CWS Market Review – February 18, 2025

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

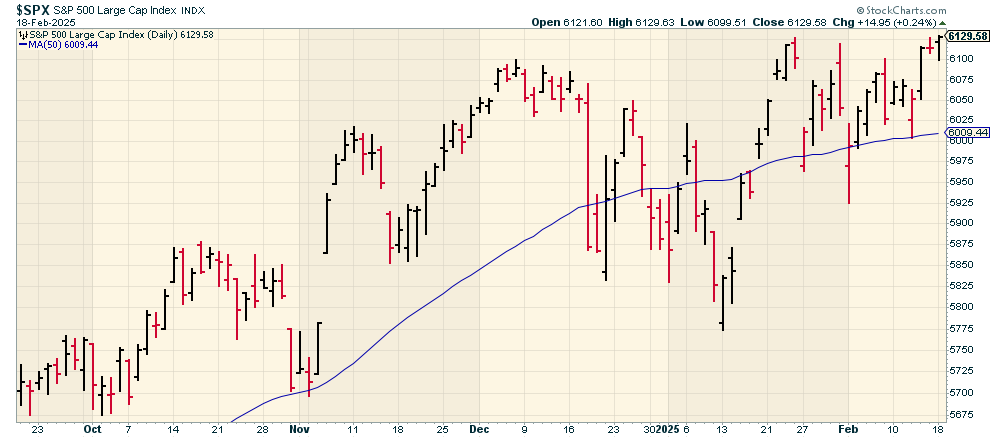

The stock market was closed yesterday in honor of President’s Day. The long weekend wasn’t enough to stop the bulls. The S&P 500 closed Tuesday at 6,129.58. That’s another new all-time closing high.

For any person who’s watched financial markets long enough, you’re struck by how easily the market can rally amid unpleasant news. The old saying is that “the market climbs a wall of worry.”

Think of all the scary news that could have led you to dump all your stocks. Yet, through it all, sitting and waiting was a great strategy.

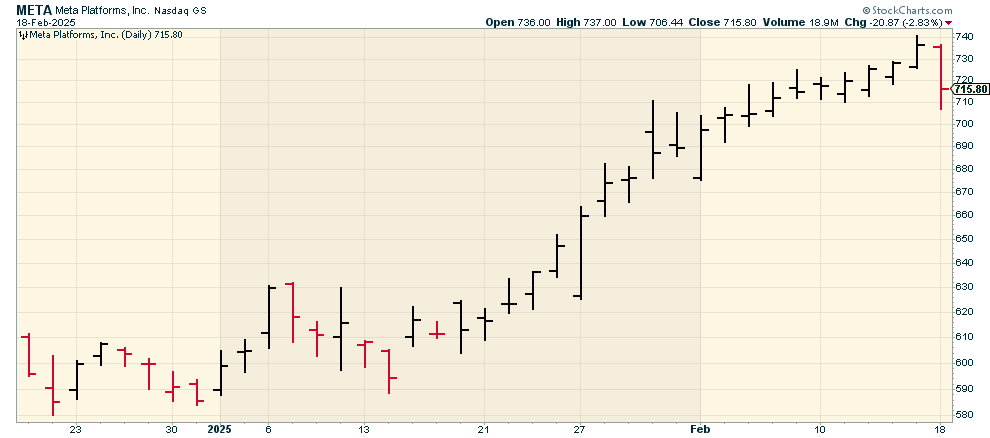

Despite it being another up day for Wall Street, Meta Platforms (META), the parent of Facebook, snapped a 20-day winning streak today. The last time that Meta’s stock closed lower was on January 16. Over that time period, Mark Zuckerberg’s net worth increased by $40 billion.

On January 29, Meta reported Q4 earnings of $8.02 per share. That was 18% higher than Wall Street’s forecast. Check out all those black crosses in a row!

