Posts Tagged ‘WFC’

-

CWS Market Review – January 16, 2015

Eddy Elfenbein, January 16th, 2015 at 7:09 am“There’s no shame in losing money on a stock. Everybody does it.

What is shameful is to hold on to a stock, or worse, to buy more

of it, when the fundamentals are deteriorating.” – Peter LynchThe stock market has suddenly gotten a lot more volatile. We went all of 2014 without a losing streak of more than three days. Since Christmas, we’ve had two five-day losing streaks. So far, the U.S. stock market has lost nearly $1 trillion this year.

Last year was the calmest year for stocks since 2006. The average daily change for the S&P 500 in 2014 was 0.53%. So far this year, we’re running at more than twice that. If you recall, the S&P 500 had a three-month stretch last year when it didn’t close up or down by more than 1% in a single day; but in the last five weeks, it’s happened eight times. On Thursday, the S&P 500 closed below 2,000 for the first time in a month. This is the index’s worst start for the year since 2009.

So what’s behind the market’s vicissitude? There are several events coming together, but most of them are a result of our good friend, the Strong Dollar Trade. I’ve written about this before, but every investor needs to understand what this means. Just this week, the euro slumped to a nine-year low against the dollar. The Swiss National Bank responded by scrapping the franc’s price cap against the euro. All over the globe, forex trading went bonkers. Within minutes, the franc skyrocketed 38%.

The rising dollar is putting a lot of pressure on commodities which are priced in dollars. On Tuesday, spot West Texas Intermediate broke below $45 per barrel. Then on Wednesday, copper plunged 5.3% for its biggest loss in nearly six years.

Underlying the Strong Dollar Trade is the belief that the U.S. economy is semi-strong while Europe and Asia are weak. But our economy might not be as healthy as we thought. We just learned that last month’s retail sales were the weakest in a year. This week marked the beginning of Q4 earnings season, and we’re starting to see how the soaring greenback has impacted different companies.

Confused? Don’t be. I’m pleased to report that our Buy List is well-positioned for whatever the market throws our way. In this week’s CWS Market Review, we’ll take a closer look at the earnings outlook and what it means for us. We’ll also break down the latest ructions in Europe. Later on, I’ll discuss the latest earnings report from Wells Fargo ($WFC). The big bank is doing well in a challenging environment for banks. I’ll also preview upcoming Buy List earnings reports from eBay and Signature Bank. But first, let’s take a look at how the Strong Dollar Trade is impacting the world.

Looking at the Fourth-Quarter Earnings Season

The Q4 earnings season has officially begun. This is an important earnings season because it’s our first look at how the plunge in oil has affected the corporate bottom line. In the weeks leading up to earnings season, analysts had been slashing their estimates, especially for energy stocks.

In October, Wall Street had been expecting earnings to rise by 8.5% for Q4 and by 9.5% for Q1. That’s been pared back a lot. The Street now expects earnings growth of 2.0% for Q4 and 2.8% for Q1. As you might guess, energy is mostly to blame. From the end of June to the end of December, full-year 2015 earnings estimates for energy stocks dropped by 28.9%. For the rest of the S&P 500, estimates dropped by 1.5%. Actually, that probably understates the impact of energy, since the mega-caps like Chevron ($CVX) and Exxon ($XOM) aren’t down nearly much as many of the small- and mid-cap energy stocks.

The irony is that if OPEC hadn’t been so greedy and let oil shoot over $100 per barrel, then no one would have put so much money and effort into fracking or horizontal drilling. It’s now a game of who’s going to blink first, the shale guys or OPEC. All across Wall Street, oil experts are playing a guessing game of “how low can it go.” Goldman said that oil will have to be near $40 to fend off new supplies. Bank of America and Societe Generale say that oil’s going below $40. Barron’s speculates that oil could hit $20 per barrel.

AAA said that the average price at the pump is $2.101 per gallon. That’s the cheapest gasoline has been since May 2009. OPEC has shown every sign that they’re cool with this drop and that they’re ready to let oil slide down even more. Neither side is ready to blink. In December, Iraq exported more oil than it had since the 1980s.

As I see it, a black swan is a white swan that got doused with $44 oil. Experts estimate that the supply of crude is outpacing demand by two million barrels every day. The oil bear has put the squeeze on the Russian bear. The situation in Russia is so bad that Mikhail Prokhorov, one of the big-time oligarchs, is selling his majority stake in the Brooklyn Nets. Does plunging oil hurt stocks? We don’t have a precise answer, but previous oil bears have been good for stocks.

We can assume that lower oil is very good for consumers, and that’s been helping retail stocks like Ross Stores ($ROST). But we got a surprise this week from a weak retail sales report for December. Sure, more people are working, but last week’s jobs report showed that average hourly earnings fell in December. There’s also the fear that the oil bust could lead to a collapse in capex spending. That’s a fancy way of saying that energy companies won’t shell out as much money for new projects since oil’s so cheap. That could also lead to layoffs in the energy sector.

The lousy average hourly earnings data may cause the Federal Reserve to rethink any rate-hike plans. The Strong Dollar Trade really overwhelms everything. Wholesale inflation just recorded its biggest drop in three years. Charles Evans, the president of the Chicago Fed, said that inflation may not hit 2% until 2018. Evans doesn’t want to see rates go up until next year at the earliest. He may be right. It looks like the Strong Dollar Trade is already doing its own monetary tightening, beating Yellen to the punch. That’s why the bond market continues to rally. This week, the yield on the 10-year Treasury dipped below 1.80% for the first time since May 2013 (see below). The yield on longer-dated bonds has fallen even more. The spread between the 10- and 30-year yields is at a six-year low.

Wall Street can be unforgiving if a stock misses earnings. On Wednesday, JPMorgan Chase ($JPM), a former Buy List stock, got nailed for a 3.5% loss after the bank missed the Street’s earnings consensus by 12 cents per share. JPM’s legal costs were $2.9 billion last year. I realize that sounds bad, but it’s an improvement over the $11.1 billion from 2013. Bank of America ($BAC) and Citigroup ($C) have also been weak. On Thursday, Best Buy ($BBY) got taken to the woodshed after they warned of tough times ahead. Stryker ($SYK) just said that the strong dollar will nick this year’s earnings by 20 cents per share. The previous forecast was 10 to 12 cents per share.

The real pain lately has been among “high beta” stocks, meaning the stocks that go up the most when the market goes up. Many richly valued Internet stocks like Twitter ($TWTR), Google ($GOOGL), Netflix ($NFLX), Priceline ($PCLN) and Amazon ($AMZN) have been poor performers. Investors should continue to concentrate on high-quality stocks like the ones on our Buy List. Two stocks on our Buy List that look especially attractive right now are Qualcomm ($QCOM) and Hormel Foods ($HRL). Now let’s look at Europe’s fight against slipping into deflation.

Europe’s Battle Against Deflation

Europe can’t seem to catch a break. The economy in the Old World is still flat on its face. Unemployment in the eurozone is 11.5%, and the latest stats show that Europe now faces a real threat of deflation. Mario Draghi, the head of the ECB, recently said, “If inflation remains low for a long time, people might expect prices to fall even further and postpone their spending.” A deflationary spiral is a central banker’s worst nightmare.

Draghi has been fighting intransigent European (read, German) politicians to get behind his efforts to do a large-scale Quantitative Easing, just like Bernanke did, but for Europe. Only since the latest batch of lousy economic stats has he finally prevailed. Like Bernanke, Draghi has cut rates down to nothing, and Europe is nowhere close to the ECB’s 2% target for inflation. Five-year bond yields in Germany, Finland and Switzerland have all turned negative. That means, you have to pay for the privilege of lending the government your own money!

The ECB’s next meeting is on Thursday, January 22, and that’s when Draghi will unveil his stimulus plan. This is part of the reason why the euro’s been tanking against the dollar, and why the Swiss Fed decided to abandon its currency cap (see the crazy chart below). The Swiss National Bank lowered interest rates from -0.5% to -0.75%. Now there’s the question of a price tag for Draghi’s bond-buying. Analysts have been kicking around numbers from 500 billion to 800 billion euros. Some say it could even be one trillion euros. I think Draghi is a very determined guy. Remember, he’s the one who said in 2012 that he’ll do “whatever it takes” to save the euro.

What’s Draghi going to buy? Well, that’s a really good question. His problem is that he’s going to have to buy enough bonds to make an impact, but that will mean he’ll have to buy bonds of more profligate countries, which opens him up to the charges of rewarding poor decisions. My view is that if Draghi has broad enough support from the important people, he can win his fight against deflation.

