CWS Market Review – February 11, 2025

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

After a very good 2024, the stock market seems to have settled into its comfort zone. For the S&P 500, that’s apparently anywhere between 6,025 and 6,085. The index has closed inside that narrow range ten times in the last eleven trading sessions.

On Thursday, the S&P 500 closed higher by one-thirtieth of 1%. That means for every $30 you have in the market, you made one penny today.

That’s so small that if the index closed higher by that much every day for an entire year, the total gain would be a little less than 9%. In fact, today’s gain almost perfectly matches the market’s average gain for a single day.

This is a big change from last year when the index steadily marched higher without much pushback.

We’re also not seeing any major undercurrents within the market. Neither value nor growth are leading the way. Large-cap tech has had some good days recently and some lousy ones, but there’s no larger trend at work except the absence of one.

We’re heading toward the back end of earnings season, and so far, this has been a very good earnings season for Wall Street. According to numbers from S&P Global Market Intelligence, the S&P 500 is on pace for Q4 earnings growth of 13.89%. That’s up from 8.71% one month ago.

Of the companies that have reported so far, 76.6% have beaten on earnings and 61.4% have beaten on sales.

So where does this put the Federal Reserve? Traditionally, the Fed has had its fingerprints near the scene of any bear market, but this time could be different.

“We Do Not Need to Be in a Hurry”

“We do not need to be in a hurry.” So said Fed Chair Jerome Powell as he testified before Congress today. In this instance, I think the Fed Chair is exactly right.

The Fed doesn’t need to act swiftly right now since the Fed has already cut rates a few times. That’s taken some of the pressure off the central bank. We also don’t know what the outcome of President Trump’s tariff policies will be, or even how long they’ll last.

Twice a year, the Fed Chairman testifies before members of Congress. I should caution you that watching members of Congress attempt monetary policy is not for the faint of heart. The boring stuff happens in the House or Senate chambers, but the real action is in the committees.

A few years ago, I went to the Senate office building to watch the festivities. I got there early and was able to snag the seat directly before Alan Greenspan. If you like endless jargon, then the Fed testimony is for you.

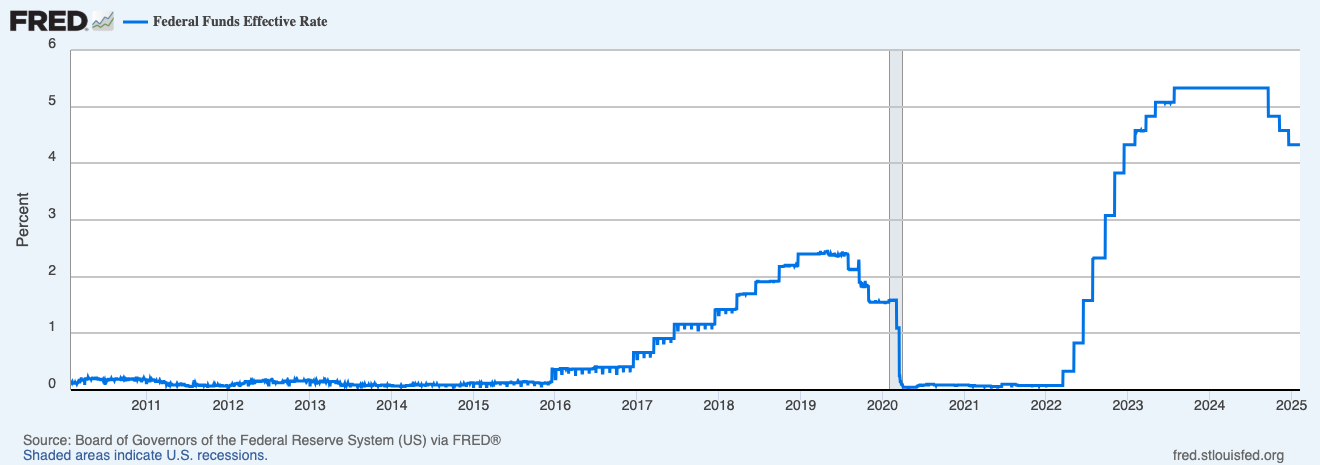

At its last meeting, at the end of January, the Federal Reserve decided to leave interest rates alone. The current range for the Fed funds rate is 4.25% to 4.5%. Before the January meeting, the Fed had lowered interest rates at three successive meetings. The first cut was by 0.5% and the other two were by 0.25%.

