-

The War for Potash

Posted by Eddy Elfenbein on August 23rd, 2010 at 10:39 amIf it’s Monday and it’s 2010, then the market is probably up and wouldn’t you know it, it is! Right now, 19 of our 20 Buy List stocks are trading higher and Nicholas Financial (NICK) is unchanged with just 100 shares traded. Once again, the cyclical stocks are trailing the overall market. I think that’s going to be a major theme going forward.

The big news today is that Potash (POT) has officially rejected the $39 billion buyout bid it got from BHP Billiton (BHP) last week. Now Potash is looking around for a “white knight” to rescue them, but it won’t be easy. Billiton’s bid is $130 per share which is pretty rich. The Street expects Potash to make $5.50 per share this year, so the BHP bid is 23.6 times that. Plus, you know the old saying, “$39 billion in hand is better than nothing in the bush.” Interesting tidbit: In any deal, Potash’s CEO will walk away a cool half billion. That’s not bad for saying “yes.’

What will Potash do? Beats me. Maybe some private equity guys will link up. Maybe the Chinese. Maybe the Brazilians. It’s an open game. I also think Billiton will up their bid just to play nice because they may go hostile.

Honestly, I’m not so interested in who will win but who’s willing to play. I still think that the bond market has far outrun the stock market so we should be seeing more aggressive plays like this. The Potash bid is good for the market and I’d like to see some more players join in.

We saw almost the exact same story three years ago when Billiton went after Rio Tinto (RTP), who had just snagged Alcan. Rio shot down the offer so BHP went hostile. Soon after, the world economy exploded and Billiton threw in the towel. When BHP first made the offer in November 2007, shares of Rio surged from $84 to $103. Today, Rio is at $52. Ouch! -

Another Down Friday

Posted by Eddy Elfenbein on August 20th, 2010 at 1:02 pmThe market is down again on a Friday which has been the trend this year. And once again, the cyclical stocks are leading us lower.

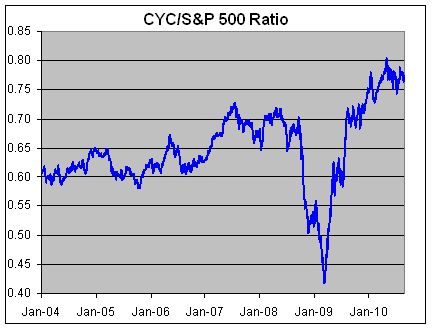

Every so often I like to look at ratio of the Morgan Stanley Cyclical Index (^CYC) divided by the S&P 500. This is a quick-and-dirty way of telling us where we are—or at least where the market thinks we are—in the economic cycle.

As you might expect, this ratio often moves in a cycle. Cyclical stocks tend to lead the market up out of a recession and conversely, lead us lower at the beginning of a recession.

I’ve said before that cyclical stocks, as a whole, probably aren’t a good place to be right now. This graph of the ratio shows how elevated the ratio is:

You can also see how dramatic the ninth-month period was from September 2008 to August 2009. The ratio closed at an all-time high of 0.803 on April 26 of this year, exactly one session after the market’s highest close in nearly two years. Since then, the S&P 500 has given back about 12% while the CYC is off by more than 16.5%. Although I think the broad market will recover, I still believe that cyclical stocks will be laggards. -

Jos. A Bank Clothiers Split 3-for-2

Posted by Eddy Elfenbein on August 19th, 2010 at 6:27 pmThere’s one small housekeeping announcement. Jos. A Bank Clothiers (JOSB) split 3-for-2 today.

For tracking purposes, I assume the Buy List is a $1 million portfolio starting on January 1 of each year. That means all 20 stocks are equal positions of $50,000 each. On January 1, our position on JOSB was 1,185.115 shares at the buy price of $42.19.

With the 3-for-2 split, our JOSB position is 1,777.6725 shares at a starting price of $28.1267. -

Is There a Bond Bubble?

Posted by Eddy Elfenbein on August 19th, 2010 at 12:40 pmLately, there’s been a lot of talk among financial bloggers of a Bond Bubble. There very well could be but the key question is, a bubble relative to what?

Compared with stocks, yes, I think bond yields are far too low. My hope is that stocks will rise to bring the two into better balance. You can think of investing as a perpetual battle between stocks and bonds. Is it better to raise money by borrowing, or taking on new partners? Understanding that key fact is to see how the market works.