Europe’s problems don’t end there. On January 25, the Sunday following the ECB meeting, Greek voters go to the polls. The far-left Syriza party, led by the charismatic Alexis Tsipras, is expected to do well. Syriza has promised to bail out of Greece’s bailout.

The problem for investors is that that could trigger a nasty chain reaction. Europe lent Greece 240 billion euros in exchange for the government’s implementing austerity policies. Those policies are hugely unpopular. Germany has made it clear that they won’t be blackmailed by Greece, and they’re fine with Greece exiting the euro. This could turn into a massive headache for everyone. Honestly, I don’t see it coming to that, but it’s not a far-fetched scenario. Hopefully, some sort of compromise will be worked out. Now let’s look at the first earnings report from our Buy List this earnings season.

Wells Fargo Earned $1.02 per Share for Q4

On Wednesday, Wells Fargo ($WFC) led off earnings season for our Buy List. The San Francisco bank reported earnings of $1.02 per share, which matched Wall Street’s view. Net income rose slightly from $5.37 billion to $5.38 billion. This was Wells’s 18th consecutive quarter of profit growth.

Wells was much more fortunate than other big banks (like JPM) because they focus more on deposits and lending rather than trading. Looking at the top line, WFC’s revenue rose 4% to $21.44 billion. The Street had been expecting $21.24 billion. Wells clearly benefited from loan growth. Total average loans rose 4% to $849.4 billion. On the downside, Wells said that expenses rose to their highest point in two years.

WFC’s net interest margin (that’s the key metric for any bank) fell a bit to 3.04%. That’s still good. For the whole year, Wells had net income of $21.82 billion on revenue of $84.35 billion. That’s an increase of 4% and 1%, respectively. For the year, Wells earned $4.10 per share.

Overall, I’m pleased with their performance, and I recognize that the environment is less friendly towards banking. Last year, Wells’s return on equity was 13.7%. That compares well with JPM, which had an ROE of 9.8%. So far this year, the S&P Bank Index is down 8.8%, while shares of WFC are down 6.5%. This is why we focus on high-quality companies; they do better when times are rough.

Wells Fargo is also being hurt by a sluggish housing market, but I think that will gradually improve over the next several quarters. The stock got nicked after the earnings report, so this week I’m lowering my Buy Below on Wells Fargo to $54 per share.

Earnings Preview for eBay and Signature Bank

We have two more Buy List earnings reports coming next week. eBay reports Q4 earnings on Wednesday, January 21, and Signature Bank, a new member of our Buy List, reports earnings on Thursday, January 22. (You can see a complete Earnings Calendar for our Buy List stocks

here.)Three months ago, eBay ($EBAY) had a good earnings report. The online-auction house earned 68 cents per share, which was a penny more than expectations. Quarterly revenue rose 12% to $4.4 billion. The report pleased Wall Street. From the October low to the December high, shares of eBay soared 25%.

I was a little disappointed by their guidance for Q4. eBay said they see earnings ranging between 88 and 91 cents per share. Frankly, I think that’s too low. I’m expecting a modest earnings beat. On the revenue side, eBay sees the numbers as ranging between $4.85 billion and $4.95 billion. Again, that strikes me as conservative.

Here’s my view: eBay is a very solid business. Last year, they probably generated more than $3.5 billion in EBITDA. Also, they have more than $15 billion cash in the bank. Of course, eBay also has the PayPal spinoff planned for the latter half of 2015. Revenues at PayPal are growing at more than 20% per year. eBay continues to be a buy up to $60 per share.

Signature Bank ($SBNY) is one of the five new members of our Buy List this year. Signature isn’t very well-known, but it may be the quietest success story in banking. They’re rarely in the news, and that’s exactly how they like it. But their performance tells the story. Signature’s loan-delinquency rate is about one-tenth of the industry average. They also keep a tight rein on overhead, which runs about 40% below industry average.

Three months ago, Signature reported Q3 earnings of $1.52 per share, which was six cents better than estimates. That was their 20th-straight quarter of record earnings. Earnings for Q3 grew by 27.7%. Shares of SBNY have drifted lower recently with other banking stocks. I started Signature with a Buy Below of $133, but I may tighten it up after next week’s earnings report.

That’s all for now. The stock market is closed on Monday in honor of Dr. Martin Luther King’s birthday. Earnings season heats up next week. On our Buy List, eBay and Signature Bank are due to report. We’ll also get important reports on housing starts, building permits and inventories on crude oil. On Thursday, the ECB has its big meeting to introduce its asset-buying program. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

CWS Market Review – October 17, 2014

Eddy Elfenbein, October 17th, 2014 at 7:09 amOur job is to find a few intelligent things to do, not to keep

up with every damn thing in the world.” – Charlie MungerGood advice, Charlie. Unfortunately, every damn thing in the world and then some has been on Wall Street’s mind lately. This has been the most dramatic week for the stock market all year. On Monday, the S&P 500 broke below its 200-day moving average for the first time in nearly two years. That gave the bears a lot more confidence to do more damage.

On Wednesday, the market dropped sharply at the open, then bounced back, then fell even lower, and then rallied even stronger. Remember how laid back and peaceful everything was this summer? Well, not anymore. I guess weird things happen on Wall Street in October. In just one week, the Volatility Index (VIX) doubled. At one point on Wednesday, the S&P 500 got as low as 1,820.66, and the Dow fell below 16,000.

As febrile as the stock market was, the bond market was even crazier. The yield on the ten-year Treasury fell below 2% this week. At one point on Wednesday, it dipped below 1.9%. At the start of the year, the ten-year was yielding 3%. (Note that this will eventually be a big help for the slumbering housing market.)

What’s causing the market to be such a drama queen? That’s simple. It’s the three E’s—earnings, Europe and Ebola. Some are real concerns (like Europe), and some are not (like Ebola). I think traders saw an opportunity to panic since everything had been so calm for so long. It was probably the dramatic impact of the strong dollar that first unnerved traders. Then once Ebola came into the news, they had their chance to panic, and they took it. Beware: Bearish sentiment can be spread through the air—or even by casual contact.

As usual, we don’t pay attention to the madding crowd. Instead, we focus on facts, and that means earnings. This week, we got three decent earnings reports from our Buy List stocks, although the guidance was fairly tepid. I’ll run through the details in a bit. I’ll also preview six Buy List earnings reports coming our way next week. We’re heading right into the heart of earnings season. But first, let’s take a closer look at the three E’s.

Riding out the October Storm

I’m not a close follower of chart patterns or technical analysis, but I do like to keep an eye on the stock market’s 200-day moving average. This is simply the average of the S&P 500 over the last 200 trading days (roughly ten months).

I’ve crunched the numbers, and it’s true: the S&P 500 does much better when it’s above its 200-DMA than when it’s below it. Since 1933, the S&P 500 has averaged an 11% annualized gain when it’s sitting above its 200-DMA, compared with a 1% annualized loss when it’s below.

Why does the 200-DMA seem to work? I think it’s a good example of a dumb rule that works well for complex reasons. The stock market tends to be very sensitive to trends. Once it gets going in one direction, it tends to stay there. The hard part, of course, is picking the turning points. These can be sharp and unexpected. The 200-DMA seems to capture the sweet spot in that it’s long enough to identify the trend, yet short enough to capture turning points.

You can see how going below the 200-DMA changed sentiment by looking at what happened on Thursday. We got the best initial jobless claims report in 14 years. It was the second-best report in 40 years. Yet traders continued to panic over the Ebola news. I’m certainly no expert in public health, but those who are continuing to maintain this hysteria are absurd.

As we know, the market likes to sell first and ask questions later. For example, airline stocks have plunged in response to Ebola. Shares of Southwest Airlines (LUV) dropped 20% in less than a month. Clorox (CLX) said that sales of disinfectants are up 28% in the last month.

I think the market’s panic reached a peak on Wednesday when the Volatility Index hit 31. I expect to see this slide downward next week. This may sound contradictory, but the stock market’s most manic phase usually comes before the lowest share prices are reached. For example, Wall Street’s volatility peaked in the fall of 2008, even though stocks continued to meander lower for another six months. Despite the lower share prices, by March 2009, other market measures such as the VIX or the TED Spread had calmed down dramatically. This pattern is very typical.

I wouldn’t be surprised to see the S&P 500 fall to near 1,800 soon, but I strongly suspect that most of the damage has already been done. That’s one of the characteristics of a selloff: Once you realize what’s happening, most of it has already passed. The economy’s fundamentals are quite solid. Q3 Earnings season is still young, but analysts expect earnings growth of 4.8% and sales growth of 4.2%. That’s not blistering, but it’s far from a recession.The strong dollar continues to make its presence felt. The price of oil dropped below $80 per barrel this week. It seems that Saudi Arabia is perfectly willing to let the price fall. They have no intention of cutting back production. Perhaps it’s a challenge to Russia. Perhaps they want to show American shale producers who’s boss. Perhaps they have no choice, since Europe is weak. Whatever the reason, the price of oil is down and may go even lower. That’s good for consumers, but not so good for domestic producers. Americans aren’t used to thinking of themselves as big-time energy producers.

