CWS Market Review – March 4, 2025

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Ninety-two years ago today, Franklin Roosevelt was sworn in as president. In his inaugural address, President Roosevelt said, “Let me assert my firm belief that the only thing we have to fear is fear itself—nameless, unreasoning, unjustified terror which paralyzes needed efforts to convert retreat into advance.”

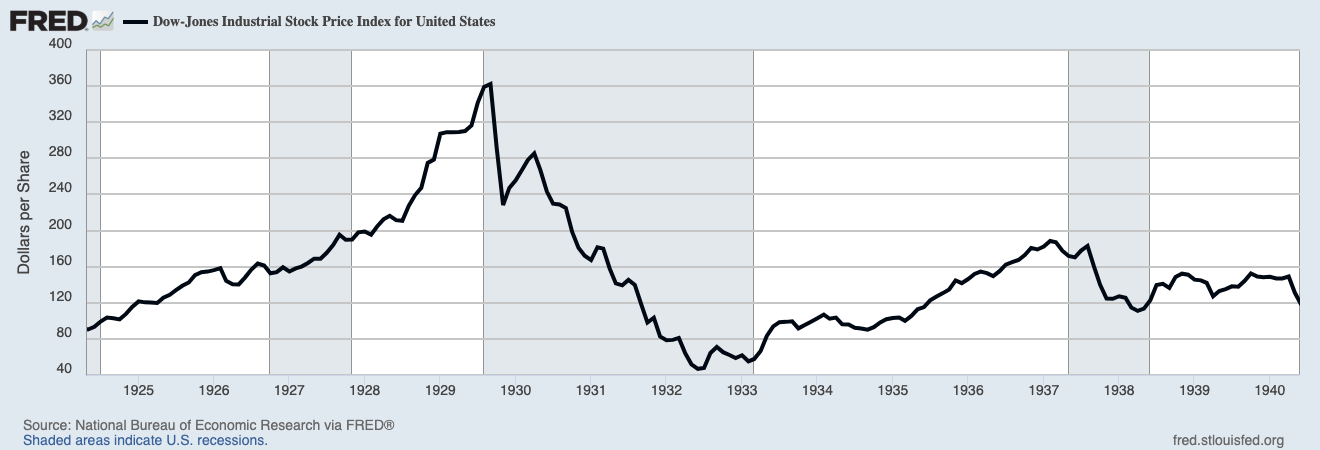

Indeed, fear is a scary thing, and there was a lot to be afraid of back then. The thing about fear is that it can easily lead to more fear, and that will compound on itself. During the Great Depression, the Dow dropped from 380 to 40. The Dow didn’t make a new high for 25 years. That certainly puts our fears of a 10% or 20% pullback into some context.

Back in FDR’s time, the new president wasn’t sworn in until March 4. That wide length and uncertainty between the Hoover and Roosevelt administrations led Americans to move the inauguration date to January 20.

Once he became president, Roosevelt got busy. Thirty-six hours into his presidency, FDR declared a bank holiday. Every bank in the country was shut down. Can you imagine that! Americans couldn’t take their money out, or even put new money in. The government inspected every bank in the country and only fiscally sound banks were allowed to reopen.

On March 9, Congress passed the Emergency Banking Act. The measure was rushed through Congress as quickly as possible. In fact, it was done so quickly that there was only one copy of the bill for the entire House of Representatives.

FDR’s order extended to the New York Stock Exchange. The stock market ended the day of March 3, 1933, at 53.84. After that, all trading was halted. The NYSE didn’t open again until March 15.

The paused worked, and the panic faded. Americans returned more than $1 billion to their banks. The Dow closed March 15 at 62.1, a gain of 15.3%. That was the single-largest gain in market history, and the record still stands today.

But in my opinion, that record deserves a small asterisk. While it’s technically true that March 15, 1933, was the best day in market history, that includes the buildup of nearly two weeks without any trading.

There’s a lesson for investors here. What’s interesting to me is how panic can build on itself, but so can calmness. Once people were forced to stop selling, other people lost the need to sell which, in turn, caused less selling. Sanity slowly returned. As it turned out, the initial problem was fear itself.

The High Beta Correction

That brings us to this week’s panic. Actually, panic is too strong a word, but the financial markets are certainly not happy. The stock market fell for the eighth time today in the last nine sessions, and five of those drops were by more than 1%.

The S&P 500 has now wiped out its entire gain since the election. That’s a loss of $3.4 trillion. The combined loss truly is not that much (about 6%), but it comes on the heels of a very placid time for the market.

The market could be in worse shape than it superficially appears. For example, 70% of the stocks in the S&P 500 are down over 10% off their 52-week highs. More than 38% are down more than 20%. It’s as if there’s a stealth bear market that’s quickly taking out some of Wall Street’s favorites. Tesla, for example, is 44% below its 52-week high.

