CWS Market Review – January 21, 2025

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

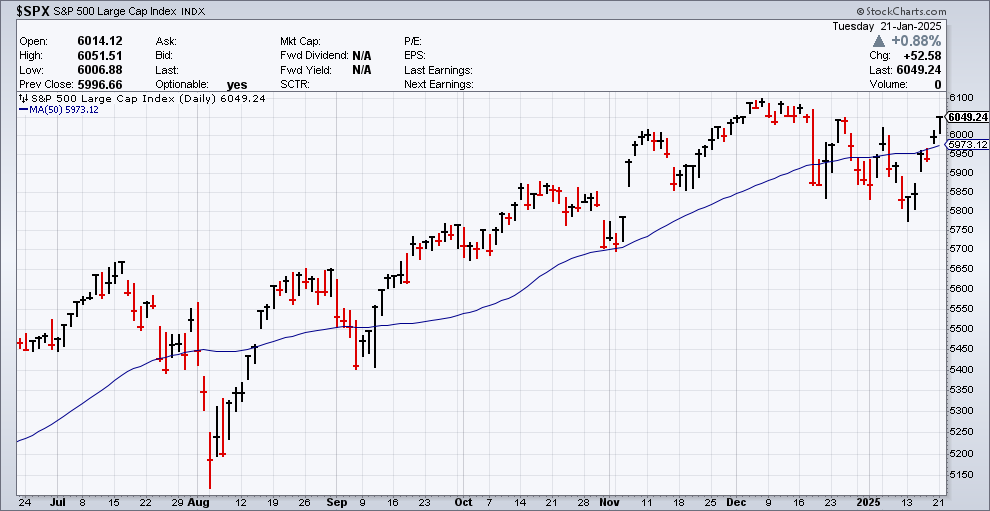

Last year, the stock market averaged one new high a week, but over the last six weeks, there have been zero new highs. Not a single one. For the first time in a while, the stock market appears apprehensive. The market isn’t good or bad, but it’s choppy. It seems like the index can’t muster enough momentum to go in either direction for very long.

Of course, by historical standards, this is perfectly normal. This is what markets do: they bounce around. The unusual period is the one we recently left. Consider that from October 2022 until last month, the S&P 500 Total Return Index gained 75%. That’s not bad for a little over two years’ work.

Just understand that from an investor’s perspective, that was the odd period, not what we’re seeing now. As of Tuesday’s close, the S&P 500 was about 0.75% away from a new all-time high close. It may come tomorrow. As we know, the market gods have a habit of doing the unexpected.

There are a number of signs that suggest that the U.S. economy is healthier than many think. It’s odd how not that long ago, it was assumed that the economy was about to fall on its face. I continue to be amazed by the very poor relative performance of the defensive sectors. Consumer staples and health care stocks, in particular, have badly lagged the market. That’s not what you’d expect to see in a recession or even a late-cycle market.

When you see stalwart blue chips Colgate-Palmolive (CL) and Johnson & Johnson (JNJ) lag the market, I’m inclined to think it says something about the market’s appetite for risk and not much about Colgate and J&J themselves.

While the Mag 7 gets a lot of attention, the tech sector as a whole hasn’t done that well, in a relative sense, over the past year. Instead, we’ve seen impressive relative strength in areas like industrial stocks. Materials are also doing well. These are classic cyclical areas of the market. No one, it seems, wants to hold the steady stalwarts.

On our Buy List, stocks like Miller (MLR) and Mueller (MLI) are both up more than 4% this year. Allison Transmission (ALSN) is already an 11% winner for us this year.

How about IES Industries (IESC)? The company has a market value of $5 billion, 9,000 employees, and it’s not followed by any analysts on Wall Street. It’s up 37% this year!

We’ll soon learn a lot more about these companies when they report earnings. Now let’s look at some details from earning season.

It’s Early but Q4 Earnings Are Looking Good

The Q4 earnings season is starting to heat up. We’ve already had our first few reports, and that will soon turn into a flood.