The strong dollar is also putting the squeeze on inflation. James Bullard, the head of the St. Louis Fed, said this week that the Federal Reserve ought to reconsider ending its bond-buying program. Even though the labor market appears to be getting better, workers aren’t getting higher wages. Also, inflation expectations have fallen, and getting inflation up to 2% is the Fed’s target.

Inflation expectations, as measured by the five-year “breakeven” rate, have dropped substantially. Three months ago, the bond market expected inflation to be 1.96% over the coming five years. Now that’s down to 1.37%. I see Bullard’s point, but I don’t think there’s anything like a majority within the Fed to keep buying bonds. But I think it’s very possible that the Fed will hold off on any rate increase until late 2015, or even 2016. The yield on the two-year Treasury is down 20 basis points in the last two weeks. That’s probably the maturity that’s most sensitive to changes in the Fed’s outlook. We’re living in a low-rate world.

Investors shouldn’t get rattled by this latest selling. Although the market is down, the relative performance of our Buy List has improved a great deal this month. That’s because investors flock towards high-quality stocks when things get scary. With Ebola, I urge calm. With Europe, I urge patience. And with earnings, I urge you to focus on quality. Now let’s take a look at our recent earnings reports.

Wells Fargo Earns $1.02 per Share

Wells Fargo (WFC) kicked off earnings season for our Buy List. The big bank reported Q3 earnings of $1.02 per share, which matched expectations. Digging in the details, the bank was helped out by a gain in venture capital and lower-than-expected taxes. Without that, they would have missed earnings. But on the plus side, WFC’s quarterly revenue rose to $21.21 billion, which topped expectations.

Frankly, this is a difficult time for the banking sector, since mortgage activity has dried up. Make no mistake, Wells is doing just fine. They’re the best-run big bank in America. I’m also pleased to see that WFC’s “underperforming” loans are getting smaller. They’re well capitalized and can weather any storm.

Unfortunately, one thing Wells isn’t protected against is a rash of selling. WFC dropped below $46 on Wednesday, which is a very attractive price. The stock is currently going for less than 12 times this year’s earnings. That’s a bargain, but it will take a calmer market for Wells to rally. This is a keeper. Wells Fargo is a buy up to $54 per share.

eBay Drops below $48 per Share

After the bell on Wednesday, eBay (EBAY) reported Q3 earnings of 68 cents per share. That was one penny more than expectations. Three months ago, the online auction house gave us a range of 65 to 67 cents per share, so they’re running ahead of their own guidance. Quarterly revenue rose 12% to $4.4 billion, which was slightly better than expectations.

From the press release:

“Rapidly changing competitive environments in commerce and payments underscore the opportunities for eBay and PayPal and highlight how each business will benefit from the focus and agility of being an independent company,” said eBay Inc. President and CEO John Donahoe. “PayPal had another strong quarter, and its mobile-payments leadership and momentum continued, with mobile volume up 72 percent to $12 billion. PayPal is on track to process 1 billion mobile transactions in 2014. And eBay continues to focus on enhancing its competitive position, improving the experience for buyers and sellers and investing in consumer engagement. As we prepare to separate eBay and PayPal in 2015, our teams are focused on strong execution to ensure each business is set up for long-term success.”

Guidance was blah (to use a technical term). For Q4, eBay expects earnings to come in between 88 and 91 cents per share. Wall Street had been expecting 91 cents per share. The company expects Q4 revenue of $4.85 billion to $4.95 billion. That raised an eyebrow. Wall Street had $5.16 billion.

eBay lowered their full-year revenue guidance to $17.85 billion to $17.95 billion. The old guidance was $18.0 billion to $18.3 billion. They made no comment about full-year earnings guidance, so I’m assuming the previous guidance of $2.95 to $3.00 per share still holds. The stock got sacked for a 4.7% loss on Thursday. That hardly seems commensurate for a company that hasn’t altered its earnings forecast. Stick with this one; eBay is a buy up to $55 per share.

Stryker Is a Buy up to $87

On Thursday, Stryker (SYK) reported Q3 earnings of $1.15 per share, which was a penny ahead of expectations. They had said to expect earnings between $1.12 and $1.16 per share. Like so many other companies, Stryker has felt the impact of the strong U.S. dollar. Unfortunately, Stryker said they expect full-year earnings to be at the low end of their previous guidance, which was $4.75 to $4.80 per share.

That’s still a healthy profit. I don’t get too worried about issues of exchange rates because that can happen to anyone. The good news is that Stryker continues to see organic sales rising by 5% to 6%. For the quarter, revenue rose 11% to 2.39 billion, which beat expectations by $70 million. Stryker is an ideal buy-and-hold stock. SYK is a buy up to $87 per share.

Six Buy List Earnings Reports Next Week

Next week, we have six Buy List earnings reports coming out. Here’s a rundown:

IBM (IBM) is due to report on Monday. Frankly, the company’s business has been rather lackluster of late, but large-scale buybacks have greatly aided Big Blue’s earnings-per-share. Wall Street currently expects Q3 earnings of $4.32 per share. That may be a bit too high, but I want to see how their business units are faring under the stronger dollar.

McDonald’s (MCD) is due to report on Tuesday. The burger giant is working to turn itself around, and that’s taking longer than I had anticipated. On Thursday, the shares hit a fresh 52-week low. Thanks to the lower share price, the yield on MCD is up to 3.78%. The stock is cheap here, but I want to see concrete evidence that things are getting better.

On Wednesday, CA Technologies (CA) is due to report. The company was one of the bright spots last earnings season. Shares of CA jumped after they beat earnings by five cents per share, but the stock hasn’t done well since then. They also touched a 52-week low on Thursday, and yield is now close to 4%. I’m not sure what more the market expects from them.

CR Bard (BCR) will report on Wednesday, and like CA, Bard also had an impressive earnings beat this summer. They raised their full-year guidance by five cents per share at each end. Bard now expects full-year earnings of $8.25 to $8.35 per share. For Q3, they expect earnings to range between $2.07 and 2.11 per share. Bard has raised its dividend every year since 1972. Look for more good news from them next week.

On Thursday, it’s Microsoft’s (MSFT) turn. This will be for their fiscal fourth quarter. Last month, the software giant gave shareholders a gift by raising their dividend by 11%. That shows confidence in their future. MSFT’s last earnings report was a little confusing, since they missed expectations by five cents per share. One problem for Microsoft is that Nokia’s handset business is a money-loser. They need to do something about that. On the plus side, Microsoft’s cloud business is doing very well. Wall Street currently expects quarterly earnings of 49 cents per share. This is our second-best performer on the year.

I’m very curious about Ford’s (F) earnings report, which comes out next Friday. I can tell you right now that the results won’t be very strong, but that’s for operational reasons. Lots of folks are holding off buying new Fords since the company is getting ready to roll out their new aluminum-bodied trucks. The automaker also lowered expectations for this year, but they’ve kept an optimistic outlook for 2015. If Ford is right about next year, the stock is very cheap here. On Wednesday, Ford went as low as $13.28 per share. The stock is currently going for about 8.5 times next year’s estimate. This could be a home run for us, but I want to hear more specifics in the earnings report.

That’s all for now. Stay tuned for lots more earnings reports. You can see our complete Earnings Calendar. Next week, we’ll also get important reports on consumer inflation, plus new and existing home sales. The housing market continues to weigh on the overall economy, but lower mortgages rates may help it turn the corner. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

CWS Market Review – April 4, 2014

Eddy Elfenbein, April 4th, 2014 at 6:58 am“There will be growth in the spring.” – Chauncey Gardiner

T.S. Eliot famously called April “the cruelest month,” but it’s not so bad for the stock market (Eliot himself was a Lloyd’s Bank employee). Since 1950, the S&P 500 has rallied 44 times in April while losing ground 20 times, and recent Aprils have been especially good. In the last eight years, the S&P 500 has averaged over 3% in April.

This April has gotten off to a good start as well. On Thursday, the S&P 500 got as high as 1,893.80, which is yet another all-time intra-day high. I’m not much of a fan of the Dow Jones, but I should note that until this week, the Dow 30 had failed to break its high from December 31. Some bears claimed that this lack of “confirmation” was a bad omen. Well, that mark fell as well. On Thursday, the Dow broke 16,600 for the first time ever.

