led by the professional and business services sector, with 209,000 unfilled positions. Vacancies rose by 162,000 in the accommodation and food services industry and climbed by 87,000 in the information sector.

But there were 26,000 fewer open positions in the federal government. The job openings rate increased to 4.6% from 4.4% in September.

The number of quits also increased. That’s a good metric to follow because a rising number often signals confidence in the economy. Layoffs fell to 1.6 million. That’s the largest drop in layoffs in 18 months.

Stankey’s Bold Turnaround at AT&T

I wanted to comment on the recent success of AT&T (T). The stock has done very well this year, and it’s due to a very simple strategy. The company got rid of its entertainment holdings.

I’m not sure why, but too many companies decide that they need to buy up other firms in order to make their own firms unnecessarily complicated. I remember that Peter Lynch warned of the dangers of holding too much cash on a firm’s balance sheet. They’re liable to spend it unwisely. Lynch referred to this as the Bladder Theory of corporate finance. I see it in action all the time.

AT&T has moved in the other direction. CEO John Stankey got rid of AT&T’s Warner Brothers unit and also its satellite-TV company DirecTV. What was the point of owning them? Stankey also improved the company’s balance sheet by getting rid of tons of debt. The biggest issue was resolving AT&T’s terrible move of merging with Time Warner.

This morning, the company said it is aiming, over the next three years, to return $40 billion to shareholders via dividends and share buybacks. It wasn’t that long ago that Stankey had to cut AT&T’s dividend, and he sold WarnerMedia to Discovery Communications.

Since getting rid of Warner, AT&T is up 50% including dividends while Warner hasn’t done much. AT&T is smaller now, but it’s focused on telecom which is what it does best. AT&T still holds a dominant position in fiber-optic broadband subscribers. Investors love recuring revenue and that’s what AT&T provides with its monthly cellphone bills.

The company’s major challenge now is to upgrade its fiber lines to better compete with companies like Verizon. There’s a lot of work ahead for AT&T and I’m afraid the company will have to shrink its workforce, but this is a good example of a company taking the right steps to make itself more competitive.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on December 3rd, 2024 at 6:21 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His