-

Hulbert: What Stocks Do Well from Deflation

Posted by Eddy Elfenbein on September 8th, 2010 at 11:10 amFrom MarketWatch:

By Tuesday’s close, the Dow Jones Industrial Average had fallen 107 points, erasing nearly half of its big gain during the previous session.

But are investors acting rationally when they dump stocks because of deflationary concerns?

Though it would certainly appear that they are, I’m not so sure. The job of a contrarian is to question widely-held assumptions, and the notion that deflation would be bad for stocks is so universally held these days that virtually no one appears to be subjecting it to any critical scrutiny.

One firm that has nevertheless done so is Ned Davis Research, the quantitative research firm. Lance Stonecypher, Senior Sector Strategist for the firm, recently analyzed sector performance during previous periods of significant deflation, both in this country as well as in Japan. Since there haven’t been many such periods, his conclusions of necessity must remain somewhat tentative.

But some fairly consistent themes nevertheless did emerge.

Perhaps the primary conclusion that Stonecypher reached was that, during past deflationary periods, the industry groups that performed the best fell into two categories Necessity and Defensive. Examples include Consumer Staples and Health Care.

Though Ned Davis Research doesn’t provide specific stock recommendations, examples of widely-held stocks in these two industry groups include Johnson & Johnson, Procter & Gamble, PepsiCo, Coca-Cola, and McDonald’s.

Digging further, Stonecypher also found that small-cap stocks have tended to markedly lag the large-caps during deflationary periods. The most pronounced periods of deflation in U.S. history came during the early 1930s, the late 1930s, and immediately after World War II. On average in those three cases, he found, small-cap stocks lagged the large caps by 13% per year.

Finally, Stonecypher suspects that the companies whose stocks perform the best during deflationary periods are those with the lowest debt/equity ratios. This makes sense in theory, he argues, because deflation makes it more difficult for debt to be repaid. (He was unable to confirm this theory, however, since he doesn’t have industry sector debt-to-equity data for the 1930s.)

The bottom line? It is possible to be gravely concerned about the prospects of outright deflation and still invest in equities. If you harbor such concerns but don’t want to give up completely on stocks, you might want to shift some of your equity holdings into the Consumer Staples and Health Care sectors, as well as shunning small-caps in favor of large-cap stocks with the lowest debt-to-equity ratios.During the 1960s and 1970s, stocks like Wal-Mart (WMT) did very well by offering price-conscious consumers a place to go in order to fight inflation. While WMT’s pricing policies are controversial now, the company prospered thanks to its market position during the U.S. economy’s 15-year bout with inflation. The overall U.S. stock market didn’t do well at all.

-

Similar Companies Doesn’t Mean Similar Stocks

Posted by Eddy Elfenbein on September 8th, 2010 at 11:06 amOk class, today’s lesson is on the pitfalls of similar stock performance. It’s tempting to think that all companies in a certain industry group behave the same way. The reason why is that in the short term, they often do.

Once you start following a sector closely, you’ll see that, say, all the major banks will go up or down together on a particular day. In fact, if bad news hits one company, then all of its competitors will behave similarly that day albeit not as much. Oddly, one would think that bad news hitting a competitor would be a positive, but such is often not the case.

I want to bring up the case of the major drug stocks. Here’s a chart of six major drug stocks over the past month. The stocks are Merck (gold), Pfizer (red), GlaxoSmithKline (orange), Abbott Laboratories (yellow), Eli Lilly (blue) and Bristol-Myers Squibb Company (black).

Notice that Lilly is at the bottom and GlaxoSmithKline is at the top. Yet, except for those two the other four are very bunched together. You can even see that the “nooks and crannies” of each line seem to match-up. This is actually a very good example of how the market works.

Let’s say you’re a hedge fund manager and you only have these six stocks to choose from. Since you’re being paid a lot to manage people’s money, you want to stand out from the crowd. As a result, you’re not so much looking for the best investments first, but you’re looking for the least-correlated investments. What attracts you is Lilly falling away at the bottom and Glaxo soaring above at the top.