What’s the cause for the recent rally? That’s hard to say exactly, but I suspect that the cooling-off of tensions in Eastern Europe has helped a lot. Investors were also buoyed by some remarks made by Fed Chair Janet Yellen. We also got some decent economic news this week, and there seems to be some optimism for Friday’s jobs report (as usual, I’m writing this before the report comes out.)

But the next big event for investors is the Q1 earnings season, which starts next week. We already know that crummy weather held back consumers this winter, but it will be interesting to hear what kind of guidance companies have for the spring. In this week’s CWS Market Review, I’ll preview this earnings season. I’ll also focus on two Buy List earnings reports for next week: Bed Bath & Beyond and Wells Fargo. I also have several new Buy Below prices for you. But first, I want to take a look at a question that keeps popping up on Wall Street.

Are We in Another Bubble?

There’s been a lot of loose talk lately about how today is similar to the Great Millennium Bubble. A few days ago, the New York Times ran a story titled “In Some Ways, It’s Looking Like 1999 in the Stock Market.”

Oh, please. This is nonsense. Sure, stock prices have rallied, and yes, valuations are higher, but c’mon, we’re nowhere close to the kind of crazy numbers we saw in the late 90s. Back then, all you needed was a dot-com address, a sock puppet and some clever ads, and presto, investors would throw billions of dollars your way.

Actually, your company didn’t even need to be that fancy. I’ll give you a good example. General Electric ($GE) is about the bluest blue chip you can find. The stock is currently going for $26.23 per share. That’s half of where it was 14 years ago, yet the company is expected to earn $1.70 per share this year. Compare that to 2000, when GE’s bottom line was $1.27 per share. So profits are up 34% in 14 years (not so good), while the stock price is down by 50%. GE’s Price/Earnings Ratio has dropped from 42 to 15. My point is that people have forgotten what a real bubble looks like.

To be sure, there are areas of the market looking bubbly. Actually, to be more specific, it’s areas outside the market that look troublesome. Tech companies are paying some hefty prices for start-ups with little or no revenue.

Last year, Yahoo shelled out $1.1 billion to buy Tumblr. The company has so little revenue that Yahoo isn’t even required to list it in its financial statements. In business jargon, that’s what we like to call “not good.” A few weeks ago, Facebook paid a massive amount, $19 billion, for WhatsApp, a company with 55 employees. I freely admit that I can’t judge the value of enterprise like that, but there seems to be a fear in Silicon Valley of being left behind in this week’s app of the century, so these prices are getting carried away.

But that’s not the kind of investing we’ve been doing, and our stocks haven’t done many mega-deals lately (though Oracle did a few years ago). My advice is to ignore all the silly bubble talk, and let’s focus on what the numbers say.

Breaking down Q1 Earnings Season

Now let’s take at a look at some current numbers and the outlook for Q1 earnings. Last year, the S&P 500 earned $107.30 (that’s the index-adjusted number; to convert to actual dollar amounts, multiple by 8.9 billion). Currently, Wall Street expects the index make $120.04 for this year and $137.20 for 2015. In my opinion, both numbers are too high, but I’ll get to that in a bit.

For Q1, Wall Street currently expects earnings of $27.60. Those estimates have drifted lower over the past several months. One year ago, the Street had been expecting over $29 for Q1. As a general rule, earnings estimates start high and gradually fall as earnings season gets closer, so don’t be alarmed about the reduced estimates. By the time earnings season arrives, estimates are often too low. This is part of a game the Street likes to play. There’s nothing Wall Street likes better than beating expectations, so companies know how to play the expectations game. The current Q1 estimate of $27.60 works out to an increase of 7.1% over last year’s Q1. That sounds about right. I think we’ll probably be at about $28 by the time all the reports have come in.

I also want to touch on an important and often-overlooked point, which is dividends. Payouts have been growing impressively for the last few quarters. Dividends for the S&P 500 grew by 15.1% for Q1. Technically, I should say “dividends-per-share,” because the stock market has been helped by a reduced share count, thanks to stock buybacks.

Over the last three years, dividends are up by 55%. The S&P 500 paid out $34.99 in dividends last year, and I think it will pay out $40 for this year. Going by Thursday’s close, that gives the index a yield of 2.12%. That’s not bad at all, especially in an environment where interest rates are near 0%, and we know they’ll be stuck on the ground for another year.

Instead of the $120 that Wall Street expects in earnings from the S&P 500, I think $115 is a more reasonable estimate. (I don’t know if it will be more accurate, but I think it’s a safer assumption.) That gives the S&P 500 a forward P/E Ratio of 16.4, which is quite reasonable. Historically, more bull markets are upended by deteriorating fundamentals than by excessive valuations. How far the markets fall, however, is usually determined by valuations. As long as profits continue to grow, the stock market is a good place to be.

Is the U.S. Stock Market Rigged?

This week, Wall Street has been buzzing about Sunday’s 60 Minutes segment with Michael Lewis. He was on to discuss his new book, “Flash Boys,” which covers High Frequency Trading. In the interview, Lewis said that the U.S. stock market is “rigged.” I was disappointed to hear him say that. Lewis is a gifted writer, but I’m afraid he drew an overly simplistic narrative for a complicated issue.

Let me put your fears to rest. The U.S. stock market is not rigged. Individual investors have no reason to fear that a bunch of super computers are ripping them off. There are serious concerns about HFT, but saying that the market is rigged deflects the debate in a pointless direction.

I wanted cover this topic because it’s made so much news on Wall Street this week, including an acrimonious debate on CNBC, and I’m afraid Lewis’s interview rattled investors. The issue with HFT is an issue we often see: technology is changing the way we do business. Some of the changes are good, and some are bad. Instead of having floor traders, guys who make funny hand signals at each other, the modern market is governed by very fast computers. The HFT guys provide liquidity, and they get paid for it. On balance, that’s much better than the system we used to have.

I have concerns about HFT causing more numerous and more severe Flash Crashes, and I like to see that addressed. Fortunately, our strategy isn’t based on trading. I change the Buy List just once a year. I guess you could call us Low Frequency Traders. But I want to assure investors that the U.S. market is not rigged.

Don’t Count out Bed Bath & Beyond

This Wednesday, April 9, Bed Bath & Beyond ($BBBY) will release its fiscal Q4 earnings report. Let me fill you in on the back story. In early January, BBBY cut their Q4 (Dec/Jan/Feb) earnings estimate. They had been expecting earnings to range between $1.70 and $1.77 per share. Now they said it would be between $1.60 and $1.67 per share.

The stock market wrecked the shares. In one day, BBBY plunged from $80 to $70. It continued to fall for the rest of January, and it got as low as $62 per share in early February. If that wasn’t enough, one month ago, the company lowered their Q4 estimates again. This time it was due to the lousy weather. Now they expect earnings between $1.57 and $1.61 per share.

So where do we stand now? I still like Bed Bath & Beyond, and this is why we have a locked-and-sealed Buy List. We didn’t jump ship in a panic, and the shares have started to rebound. Yesterday, BBBY came within a penny of hitting $70 for the first time in three months. I think the market has basically written off the Q4 earnings report and is now focused on their guidance for Q1.

For last year’s Q1, BBBY earned 93 cents per share. The Street currently expects $1.03 per share. I’m going to hold off making a forecast, but I’m still optimistic for BBBY. The company has a rock-solid balance, they’re well run and the recovery in housing is good for them. For now, I’m going to keep our Buy Below for BBBY at $71 per share. Don’t count these guys out.

Wells Fargo Is a Buy up to $54 Per Share

Next Friday, Wells Fargo ($WFC) will be our first Buy List stock to report for this earnings cycle. As I mentioned last week, Wells passed the Federal Reserve’s stress test with flying colors. The Fed also had no objection to WFC’s capital plan, which included a 16.7% increase to their dividend. Wells now pays 35 cents per share each quarter.

In my opinion, Wells is the best-run big bank in America, and it’s better than a lot of small banks. The shares came very close to breaking $50 this week. Wall Street currently expects earnings of 96 cents per share. My numbers say that’s about right, so don’t expect any major earnings beat. The new dividend gives Wells a yield of 2.81%. I’m keeping our Buy Below at $54 per share.

Six New Buy Below Prices

The recent rally has been very good to us. Through Thursday, our Buy List is up 3.29% for the year, which is ahead of the S&P 500’s gain of 2.19%. Three of our stocks, DirecTV ($DTV), Stryker ($SYK) and CR Bard ($BCR), are already up more than 10% this year. Plus, Microsoft ($MSFT) and Wells Fargo ($WFC) aren’t far behind. This week, I’m raising the Buy Belows on six of our stocks.