The plus of borrowing is that when you’re done renting someone else’s money, it’s over. Taking on new partners never goes away unless you by them out. The negative of borrowing is that you have to pay interest, so whatever you sell, a few pennies in price goes towards paying interest. The positive of equity financing is that there’s no up-front cost.

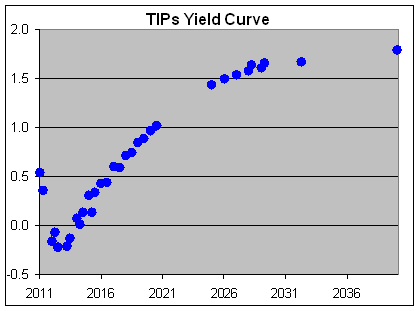

Right now, I believe bond yields are very, very low, even adjusting for inflation. Just look at the TIPs yield curve.

The TIP coming due in July 2010 currently yields just 1% over inflation (or rather, over the CPI). In my opinion, that’s awful.

I don’t, however, believe that bond yields will plummet like dot-com stocks did 10 years ago. Rather, I think investors are unduly fond of the security of Treasury bonds. Sure, they’re safe but that safety comes at a price. One percent real yield for 10 years is too rich for me. The good news is that our massive debt can be financed rather cheaply. -

Intel Buys McAfee for $7.7 Billion in Cash

Posted by Eddy Elfenbein on August 19th, 2010 at 11:39 amThe stock market is down again today, but the big news is that Intel (INTC) is buying McAfee (MFE) for $7.7 billion in cash. In my opinion, this is an awful move. There are so many better uses for that money, like dividends, rather than an acquisition. According to Yahoo Finance, Intel has $18.3 billion in cash which translate to $3.29 per share.

The boards of both companies have unanimously approved the deal, but it’s still pending McAfee shareholder and regulatory approval. Intel said that the deal “reflects that security is now a fundamental component of online computing.” Intel went on to say that security is now just as important to the company as energy efficiency and internet connectivity.

Sure, I don’t doubt how important security is but Intel is paying a gigantic premium. The acquisition price is $48 per share which is a 60% premium over the closing price from yesterday. Think of it this way: MFE was trading at 10.5 times next year’s earnings. Now it’s trading at close to 17 times next year’s earnings.

McAfee will become a wholly owned subsidiary of Intel, and will report to its Software and Services Group. Both companies are based in Santa Clara, Calif. Founded in 1987, McAfee has some 6,100 employees, and saw $2 billion in 2009 revenue , making it the world’s largest security company.

Intel will benefit from McAfee’s entrenched position in the security field, and McAfee may be able to optimize its notoriously performance-hungry software now that it’s a part of the company that provides the CPUs to many computers.

Intel recently announced its best quarter ever with $2.9 billion in profit, thanks to an influx of delayed computer purchases by businesses.Despite all press a mega-deal gets, they rarely work out. At best, they’re a wash. At worst, both firms are hurt. The problem is that deals often look good on paper, but the actual merging of two companies is very hard. There are two cultures, two ways of doing things and two histories. That isn’t given up so easily.

What it comes down to is that I think executives like to lead large organizations. They see “large size” as translating to “good for shareholders.”

I think smaller “fold-in” mergers can work very well, but beyond a certain size, you’re asking for trouble. The frustrating part is that Intel looked so attractive here with lots of cash and a low valuation. -

Lilly’s Dividend Is Holding Strong

Posted by Eddy Elfenbein on August 17th, 2010 at 10:07 amThis hasn’t been a very good year for Eli Lilly (LLY). The shares are down again today on news that it will halt development of semagacestat, a potential Alzheimer’s treatment.

The preliminary tests just weren’t working out. Lilly said that this will result in a Q3 charge of three to four cents per share. That’s bad but not awful.Lilly confirmed its previous 2010 earnings per share guidance range of $4.44 to $4.59 on a reported basis, or $4.50 to $4.65 on a non-GAAP basis (consensus is for $4.61).