For the hedge manager, the ideal trade would have been to be long Glaxo and short Lilly—hence the overall line would have been somewhat smooth and this trade probably would have been done with a great deal of leverage. Remember that leverage hates volatility. If you’re leveraged up 20-to-1, then a small 5% decline wipes you out.

Let’s say that you’re a mutual fund manager and you want quick-and-easy exposure to the major drug sector. You can buy an ETF but that makes you look lazy. You can also aim to get one of the four stocks in the middle. That way, you have the exposure and as long as you stay away from the worst performer, you’re fine.

Now let’s take a step back. Here’s the same chart except it goes back to the beginning of 2008.

Now we see a different story. The lines really do separate from each other. The only winning trade is Bristol-Myers, and Glaxo goes from the best stock to the third-best.

The point is that these companies aren’t the same despite near-term correlation. Even after less than three years, we can see major price discrepancies among these stocks. The lesson is that quality wins out, but it does take some time. -

Erin Burnett: “You Have Definitely Gotten My Temper Up”

Posted by Eddy Elfenbein on September 7th, 2010 at 3:51 pmCNBC: First in business worldwide.

-

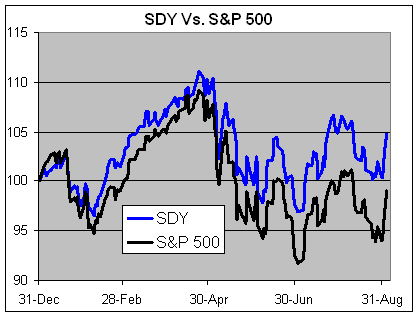

Dividends Are the New Thing

Posted by Eddy Elfenbein on September 7th, 2010 at 1:42 pmAt the end of last year, I was invited to participate in Bespoke’s Roundtable Q&A to discuss investing in 2010. For the question of what the major themes I saw, I said that investors would return to dividends.

Not a major theme, but I expect a new-found love for dividends. A company like GE could easily raise its dividend by 50%. I doubt many money managers will beat the SDY in 2010.

I think I stretched the point about GE’s dividend, although it could use some increasing. But my call on the SDY ETF (SDY) has held up fairly well. That ETF tries to match the S&P High Yield Dividend Aristocrats Index.

Here’s how it’s done versus the S&P 500 this year:

Through Friday, the SDY is up 4.80% for the year, and 5.71% including dividends.

In contract, the SPY is down -0.49% for the year, and down -0.02% including dividends.

Don’t dismiss buy-and-hold so easily. It depends what you buy…and what you hold. -

This Just In….

Posted by Eddy Elfenbein on September 7th, 2010 at 11:18 amThe disparity in the numbers could either mean the market is due for a correction or the recent stock rally will keep going, analysts say.

I particularly like the “analysts say” part.

-

The Guardian Thinks There’s a Chicago Red Sox

Posted by Eddy Elfenbein on September 7th, 2010 at 10:31 amThis is from the Guardian‘s profile of Bob Diamond, the new head of Barclays:

When not at work, Diamond is a fanatical sports fan, supporting Chelsea (football), the Chicago Red Sox (baseball) and the New England Patriots (American football).

I’m guessing they’re inbox is filling up. But who’s more offended; Chicago or Red Sox fans?

(HT: 1440 Wall Street) -

How Much Is a CEO Truly Worth?

Posted by Eddy Elfenbein on September 7th, 2010 at 10:02 amOracle (ORCL) announced that it’s hiring Mark Hurd, formerly of Hewlett-Packard (HPQ). First, I’m glad to see wealthy and powerful people finally land on their feet after a few weeks of unemployment.

But an interesting question is, how much does a CEO really add to a company’s business? When you get right down to it, I don’t believe it’s that much. Steve Jobs, sure. But others, I’m not so sure. I think culture and where the firm and industry are in their life-cycle can also be very important.