Two weeks ago, I said that I expected Oracle ($ORCL) to soon break through $40 per share, and that’s exactly what happened. In fact, the stock hit $42 per share on Tuesday. Oracle hasn’t been this high in 14 years. (Remember how the stock dropped after the last earnings report? It’s funny how quickly people forget those short-term reactions.) This week, I’m bumping up my Buy Below on Oracle to $44 per share. I really like this stock.

Ford Motor ($F) has been especially strong lately. Two months ago, the shares pulled back below $14.50, and it recently closed at $16.39. Ford just reported very good sales for March. I’ll repeat what I’ve said before: I think Ford is worth $22 per share. I’m raising my Buy Below on Ford to $18 per share.

Three of our healthcare stocks, CR Bard ($BCR), Medtronic ($MDT) and Stryker ($SYK), broke out to new highs this week. I’m expecting more good earnings news from all of them. I’m raising my Buy Below on Bard to $152 per share. Medtronic is going up to $65, and Stryker’s is rising to $90 per share.

I’ve raised my Buy Below on Qualcomm ($QCOM) for the past two weeks, so I might as well make it three in a row. This stock continues to rally higher for us. On Thursday, QCOM topped $81 per share for another 14-year high. I’m raising Qualcomm’s Buy Below to $87 per share. This could be a break-out star for us.

That’s all for now. First-quarter earnings season kicks off next week. Bed Bath & Beyond reports on Wednesday. Then the big banks start to chime in Friday when Wells Fargo reports. Investors will also be paying attention to the latest Fed minutes, which come out on Wednesday. If you recall, the market was rather confused by Janet Yellen’s press conference. The minutes may clear things up. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

CWS Market Review – March 28, 2014

Eddy Elfenbein, March 28th, 2014 at 8:28 am“Time is your friend; impulse is your enemy.” – Jack Bogle

On the surface, the stock market was fairly subdued this week. The S&P 500 meandered lower, but the overall loss wasn’t so bad. On Thursday, the index closed a hair below 1,850, but let’s not forget that one week ago, we touched an all-time intra-day high.

Beneath the surface, however, there’s been a big shake-up in the market. Specifically, momentum names have faltered while value stocks have taken the lead. This is an important development, and investors need to understand what’s happening. High-profile sectors like biotech have gotten hammered, and former market darlings have been in a world of hurt lately.

Anyone remember a company called Netflix? That stock dropped 14 times in a 15-day span. Since March 4, NFLX is off by 20%. Stocks like Tesla and Priceline are getting dinged as well. Bespoke Investment Group recently noted that the best-performing stocks from last year are the worst performers this year.

In this week’s CWS Market Review, I’ll break down the market’s change of leadership and tell you what it means for our stocks. Speaking of our stocks, we had more good news for our Buy List stocks. DirecTV soared 8% on Wednesday after news of a possible merger with DISH. I’ll have more on that in a bit. Also on Wednesday, the stress testers at the Fed said they have no objections to Wells Fargo’s capital plan, which includes a hefty 16.7% dividend increase.

I’m pleased to see that our Buy List tech stocks are doing well. Oracle and Qualcomm are near new long-time highs, and even slumbering IBM has perked up. Big Blue just touched its highest point in six months, and I think we’ll get a dividend increase next month. But first, let’s look at the big internal shakeup on Wall Street.

The Market’s Big Shift towards Value

An important lesson with investing is that the stock market swings in cycles, and this is not just the overall market, but also within the market. For example, economically cyclical stocks will lead for a few years and then lag for a few more. Financial stocks will blossom, and then another year it will be dividend stocks that blossom. There’s a loose relationship between these cycles, and it’s always dangerous to read too much into the market’s notoriously fickle mood.

In the last month, value stocks have started to lead the market, and growth stocks have been the big losers. What’s interesting is that this has happened during a mostly bullish time for stocks. Typically, we would expect value stocks to do well when the overall market is suffering. Then, as the bull market starts to age, we would expect growth stocks to come into their own. If you recall, that’s what happened during the late 1990s. What was so arresting about that market wasn’t that value stocks merely lagged—it’s that they got crushed even though growth stocks soared. Back then, the Growth/Value divergence was a yawning chasm.

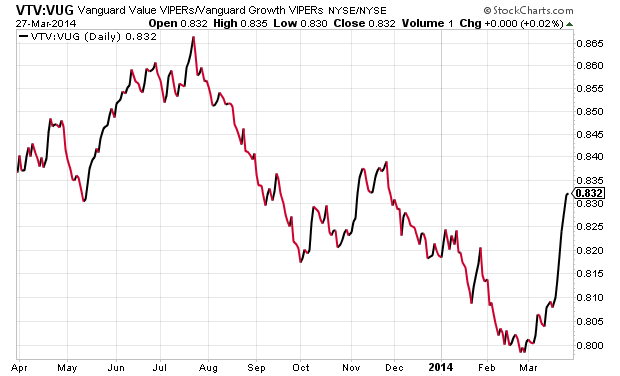

Another interesting aspect about this recent shift to value has been how sharp it’s been. For my Growth proxy, I like to follow the Vanguard Growth ETF ($VUG), and for Value, I look at the Vanguard Value ETF ($VTV). They’re like twin brothers always fighting over mom’s attention. VUG is flashier and has more popular names, while VTV is the quiet, dutiful student. The typical Value/Growth cycle has been distorted in the last few years because the value indexes have been filled with so many toxic financial stocks. (Here’s a chart of the VTV divided by VUG.)

The last Value cycle topped out in mid-2006, and Growth has been in the driver’s seat ever since (with a few false starts for Value). This means that Value underperformed during both the bear market and the bull market. That’s quite a feat. A lot of people have anticipated a Value resurgence, but each attempt has failed. Or I should say each attempt so far.

Since February 27, VTV is up 1.08%, while VUG is down 2.73%. That may not sound like much, but within the ongoing battle between Value and Growth, that’s a major short-term move, and it may continue for some time. VTV has beaten VUG for the last seven days in a row, and 10 of the last 11.

So What Does This Value Shift Mean?

When the market moves towards Value, it typically means that investors are nervous and seeking safety in cheaper names. This time around, it’s not so much that investors want Value. No, it’s that they’re fleeing Growth. An orderly exit is turning into a mad dash. Probably the best example of this has been with biotech stocks. The main Biotech ETF ($IBB) has dropped sharply over the past month. Since February 25, the IBB is off by 13.6%, and a lot of biotech names are down much more than that. Of course, we have to remember that biotech had been in an astounding rally over the past two years.

“So the last shall be first, and the first last” is a quote from the Bible, but it also could serve as a recent stock market report. Look at Tesla ($TSLA), a high-flyer which could do no wrong. The stock went from $35 one year ago to as high as $265 last month. But the past few days have been a different story. Tesla is currently 22% off its high. On the flip side, look at boring Long-Term Treasuries ($TLT). They’re supposed to be dead money, right? But the TLT is at its highest level in eight months. When the current shifts, it can be rough.

I also think the market’s shift towards Value is a reflection of what I talked about last week—investors are getting prepared for the probability of higher short-term interest rates. Last week, the bond market woke up to this idea, and the shift to Value is the stock market’s turn.

Overall, the renewed emphasis on Value is a benefit for our Buy List. In the short term, some of the prominent growth stocks like Cognizant Technology ($CTSH) have suffered in the backlash. I don’t expect that to last. Now let’s take a look at some recent Buy List news.

Wells Fargo Raises Dividend 16.7%

Last week, the Federal Reserve said that Wells Fargo ($WFC) aced its most recent stress test. I had no doubts they’d pass. It’s hardly a secret that WFC is one of the best-run big banks around.

The second part of the Fed’s test came this week to see if they’d approve their capital plans. Once again, Wells Fargo easily passed. The Federal Reserve said they had no objections to WFC’s capital plans. That includes a 16.7% increase in their dividend. The quarterly payout will rise from 30 to 35 cents per share. Last week, I said that I was expecting an increase but only of two cents. Shows what I know!

The shares jumped after the announcement. Using the new dividend and going by Thursday’s close, Wells now yields 2.85%. The board also approved a 350 million-share increase in their buyback plan.

By the way, this stress test wasn’t a cakewalk. Zion’s failed, and Citigroup’s dividend request was shot down. Six years after Bear Stearns collapsed, Citi still pays a quarterly dividend of one penny per share even though Wall Street expects them to earn $5.78 per share next year. Citigroup is still a mess, and I’m glad we have a top-tier name like Wells Fargo. Look for another good earnings report in two weeks. WFC remains a very good buy up to $54 per share.

Will DirecTV Merge with Dish?