As rough as this year has been, Daniel Lee notes that one bright spot has been the stock’s dividend. Lilly currently pays out a 49-cent dividend. That comes to $1.96 per share per share. At the current price of $34.72, Lilly yields 5.6% which is well more than double the 10-year T-bond yield. Lilly has also paid a dividend for the last 125 years. -

The CRA Didn’t Cause of the Crisis

Posted by Eddy Elfenbein on August 17th, 2010 at 9:17 amEric Falkenstein argues that the Community Reinvestment Act didn’t cause the financial crisis but the mindset driving it sure did:

The zeitgeist suggested that lowering underwriting criteria for homeowners was costless, turn renters with their various social and economic deficiencies into homeowners with their various social and economic proficiencies, and be morally just. The mindset that underlay the CRA, not the CRA itself, caused the housing crisis. The CRA was joined by the Fair Housing Act and other explicit legislation. The regulators from the OFHEO, OCC, FDIC, SEC, and Federal Reserve were all on board with the tactics consistent with the strategy, meaning that bankers weren’t criticized for lowering their standards in regards to home lending, but rather congratulated. The US Department of Housing and Urban Development, and Department of Justice had similar objectives and initiatives to those in the CRA. The CRA, in this context, was unnecessary.

That mindset hasn’t gone away. If anything, it’s now spread to education financing.

-

Math Nerds Have Taken Over the Bond Market

Posted by Eddy Elfenbein on August 16th, 2010 at 3:58 pmThe 10-year T-bond just broke below the mathematical constant e — 2.719.

The 30-year is closing in on pi — 3.142.

The 5-year is now below phi — 1.618.

This alignment is unprecedented! Do you have any IDEA WHAT THIS MEANS???

Seriously, do you? Cause I sure as hell don’t. -

Sysco Misses by a Penny

Posted by Eddy Elfenbein on August 16th, 2010 at 1:33 pmAfter opening lower today, the stock market is rallying off its lows. Before the opening bell Sysco (SYY) released earnings for its fiscal fourth quarter. The company earned 57 cents a share which was a penny below forecasts but four cents more than a year ago.

Sysco is a consumer staple so it’s usually good stock to own during a recession. Still, times are tough and the company’s CEO said, “We have seen no consistent pattern of improvement on a week to week basis.”

Looking at the numbers, Sysco is still doing well. Not great, but well enough. For the quarter, revenue rose 14% to $10.35 billion, up from $9.09 billion last year. For the full year, Sysco earned $1.99 per share which is up from $1.77 per share.

Sysco is your classic slow-and-steady stock so I’m not too concerned about it missing earnings by a penny. The company should probably make another $2 a share this year so the current price is a pretty good value. The shares are down about 3% today. -

Will the Dems Dump Pelosi After a Defeat?

Posted by Eddy Elfenbein on August 16th, 2010 at 12:59 pmWith the mid-term election only three-and-a-half months away, I noticed that the Intrade contract for the GOP to retake the House is up to 64.7. Of course, those are just odds but it does mean that “the market” sees a GOP takeover as slightly probably.

I’m curious that if the Republicans do take control of the House, would Nancy Pelosi have to depart as Minority leader? I really don’t care one way or the other but I think it’s interesting scenario, and I’m guessing she would have to depart. Taking your party to parliamentary defeat happens a lot in other political systems but it’s fairly rare in the United States.

For example, after taking his party to defeat this past May, Gordon Brown had to step down as leader of the Labour Party. The party is currently deciding who the next leader will be.

We really haven’t established much of a precedent in the U.S. When the Republicans won the House in 1994, the issue of what former Speaker Tom Foley would do wasn’t an issue since he lost his House seat as well. When the Democrats took control in 2006, former Speaker Dennis Hastert resigned his seat mid-session. But Hastert had already said that 2006 was going to be his last election so he was a lame duck anyway.

When the GOP lost the House in 1954, former Speaker Joseph Martin hung on as Minority leader until the Democrats big victory in 1958. In January 1959, he was ousted by Charles Halleck by a vote of 74 to 70. Six years later, after another big GOP defeat, Halleck was ousted by the Gerald Ford.

I guess that in the U.S. system the “Shadow Leader,” if you will, isn’t an official position although it’s often clear what people are important to listen to and they usually aren’t in the House of Representatives. I remember when Mario Cuomo was treated as the faux Shadow Leader for a few years in the late 1980s. Ronald Reagan held that position for perhaps as long as 15 years. Is Sarah Palin the current Shadow Leader? I really don’t know. But I think having those people outside of the House takes some of the heat, and light, off what the Party Leader does.

- Tweets by @EddyElfenbein

-

-

Archives

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His