I should explain that Q4 earnings season is slightly different than the earnings seasons of the other quarters. Companies are allowed a little more time to report their full-year results. That means that Q4 earnings season is longer, and it stretches well into February.

After the closing bell today, we got a very good earnings report from Netflix (NFLX). The stock is up $115 per share, or 13% in after-hours trading.

For this earnings season, we have some early numbers. According to FactSet, 9% of the S&P 500 has reported so far. Of that, 79% have beaten their earnings reports and 67% have beaten sales. That’s quite good.

So far, earnings growth is tracking at 12.5%. Again, that’s early, but if that number holds, it will be the strongest growth we’ve seen since Q4 of 2021, which was severely impacted by Covid.

Only one stock so far has issued negative guidance, but four have issued positive guidance.

The forward P/E Ratio for the S&P 500 now stands at 21.6. That’s not extreme, but it’s higher than the market’s five and ten-year averages (19.7 and 18.2, respectively). Overall, there’s little reason for alarm, especially if earnings continue to grow as they have.

Watch Out for Value Traps

Shares of Walgreens Boots Alliance (WBA) got knocked down by 9% today. The Justice Department said it’s suing Walgreens claiming that the pharmacy chain unlawfully filled prescriptions for addictive painkillers.

The DOJ has already gone after CVS. The opioid epidemic has been a major problem for several years. According to the U.S. government, from 1999 to 2022, there were nearly 727,000 deaths from opioid overdosing.

The lawsuit alleged that by knowingly filling unlawful prescriptions for controlled substances, Walgreens violated the Controlled Substances Act. The government also alleged it violated the False Claims Act when it then sought reimbursement from federal health care programs, like Medicare, for the prescriptions.

The lawsuit was announced after Walgreens filed its own lawsuit on Thursday challenging what it said were new policies the U.S. Drug Enforcement Administration had unlawfully adopted, seeking to ensure pharmacies do not dispense controlled substances for medically illegitimate purposes.

CVS had to write a big check, and I suspect that Walgreens will have to do the same. Two weeks ago, WBA reported good earnings for its fiscal Q4. The company made 51 cents per share which topped expectations of 38 cents per share.

I’m highlighting WBA because it’s a good example of a “value trap.” By that, we mean a stock that has the outward appearance of being an inexpensive stock based on conventional valuation metrics. WBA certainly fits that. It’s going for seven times this year’s earnings, but it’s not a value stock. It’s wildly overvalued once you factor in its legal realities.

Over the last 10 years, the S&P 500 has more than tripled while Walgreens is down by 80%. This is an important lesson for investors. Whenever we see a stock that seems to be going for a low valuation, we need to ask why. There may be a very good reason why.

Don’t Count the Economy Out

We recently got a good jobs report. The government said that the economy created 256,000 net new jobs last month. That beat expectations of 155,000. The unemployment rate fell by 0.1% to 4.1%. The jobless rate has been below 4.3% for the last 38 months in a row.

Last week, the Bureau of Labor Statistics said that inflation increased by 0.4% last month. Despite the higher headline rate, core inflation, which excludes food and energy, increased by 0.2% last month. That was 0.1% below expectations. Over the past year, core inflation is running at 3.2%.

Not too long ago, Wall Street assumed that the Federal Reserve would be slashing interest rates this year. That may not be the case. The Fed meets again next week, and you can forget about any rate cuts coming. The futures market currently thinks there’s a 0.5% chance of an interest rate cut. I think that’s about 0.49% too high, but that’s only a guess.

For the meeting after that, coming in March, futures traders think there’s only a 26% chance that the Fed will cut interest rates. Traders don’t see a cut coming at the May meeting, either. They think the first cut will come in the middle of June.

Remarkably, that’s the only Fed interest rate cut that traders expect all year. This is a huge change in sentiment from just a few weeks ago. If earnings continue to grow as they are now, what’s the point of cutting rates?

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on January 21st, 2025 at 6:45 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His