On Wednesday afternoon, news broke that the CEO of Dish Network ($DISH) had spoken to the CEO of DirecTV ($DTV) to talk about a possible merger. Honestly, this isn’t a big surprise. Folks have talked about a merger between the two for years. In fact, they tried to merge 12 years ago, but the Federales blocked it. Today, I think DTV is the stronger company, but I have to give credit to Dish for holding its own.

Clearly, the recent merger announcement between Time Warner Cable and Comcast has changed the game, and the two satellite guys have to start thinking seriously about their future. A merger makes sense, but at what price? That’s hard to say. I think DirecTV holds the upper hand here, and it’s interesting to note that Dish’s CEO made the call. Still, DirecTV would be wise to consider an offer. DirecTV has 20 million subscribers, while DISH has 14 million (check out the amazing growth of DTV below).

A lot of this will depend on how regulators rule on the Comcast/TWC deal. If the Feds say yes to that, it will be hard for them to say no to the Direct/Dish deal. DirecTV’s CEO, Mike White, has seemed hesitant about a deal, but he hasn’t ruled it out. I think that’s the right attitude. Frankly, I think these two will get together at some point. I just don’t know when.

The immediate benefit of the merger talk is that shares of DTV jumped as much as 8% on Wednesday, although the stock pulled back as the excitement wore off. DirecTV remains an excellent buy up to $84 per share.

New Buy Below Prices

I want to update a few of our Buy Below Prices. IBM ($IBM) has been doing well lately. This week, the shares got above $195 for the first time since September. I’m expecting a dividend increase from Big Blue sometime next month. I’m raising my Buy Below to $197 per share.

On Thursday, Qualcomm ($QCOM) closed at another multi-year high. The company raised their dividend by 20% just a few weeks ago. This week, I’m bumping up my Buy Below to $83 per share.

CR Bard ($BCR) has been one of our top performers this year. I’ve already raised my Buy Below on BCR a few times, and I’ve purposely held off in the past few weeks. With the Q1 earnings season just around the bend, I feel more confident in BCR’s outlook. Bard has beaten earnings for the last six quarters, and I think they’ll do it again. I’m raising my Buy Below on BCR to $147 per share.

I’m keeping my Buy Below for Microsoft ($MSFT) at $43 per share, but I wanted to highlight the CEO’s plans for the company. For the first time in years, investors are optimistic for MSFT. Keep watching this story – it’s going to get better.

Two of our tech stocks have had a rough month: CA Technologies ($CA) and Cognizant Technology Solutions ($CTSH). I still like both stocks, but I want my Buy Below to better reflect the market’s current judgment. I’m lowering my Buy Below on CA to $34 per share, and I’m lowering Cognizant to $52 per share. Going by Thursday’s close, CA’s dividend works out to 3.28%. Both stocks are very good buys.

That’s all for now. The first quarter ends on Monday; after that, we’ll get our regular beginning-of-the-month reports. ISM comes out on Tuesday. The ADP jobs report comes out on Wednesday. Then on Friday, the government releases the big jobs report for March. With the Fed committed to tapering, I actually think the monthly jobs reports aren’t quite as important as they were last year. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

CWS Market Review – March 21, 2014

Eddy Elfenbein, March 21st, 2014 at 8:56 am“…something on the order of six months.” – Janet Yellen

With those words, the new Fed Chairwoman sent world markets into a tizzy. How could that be, and what, pray tell, did she mean?

Fear not, gentle reader, for I am well versed in the convoluted sub-dialect of Fed-speak, and I’ll lead you through Wall Street’s latest hissy fit. The bottom line, as I’ll explain later, is not to worry. Traders are freaking out over nothing special.

After six painful years, the economy is slowly returning to something approaching normal. Soon, workers will be able to demand higher wages, and consumer prices will rise. This is good news—it’s what we want to happen. A side effect is that we’re soon going to return more traditional monetary policies, and that will apparently take some getting used to. In this week’s CWS Market Review, I’ll explain what you need to know.

I’ll also walk you through the latest earnings report from Oracle. The bottom line number was a tad disappointing, but that was more than made up for by rather rosy guidance. I expect the enterprise software giant soon to hit $40 per share, which it last touched 14 years ago. I’ll break it down in a bit, but first, let’s look at this week’s Fed meeting and why everyone’s scratching their heads.

The Fed Ditches the Evans Rule

Before I get into this week’s Federal Reserve meeting, let’s back up a bit and explain how we got where we are. When the economy plunged into recession, the Federal Reserve responded by dramatically cutting interest rates in an attempt to cushion the blow and hopefully turn things around. Soon, the Fed got to 0% and couldn’t cut any more. Many of the top economic models said that short-term interest rates should be negative—pay people to borrow money!

The Fed decided the best way to get below 0% was to buy bonds. Lots and lots of bonds. The fancy term for this is Quantitative Easing or QE. They tried this a few times for limited periods, but it wasn’t enough. Finally, they threw up their hands and said, “we’re going to buy bonds until things get better.” Specifically, the plan was to purchase $85 billion each month in Treasuries and mortgage-backed bonds.

The market loved the plan, and stock prices soared. But investors wanted to know: How long would the bond-buying party last? The idea floated by Charles Evans of the Chicago Fed was to lay out a specific unemployment number and say, “we won’t end QE until we hit this number.” The Fed adopted the Evans Rule and said that 6.5% unemployment was their threshold. (The Evans Rule also included 2.5% for inflation, but we’re a long way from that.)

Stock prices continued to climb, and the unemployment rated started to fall. Then some investors got nervous because we were getting close to 6.5% on jobs, but the economy obviously needed more QE. The reason is that so many people had left the workforce, and as a result weren’t counted as part of that 6.5%. In other words, the economy is weaker than that unemployment number suggests. As a result, the belief was that the Fed would soon abandon the Evans Rule (I first mentioned this in January), and that’s exactly what happened this week. The Fed ditched the Evans Rule.

Yellen Confuses the Market

Now that leads us to the next step, and here’s where things get a little complicated. Last June, the Fed signaled that it was planning to pare back on its bond purchases. The market, predictably, freaked out. This was the famous Taper Tantrum. In four months, the three-year Treasury jumped from 0.3% to nearly 1%.

Investors believed, incorrectly, that the entire rally was due to QE, so once that was gone, the market was toast. Not only did they get that wrong, but they completely misjudged the timing of the Fed’s taper decision (to be fair, the miscommunication was mostly the Fed’s fault). Ultimately, it wasn’t until December that the Fed decided to taper its monthly bond-buying by $10 billion. In January, the Fed tapered by another $10 billion, and they did it again this week.

The Fed had said they wouldn’t raise interest rates until they were done with bond-buying. Sure, that makes sense. But now that they’re tapering, here’s the big question: How long will it be between the ending of QE and the first rate increase? In Wednesday’s policy statement, the Fed said “a considerable time,” so when Janet Yellen faced the media at her press conference, someone asked, “Well…what does a considerable time mean?” Her answer was “something on the order of six months.”

The next logical question is, “Six months from when?” Yellen said of QE’s end, “we would be looking at next fall.” That totally confused reporters. Did she mean fall of 2015? Nope, Yellen clarified by saying she meant this fall. Now six months from this fall means…a rate hike next spring? Hold on! That’s earlier than the market was expecting.

As a result, stocks dropped on Wednesday, and the middle part of the yield curve bulged. The three-year Treasury yield rose by 16 basis points, and the five-year jumped by 19 points (the chart above). The two- and three-year Treasuries’ yields reached six-month highs. Utility stocks, which are highly sensitive to interest rates due to their rich yields, took a beating. On the forex market, the yen dropped against the dollar, and that took a 1.5% bite out of AFLAC’s ($AFL) stock during Wednesday’s trading. Gold, which had been doing well, has lost more than 4% this week.

When Will the Fed Raise Rates?

But does Yellen’s timetable make sense? With this latest taper, the Fed will be buying $55 billion in bonds starting with April. Follow me on this. The Fed meets again in April (they meet every six or seven weeks), so presumably another $10 billion taper would bring us down to $45 billion. Then we’d go to $35 billion at the June meeting. For July, we’d be down to $25 billion. Then in September, we’re down to $15 billion.

The next meeting would be on October 28-29. If the Fed wiped out the last $15 billion in one move, that would mean QE wraps up in November, which is indeed in the fall, as Yellen mentioned. But if the Fed tapers by only $10 billion in October, that leaves $5 billion on the table to tapered at the December meeting. That would mean that QE would be done by the end of the year. Counting six months from that, it means we’d see the first rate increase by the middle of 2015. That’s more in line with what the futures market had been expecting.

The market got tripped up by Yellen’s mention of “the fall” and “six months.” So here’s my take: I think this was a rookie mistake by Janet Yellen. I strongly doubt there’s anything close to a majority at the FOMC that thinks interest rates will rise next spring. The economy is getting better, but we still have a way to go, and the CPI numbers are barely moving.