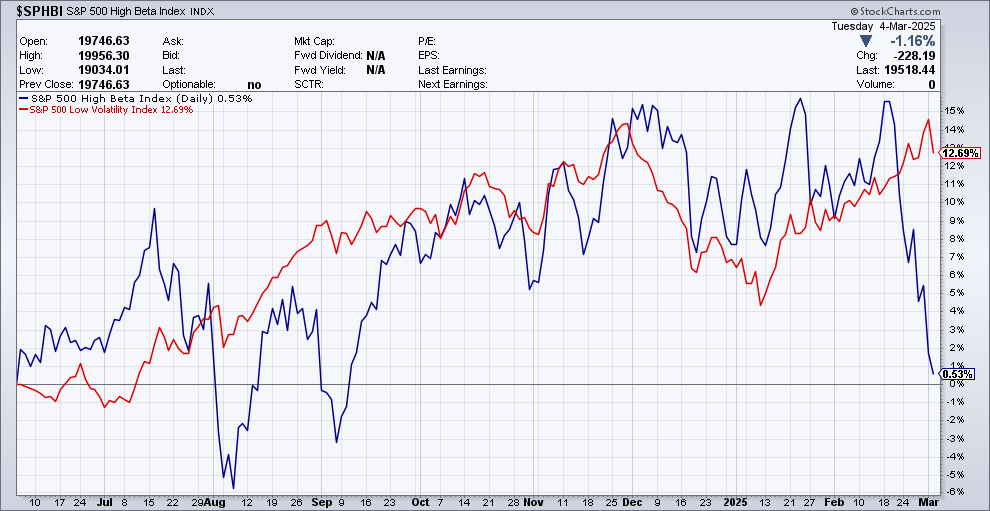

I’ve mentioned this before, but it bears repeating. The selling is falling disproportionally on riskier stocks. Low risk stocks have barely been hit.

Here’s a chart of the S&P 500 High Beta Index (in blue) along with the S&P 500 Low Vol Index (in red):

Notice how sharply the blue line has fallen. The chart above is a good way of seeing how the market swings between fear and greed. See how stable the red line is in comparison. The same effect is happening between value stocks and growth stocks. The Nasdaq Composite is down 8.7% since February 14.

There are sound reasons for the market to get more conservative. At the top of the list is the escalating trade war between the United States and Mexico and Canada. The tariffs are set to go into effect at midnight tonight. Last year, the United States had imports worth $1.4 trillion from Canada, China and Mexico.

According to the New York Times, “All goods imported from Canada and Mexico are now subject to a 25 percent tariff, except Canadian energy products, which face a 10 percent tariff, according to the executive orders.”

We’ve also been getting a raft of softer economic news. For example, the Atlanta Fed’s GDPNow model now estimates that the U.S. economy shrank at a 2.8% rate during Q1. Just a few days ago, the model was forecasting 2% growth. We also learned that in January, construction spending fell by 0.2%. The ISM Manufacturing Index fell to 50.3. That still indicates a growing factory sector but not by much.

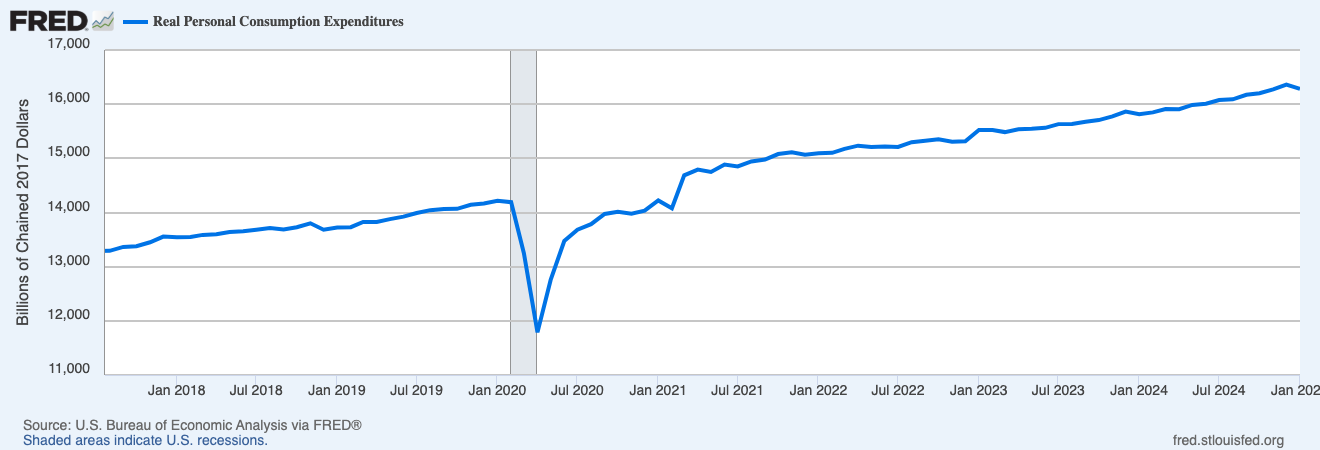

Last week, the government revised its report on Q4 GDP growth to 2.3%, but the shocking news came with the personal income report. That usually comes out the day after the GDP report. For January, personal income rose by 0.9%, but spending (officially called “personal consumption expenditures”) fell by 0.2%.

Here’s a look at real PCE, which means adjusted for inflation. That little dip at the right is what freaked out Wall Street. I’m not concerned about one or two bad months, but I don’t want to see a bad trend develop here.

President Trump will be speaking this evening. Early reports suggest he’ll be talking about Ukraine and his tariff policies.

This Friday, we’ll get the jobs report for February. Wall Street expects to see a gain of 170,000 net new jobs. I’ll be curious to see if that number is as strong as expected. In January, only 143,000 jobs were created which was below expectations. The unemployment rate is expected to be 4.0%.

If the jobs numbers are bad, it could convince investors that they were right to exit High Beta stocks.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on March 4th, 2025 at 4:19 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His