So far, there hasn’t been any disharmony between the White House and the Fed. President Trump even said he agreed with the Fed holding rates steady at its last meeting, but that goodwill may not last. Last Friday’s jobs report could lead to calls for more rate cuts.

The Economy Created 143,000 New Jobs Last Month

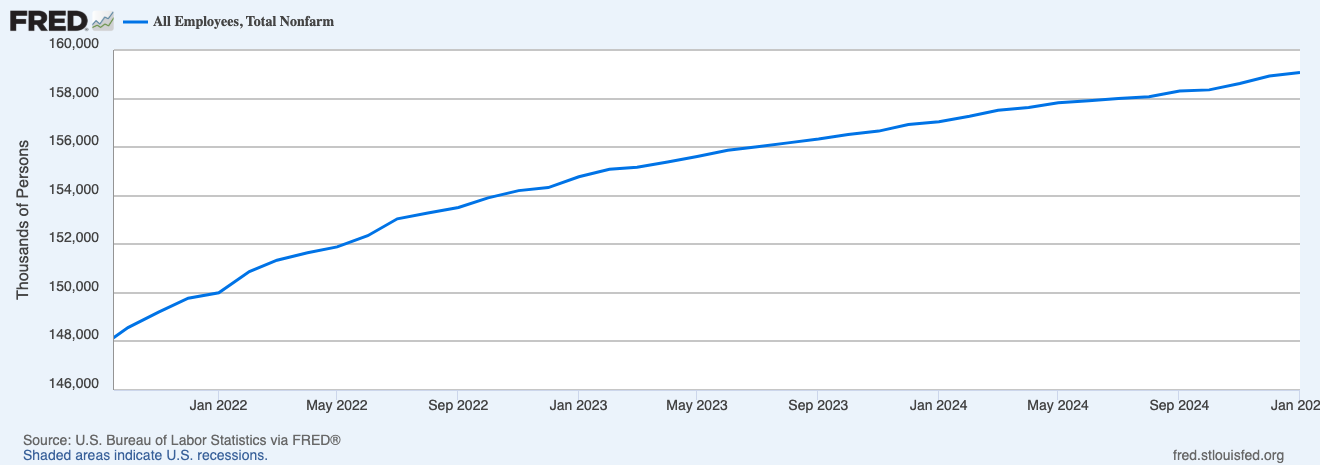

On Friday, the government said that the U.S. economy added 143,000 net new jobs last month. That’s an OK figure, but it’s nothing great. It was below Wall Street’s estimates of 169,000 jobs, and it was also below December’s revised gain of 307,000.

The best news in the report is that average hourly earnings rose by 0.5%. That’s a very nice gain and it’s more than inflation. In previous reports, wages have been rising but only slightly more than inflation. Over the last year, average hourly earnings are up 4.1%.

On a technical note, the Bureau of Labor Statistics did its annual revisions, and that reduced its jobs count for last year. In plain English, they overcounted the number of jobs. We already knew they overcounted, but we didn’t know by how much. It turns out that it was by 589,000 jobs.

Oopsie!

On the plus side, the jobs numbers for November and December were revised higher. The unemployment rate fell to 4.0%. Except for January 1970, the unemployment rate is lower now than it was during the entire 1970s, 80s and 90s.

Job growth for January was concentrated in health care (44,000), retail (34,000) and government (32,000). The total gain for the month was slightly off the average 166,000 in 2024, the BLS said. Social assistance added 22,000, while mining-related industries lost 8,000.

Also, more people are looking for work. The labor force participation rate increased by 0.1% to 62.6%. The broader U-6 jobless rate held steady at 7.5%. There’s really nothing in this report to convince the Fed that it needs to get back to lowering rates, but that could change.

The Fed meets again in another month and it’s very doubtful that they’ll change rates. In fact, the Fed may not make any rate changes for a few months. Currently, traders think there’s a 59% chance of a rate cut by the end of July.

The next big news will come tomorrow when the Fed releases the CPI report for December. This could be a very influential report. The backstory is that inflation came down quickly from its high, but it’s had a hard time falling much below 3% or so. The Fed’s official policy is to get inflation back to 2%.

I’m really starting to question the efficacy of a 2% inflation target. What makes 2% inflation vastly better than 3%? I don’t know the answer.

For tomorrow, Wall Street expects the core and headline rates to have increased by 0.3% last month. That would place the 2024 headline rate at 2.8%, and the full-year core rate at 3.2%. The year-over-year rates have been moving higher in recent months, which must be frustrating for the Fed.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on February 11th, 2025 at 6:38 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His