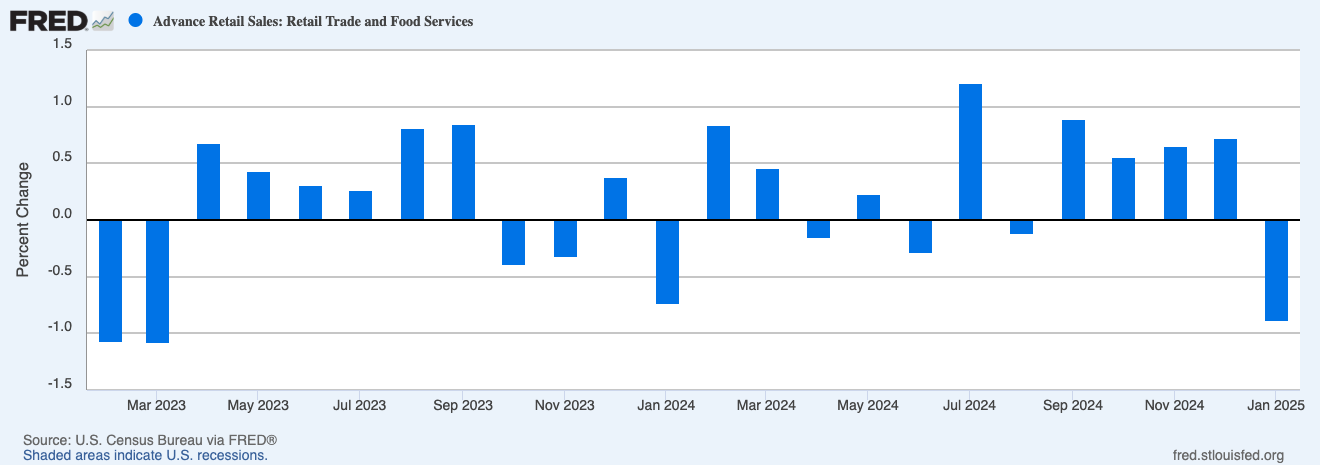

December Retail Sales Drop 0.9%

Wall Street got a big shock on Friday with the latest retail sales report. According to the report, retail sales fell 0.9% last month. Bear in mind, that’s not adjusted for the 0.5% inflation we saw last month.

That retail sales report was much worse than expected. Wall Street had been expecting a modest decline of 0.2%. The number for November was revised to 0.7%.

This suggests that consumers are holding back on their shopping. I can’t blame them. Consumers are getting squeezed by higher prices – eggs are up over 50% over the last year – and also by small wage gains. Consumers make up two-thirds of the U.S. economy. If shoppers aren’t happy, the economy won’t prosper.

Excluding autos, prices fell 0.4%, also well off the consensus forecast for a 0.3% increase. A “control” measure that strips out several nonessential categories and figures directly into calculations for gross domestic product fell 0.8% after an upwardly revised increase of 0.8%.

With consumer spending making up about two-thirds of all economic activity in the U.S., the sales numbers indicate a potential weakening in growth for the first quarter.

Receipts at sporting goods, music and book stores tumbled 4.6% on the month, while online outlets reported a 1.9% decline and motor vehicles and parts spending dropped 2.8%. Gas stations along with food and drinking establishments both reported 0.9% increases.

Some folks are saying the report really isn’t that bad. Some of the drop is due to bad weather. Also, auto sales fell after delivering a big gain in December. Maybe so, but those factors were known prior to the report and it still fell far below expectations.

The retail sales report is especially worrisome because it comes after another bad inflation report. It’s becoming very clear that inflation isn’t going away. Core inflation is holding steady around 3.3% or so, which is much higher than the Fed’s target.

The Budget Deficit Soars

Yesterday, the government said it ran a budget deficit last month of $129 billion. Holy moly, that’s big! The deficit is up significantly from the $22 billion deficit it ran for last January.

It’s not hard to pinpoint the problem. For January, receipts grew 8% to $513 billion, but outlays were up 29% to $642 billion.

The Treasury said there were some technical reasons for the big increase such as benefit payment calendar shifts. Also, payments of $87 billion worth of February benefits were paid out in January. Treasury said the adjusted deficit increase for the month would have been $21 billion instead of the reported $107 billion.

Still, that doesn’t exactly put me at ease. For the first four months of this fiscal year, the U.S. Treasury reported a deficit of $840 billion. That’s up 58% from last year. For the year so far, receipts are up 1% to $1.6 trillion, but outlays are up 15% to $2.4 trillion. For the new fiscal year, individual income taxes are up 6%.

Customs receipts were up 12% but that’s a very small portion of receipts. This doesn’t yet reflect any of the new tariffs on Chinese goods that went into effect recently.

The most concerning number is the interest payments on the debt. You can’t escape those. So far this year, interest expenses are up 10% to $318 billion. Social Security outlays, which is the single-largest item on the budget, are up 8% to $529 billion. Military spending rose 13% to $318 billion.

I try not to be an alarmist on these matters, but if we’re in better fiscal shape, that gives the Fed a lot more room to lower interest rates. The rolling 12-month deficit is now running at 7.3% of GDP. Ideally, that should be cut in half. These deficits are having an effect. Consider that over the last 16 months, the price for gold has gained close to 50%.

Even with the holiday-shortened week, there are still a few things to look out for this week. Tomorrow we’ll get reports on housing starts and building permits. The Fed will also release the minutes of its last meeting. The Fed decided to leave interest rates alone, but it will be interesting to see if the central bank has any broader concerns about the economy.

On Thursday, we’ll get the regular jobless claims report. This data series has held up well in recent months despite the concerns news about retail sales. Then on Friday, we’ll get the report on existing home sales.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on February 18th, 2025 at 6:17 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His