By my judgment isn’t what counts, it’s the market’s and Oracle’s market value has increased by $8 billion today. Henry Blodget notes that that’s about half of the $14 billion that HPQ lost when they fired Hurd. -

Russian Finance Minister: People Should Smoke and Drink More

Posted by Eddy Elfenbein on September 7th, 2010 at 9:40 amCan anyone imagine Tim Geithner saying this?

Speaking as the Russian government announces plan to raise duty on alcohol and cigarettes, Alexei Kudrin said that by smoking a pack, “you are giving more to help solve social problems such as boosting demographics, developing other social services and upholding birth rates”.

“People should understand: Those who drink, those who smoke are doing more to help the state,” he told the Interfax news agency.

Alcohol and cigarette consumption are already extremely high in Russia, where 65 per cent of men smoke and the average Russian consumes 18 litres of alcoholic beverages per year, mainly vodka, according to official statistics.If I were cynical, I would say that in America, such a policy would greatly aid our entitlements financing.

Also, I’m not so sure that telling people that something will help the state will urge them to do it. I’ll give the Russian government credit for finally trying to kill its citizens by second-hand means. That’s actually an improvement. -

Good Morning!

Posted by Eddy Elfenbein on September 7th, 2010 at 9:30 amI hope everyone had a great long three-day weekend. The weather was perfect here in DC, lots of sun and not too hot.

On Saturday, I was walking through DuPont Circle and I came across one of the most bizarre protests I’ve ever seen. Living in DC, you get used to seeing people protest some off-beat cause or another, but this one was strange even by DC standards.

I’ll try to present their gripe as best as I can, and I’m using the groups leaflet as my guide. My apologies if I get this wrong, but the document isn’t a great example of clarity. Apparently, a group called Huntington Life Sciences allegedly does horrible things with animal testing. So the group is protesting them? No.

Huntington allegedly got a loan from Fortress Investment Group. So they’re protesting Fortress? No, that’s not it either.

Goldman Sachs allegedly owns a large stake in Fortress. So they’re protest Goldman? Yes…well, sort of.

They’re not protesting at Goldman’s HQ. Nor are they protesting at Goldman’s Government Affairs office in DC, which I’m assuming is their lobbying arm. Instead, they were protesting at the private home of the director of the Government Affairs office.

How this man, or his neighbors, is supposed to stop Huntington’s animal testing isn’t clear. This is the most degrees of separation I’ve ever heard of. I’m now curious if Kevin Bacon ever worked for Goldman Sachs’ Government Affairs unit.

I guess some people will protest anything. -

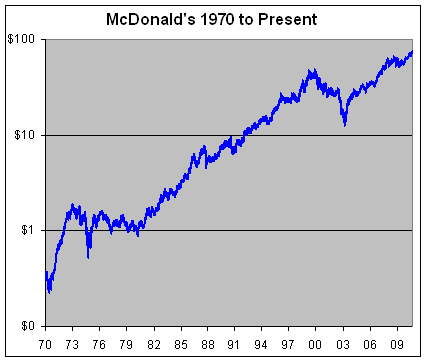

McDonald’s Hits New All-Time High

Posted by Eddy Elfenbein on September 3rd, 2010 at 11:25 amCongratulations to McDonald’s (MCD). The stock just made a new all-time high today of $75.35. That’s not just a 52-week high, or a post-crash high; that’s an all-time high.

Forty years ago you could have picked up the shares for just 29 cents a piece. That’s adjusted for nine stock splits; four 2-for-1s and five 3-for-2s which equals 121.5-for-1. That’s a gain of close to 26,000% or nearly 15% a year, and it doesn’t include dividends.

McDonald’s has done a great job in turning itself around. In 2003, the shares fell to less than $13. Who would have been brave enough to buy MCD then? I sure didn’t!

Check out this numbers: Yearly EPS has jumped from $2.04 in 2005, to $2.45 in 2006 to $2.89 in 2007 to $3.67 in 2008 to $3.97 last year. EPS will probably hit $4.50 this year and the Street is looking for $4.87 next year.

- Tweets by @EddyElfenbein

-

-

Archives

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His