Let’s also bear in mind that we’re only talking about one measly rate increase. On Wednesday, the one-year Treasury yield skyrocketed all the way up to the highest yield in five months—0.15%! For an investment of $1 million, that works out to about $4 per day.

Make no mistake: higher interest rates are like Kryptonite to a bull market. I think the market is paranoid that a hawkish Fed is suddenly going to spring on them. It’s as if they’ve adopted an attitude of “prove to me that you’re going to let me down.” That, combined with a few misstatements from Chairwoman Yellen, explains what happened. Higher rates are truly something to worry about, but for now, they’re still a long way off.

Stocks rebounded impressively on Thursday. In fact, the S&P 500 barely budged between Tuesday’s and Thursday’s close. But we’re in a new world. Investors need to realize that the Fed will tighten at some point. It’s no longer a distant hypothetical. Currently most FOMC members think short-term rates will be at 1% by the end of next year and at 2.25% by the end of 2016. In other words, the Fed Funds rate will still be less than inflation for a good while more.

Let me add one more point. The FOMC’s policy statements have gotten ridiculously long. Dear Lord, they run on and on, with lots of garbage text. Please. Just tell us the basics. A Fed statement should be no more than 300 words. Period.

Oracle Misses Earnings, but Don’t Fret

After the closing bell on Tuesday, Oracle ($ORCL) reported fiscal Q3 earnings of 68 cents per share. This was two cents below Wall Street’s consensus. It was also at the bottom of Oracle’s own guidance. The stock dropped sharply in the after-hours market. But as I said last week, what was more important than the actual earnings report would be Oracle’s guidance for the current quarter.

On the conference call, Oracle said to expect fiscal Q4 earnings to range between 92 and 99 cents per share. The Street had been expecting 96 cents per share, so that left open the possibility of an earnings beat.

On the revenue side, Oracle said it sees Q4 revenues coming in between $11.3 billion and $11.7 billion. Wall Street had expected $11.5 billion. New software sales and subscriptions would range from 0% to 10%. The best news was that hardware sales rose by 8%. That’s Oracle’s first increase since they bought Sun Microsystems four years ago. Total revenue climbed 4% to $9.31 billion, which was $50 million shy of Wall Street’s forecast.

At the start of Wednesday’s trading, shares of ORCL opened down more than $1. Gradually, traders realized that their guidance wasn’t so bad, and Oracle rallied throughout the day. Oracle finally made it into the green and got as high as a 12-cent gain on the day. The rally was later undone by Janet Yellen’s comments, but Oracle moved largely in line with the rest of the market.

Oracle’s business still needs to improve, but I think they’re making the right moves. I expect the shares soon to break $40, which the stock last hit 14 years ago. Oracle remains a good buy up to $41 per share.

Buy List Updates

Our Buy List continues to hold up well. I have a few updates to pass along. Microsoft ($MSFT) closed above $40 per share for the first time since 2000 (notice how a lot of tech stocks are hitting 14-year highs). The software king is planning to release Office for the iPad, and Morgan Stanley had good things to say about their prospects. I’m raising my Buy Below on Microsoft to $43 per share.

The Federal Reserve just completed its latest bank “stress test,” and Wells Fargo ($WFC) passed with flying colors. The Fed wants to make sure that if things go kablooey, the large banks won’t come running back to Uncle Sam for more bailout cash. Since Wells is so well run, there wasn’t any doubt it would do well.

The next part of the Fed’s decision comes next week when they say who’s allowed to increase their dividend. Again, I’m sure Wells will get whatever they ask for. WFC currently pays 30 cents per share each quarter. I’m expecting that to rise to 32 cents per share, give or take. Shares of WFC just broke out to another new 52-week high. I’m raising my Buy Below on Wells Fargo to $54 per share.

Shares of Qualcomm ($QCOM) have been doing well lately. The stock just hit—take a wild guess—a 14-year high. There’s a chance we might get a dividend increase soon. I’m bumping up my Buy Below on QCOM to $82 per share. This is a very good stock.

That’s all for now. Next week is the final full week of the first quarter. We’re going to be getting more economic reports that aren’t tainted by the inclement weather. On Wednesday, the Department of Commerce will release its latest report on durable goods. Then on Thursday, the government will revise the Q4 GDP report. Last month, the original report was revised downward from 3.2% to 2.4%. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

P.S. Do you know the difference between the different types of stock orders? Don’t be embarrassed. Many experienced investors don’t. Check out my handy guide to the different types of stock orders.

-

CWS Market Review – January 17, 2014

Eddy Elfenbein, January 17th, 2014 at 7:12 am“It is not the crook in modern business that we fear, but the honest

man who doesn’t know what he is doing.” – Owen D. YoungEarnings season is finally here. We’ve already had one good earnings report from Wells Fargo ($WFC). The big bank beat earnings by two cents per share, and after a delayed reaction, the shares broke out to a new 52-week high. This week, I’m raising my buy below on WFC (more on that in a bit).

Things are about to get very busy for our Buy List. Next week, we’re due to have six earnings reports including heavyweights like IBM, McDonald’s and Microsoft. In this week’s CWS Market Review, I’ll preview our upcoming earnings, and I’ll break down the results from Wells Fargo.

Looking at this earnings season, the consensus on Wall Street is that earnings rose 4.9% last quarter. That’s kind of blah, but going into this earnings season, there were some serious concerns. Before earnings season even started, there were 95 earnings warnings in the S&P 500, compared with just 15 good-news surprises. But most of those warnings have been about rather minor adjustments. Actually, the market seems unusually sedate. A few times this week, the Volatility Index ($VIX) dropped below 12, which brought the “Fear Index” to some of its lowest levels in the past seven years. Fortunately, the stock market continues to hold up well, and the S&P 500 reached an all-time high close on Wednesday. We edged out the previous high close of December 31 by 0.00108%.

The economic news continues to be mostly positive, with a few bumps. This week, the Federal Reserve released its Beige Book report, which looks at regional economies across the country. The reports were mostly good, and I think we can expect more tapering when the Fed meets again at the end of this month. Janet Yellen officially becomes the new Fed Chairman on February 1.

This past Tuesday, the Census Bureau released the December retail-sales report, which showed an increase of 0.2%. December is obviously a huge month for retail. While the report wasn’t outstanding, economists were expecting a gain of 0.1%. Also, the big increase for November was revised downward from 0.7% growth to 0.4%.

These are important numbers because consumers drive most of the economy. Also, retail stocks have been hit hard this year. I still like our Buy List retailers, Ross Stores ($ROST) and Bed Bath & Beyond ($BBBY). However, their most recent quarterly reports included sales through November, and not the holiday season. Once the dust settles in the retail sector, I expect our stocks to flourish.

Of course, it’s still very early, but our Buy List is already slightly ahead of the S&P 500 this year. We’ve done that despite a horrible start for Bed Bath & Beyond, which is now down over 16% for the year. Ouch! The lesson here is that diversification works. I should also note that you’ll often see the worst stock in your portfolio dropping more than the gain from your best stock. Stock performance tends to be asymmetrical. In plain English, the bad ones are worse than the best are good. That’s a key insight, and ultimately, it’s what makes value investing so effective. Now let’s look at Wells Fargo.

Wells Fargo Is a Buy up to $50 per Share

On Tuesday, Wells Fargo ($WFC) reported fourth-quarter earnings of $1 per share. That beat Wall Street’s consensus by two cents per share. Strangely, the shares initially dropped after the earnings report (yep, we know how melodramatic traders can be). Then on Wednesday, it was as if rationality and math suddenly dawned on everyone, and the nervous traders got squeezed out. Before the closing bell, WFC had rallied to a new 52-week high.

Lesson: Don’t trust the market’s first reaction. Actually, keep a wary eye on the second and third ones as well.

Now that I’ve had a chance to look at the earnings from Wells, I can say that I’m impressed. Net income for Q4 rose 10% over last year’s Q4. For the entire year, Wells’s net income rose 16% to $21.9 billion. This was their fifth-straight record year. Last year, Wells made more money than JPMorgan Chase (sorry, Jamie).

I was particularly impressed with the efforts of CEO John Stumpf and his team to trim overhead. (Notice how good companies don’t wait to cut costs; they’re always looking for excess fat they can cut.) Quarterly revenue dropped 6% to $20.7 billion. For banks, you want to see where their “efficiency ratio” is. That’s a good measure of how well they’re managing their operations. For Wells, their efficiency ratio actually ticked up a bit last quarter. That’s not bad, coming in the wake of lower revenue.

Wells’s mortgage-originations business got shellacked last quarter, but there wasn’t much they could do about that. In that sector, you’re at the mercy of the Mortgage Rate Gods. On the plus side, Wells’s wealth and brokerage business did very well. One big benefit for Wells is that they don’t have the legal bills that many of the other big banks have.

I like Wells Fargo a lot. The bank is going for less than 11 times this year’s earnings estimate. I expect another dividend increase this spring. This week, I’m raising my Buy Below on WFC to $50 per share.

Next Week’s Buy List Earnings Reports

Next Tuesday, two of our big tech stocks, IBM and CA Technologies, report earnings. I want to warn you ahead of time that IBM ($IBM) may fall below expectations. The Street expects $5.99 per share, which could be just a bit too high. I’ll tell you ahead of time not to worry about a slight earnings miss. New additions to our Buy List are often dented merchandise, and Wall Street bears have been out to get IBM. They may not be done just yet. Either way, IBM is a solid value at this price. My take: IBM is a good buy anytime you see it below $195 per share.

Three months ago, CA Technologies ($CA), the shy kid, blew the doors off its earnings report. CA netted 86 cents per share for Q3, which was 13 cents more than estimates. Wall Street expects 71 cents for Q4, which is probably a wee bit too low. There’s also a chance that CA might sweeten its quarterly dividend. CA Technologies remains a solid buy up to $35 per share. I have much love for CA.

Wednesday: Earnings from Stryker and eBay

On Wednesday, we get earnings reports from Stryker and eBay. If you recall, Stryker ($SYK) raised its dividend by 15% last month. The company missed earnings by two cents in its last report. That was mostly due to currency effects, and I said not to worry about SYK. Indeed, the stock just hit another 52-week high. This time around, Wall Street expects $1.22 per share in earnings, but I’m more interested in what they’ll have to say about 2014. Wall Street currently expects full-year earnings of $4.56 per share for 2014. Stryker remains a very good buy up to $79 per share.

eBay ($EBAY)’s earnings tend to be very consistent. So far this year, their earnings are up 14%. If we apply a 14% increase over the Q4 earnings from 2012 (70 cents per share), that gives us 80 cents per share, which is, not surprisingly, exactly what Wall Street expects. eBay is a very good buy up to $58 per share.

Thursday: Earnings from McDonald’s and Microsoft

On Thursday, we get two more blue-chip earnings reports: McDonald’s and Microsoft.

Three months ago, Microsoft ($MSFT) surprised a lot of folks on Wall Street with an outstanding earnings report. The software giant earned 62 cents per share, which was eight cents more than estimates. Sales rose 16% to $18.5 billion. Microsoft generated sales that were $700 million more than expectations. I think people forget that MSFT is a very profitable company, especially with its business clientele. For the December quarter, the expectation is for MSFT to earn 68 cents per share, which is down from 76 cents the year before. That sounds about right. We should remember that in September, MSFT raised its dividend by 22%. Microsoft is very attractive below $40 per share.

Like IBM, McDonald’s ($MCD) has been rather sluggish lately. This one may take some time before we see solid results. The consensus on the Street is for earnings of $1.39, which is only one penny more than last year’s Q4. The burger giant is coming off a lackluster year, but you should never count Ronald and his friends out. McDonald’s is a good buy up to $102 per share.

That’s all for now. The stock market will be closed on Monday in honor of Dr. Martin Luther King’s 85th Birthday. Next week will be all about earnings. In fact, there’s not much in the way of economic reports. An important note: With these earnings reports, we want to pay attention to forward guidance as much as to the actual results. I think a lot of traders are nervous about this year, especially with the Fed’s tapering plans, so any optimism from companies will go a long way. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

The Credit Card Strategy at Wells Fargo

Eddy Elfenbein, August 6th, 2013 at 12:39 pmHere’s a new look at an old business:

Wells Fargo & Co, the fourth-largest U.S. bank, is trying to grow its relatively small credit-card business with an unusual strategy: appealing to its customers’ distaste for debt.

In 2007, Wells Fargo debuted the Home Rebate Card, which offers a 1 percent rebate that automatically goes toward paying down principal on a Wells Fargo home loan. In the coming months, the bank has plans to roll out cards that provide similar benefits to customers who have taken out student loans, auto loans and other types of consumer debt from the bank.

“The real thing customers wanted was to pay down their mortgage,” Tom Wolfe, Wells Fargo’s executive vice president for consumer credit solutions, said in a recent interview. “That created a thought process where we asked, ‘Why don’t we offer that service for all our products?'”

Wells Fargo believes offering such rewards cards is one of its best bets for boosting the credit card business at a time when consumers remain wary of taking on debt. Outstanding balances on credit cards and other types of revolving debt in the United States have remained flat over the past three years, Fed data show.

Only about one-third of Wells Fargo’s customers carry the bank’s own credit cards – a relatively small number for a bank that controls roughly 10 percent of all U.S. deposits and prides itself on selling customers multiple products. It is ranked eighth among U.S. credit card issuers, with purchase volume of $66 billion in 2012, compared to $566 billion at top-ranked American Express Co and $416 billion at second-place JPMorgan Chase & Co, according to the Nilson Report.

-

CWS Market Review – July 5, 2013

Eddy Elfenbein, July 5th, 2013 at 8:08 am“Do you know the only thing that gives me pleasure?

It’s to see my dividends coming in.” – John D. RockefellerThis will be an abbreviated issue of CWS Market Review. Trading this week was shortened due to Independence Day, and most of the fat-cat Wall Streeters are relaxing at their cribs in the Hamptons.

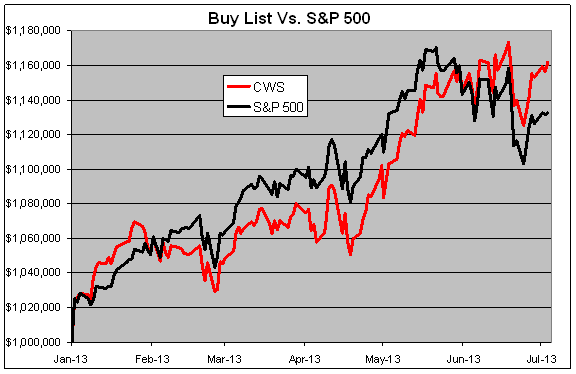

Don’t fear, my friends. My vigilant team and I are still on the watch, protecting you from whatever mayhem comes our way. The good news is that our Buy List continues to do very well. Through Wednesday, our Buy List is up 16.18% for the year compared with 13.27% for the S&P 500. That’s our widest lead all year.

In this week’s CWS Market Review, I’ll discuss the recent good news from Moog and Ford. Both stocks have been big winners for us lately. I’ll also talk about the upcoming Q2 earnings season. JPMorgan Chase and Wells Fargo will be our first stocks to report on Thursday, July 11th. But first, let’s look at why Ford just broke out to a new two-year high.

Good News for Ford and Moog

On Wednesday, shares of Ford ($F) closed at $16.43, which is the automaker’s highest close in 29 months. The catalyst for the move was a very strong sales report for June. Ford reported that sales were up 13% last month. The best news was that sales of F-150 pickups, which are a key moneymaker for Ford, jumped 24%. Ford said that sales in China are up 44% from last year. In May, China sales were up 45%. Ford has been busy playing catch up to GM in China.

Ford is due to report Q2 in a few weeks. The current estimate on Wall Street is for earnings of 36 cents per share, which would be a 20% increase over last year’s Q2. I should add that Ford has been creaming its estimates lately. I like this stock a lot. Ford remains a very solid buy up to $18 per share.

In last week’s CWS Market Review, I raised our Buy Below on Moog ($MOG-A) to $55 per share. That was pretty good timing! This week, Moog said that it’s looking at strategic options for its medical-devices division. That’s Wall Street-ese for “we’re looking to sell it.” I like when companies sell off units, and usually, so do investors. The stock broke $54 on the news, which is an all-time high.

The medical devices unit comprises just 5.7% of Moog’s overall business, but sales were down last year. As much as the market responds to the financial benefits of the divestiture, I think the market appreciates management’s willingness to shake things up. The company is due to report earnings at the end of the month. Wall Street currently expects earnings of 89 cents per share. Moog remains a good buy up to $55 per share.

Second-Quarter Earnings Season Begins Next Week

We’ve heard a lot of talk of how well companies should be doing, but beginning next week, we’ll finally see hard evidence of how well companies have performed. Earnings season is Judgment Day for Wall Street, and we’ll soon learn who’s been pulling their weight and who hasn’t. Fifteen of the 20 stocks on our Buy List ended their quarter on June 30th. This means that three-fourths of our portfolio will report earnings over the next month.