-

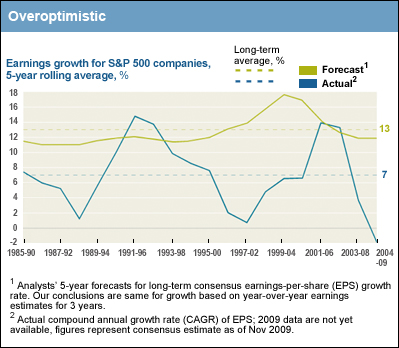

Overly Bullish Analysts

Posted by Eddy Elfenbein on May 17th, 2010 at 4:41 pmFrom the Harvard Business Review:

For the past quarter century, equity analysts’ earnings-growth estimates have been almost 100% too high. Their overoptimistic projections have generally ranged from 10% to 12% annually, compared with actual growth of 6% (excluding the spike in growth from 1998–2001), according to McKinsey research. Only in strong-growth years such as 2003 to 2006 did forecasts hit the mark.

-

Time to Legalize Insider Trading?

Posted by Eddy Elfenbein on May 17th, 2010 at 3:15 pmMatthew Yglesias get his Adam Smith on and questions why insider trading is illegal.

After all, one important function of financial markets is supposed to aggregate information so as to price assets correctly and thus guide the allocation of investment. Excluding informed participants from trading subverts the main goal of financial markets’ existence.

Let me back up a second and explain that insider trading is perfectly legal. All that corporate insiders need to do is declare what trades they make with their own stock, how much and when.

What’s illegal is when corporate insiders trade on “non-public” info. Let’s say the CEO knows that the earnings report is going to be terrible, so she dumps her shares ahead of time.

It’s actually a very murky subject. Even the movie Wall Street gets insider trading wrong. Hard as it may be to believe, Bud Fox didn’t do anything illegal (well…except for theft when he was dressed as a janitor). But the dirt he gave to Gekko wouldn’t be a legal issue because all that information was publicly observable. That’s the key. It comes down to what the public can see and what it can’t. The problem with enforcement is that it makes the government label information.

The libertarian argument is that information is information, and it’s a waste of time trying to label what’s known and unknown. Plus, you get Yglesias’ view that it really doesn’t matter since insider trading goes on anyway. (By the way, has anyone mentioned that the SEC’s case against Goldman Sachs was leaked to the New York Times? This is a scandal twice over—once for the deed and again because no one cares.)

Insider trading reminds of arguments in favor of legalizing black mail. I see their point but, darn it, it just seems…wrong. I would still prefer the companies I own prohibit their executives from trading on non-public information. This, of course, is a non-government solution although it exposes execs to civil lawsuits. The goal should be to make all the non-public information public. -

Math Problems at the WSJ

Posted by Eddy Elfenbein on May 17th, 2010 at 12:05 pmFrom an editorial today:

Taxpayer groups rightly object that the tax hike comes with no spending restraints. Arizona got into this crisis because during the boom years—2003 to 2007—then-Governor Janet Napolitano, a Democrat, and Republicans in the legislature let spending climb by more than 100% to $10 billion from $6.6 billion.

An increase from $6.6 billion to $10 billion is an increase of 51.5% which is just under 11% annualized over four years.

-

Can Things Get Worse for Baxter?

Posted by Eddy Elfenbein on May 17th, 2010 at 10:23 amI like to be upfront about my investing mistakes. Without a doubt, the biggest dud on this year’s Buy List is Baxter International (BAX). Just when I think things can’t get any worse for them, they do:

Biopharmaceutical company Halozyme Therapeutics Inc said it was voluntarily recalling certain lots of its fluid absorption drug, Hylenex, after Baxter International Inc confirmed the presence of small flake-like glass particles in the drug.

On Sunday, Halozyme reported that its development partner Baxter has had “manufacturing failures” in making Hylenex.Baxter is now down -27% on the year for us. The stock is at a new 52-week low and it’s going for about 10 times next year’s earnings.

-

Lowe’s Lifts Guidance But Not Enough for Wall Street

Posted by Eddy Elfenbein on May 17th, 2010 at 10:12 amI recently said that Lowe’s (LOW) and Home Depot (HD) were nearly tied as investments but I gave a slight edge to Home Depot. Lowe’s reported first-quarter earnings this morning and while the results were good and the company raised guidance, it wasn’t as much as the Street hoped for:

The company, based in Mooresville, N.C., said it earned $489 million, or 34 cents a share, in the three-month period ended April 30. In the same period last year the Mooresville, N.C., company earned $476 million, or 32 cents a share.

Revenue rose 4.7 percent to $12.39 billion.

The results handily beat the expectations of analysts. According to Thomson Reuters, analysts expected the company to earn 31 cents a share on revenue of $12.24 billion.

(…)

For the second quarter and full year, Lowe’s said it expects revenue to rise between 5 percent and 7 percent over the prior year and revenue at stores open at least a year to grow between 2 percent and 4 percent. Previously for the year, the company expected sales to rise between 4 percent and 6 percent, and revenue at stores open at least a year to increase 1 percent to 3 percent.

The company expects second-quarter earnings per share to range from 57 cents to 59 cents, shy of the 62 cents a share analysts expect.

For the full year, Lowe’s now expects earnings per share to range from $1.37 to $1.47. Previously it had expected a range of $1.30 to $1.42. Analysts expect earnings per share of $1.45 for the year on revenue of $49.67 billion, according to Thomson.The stock is now down to $24.71 as I write this which works out to 17.4 times this year’s earnings. That seems like a fair price. Lowe’s is neither a screaming bargain nor overpriced. Home Depot reports tomorrow.

-

Exchange Scene in Trading Places

Posted by Eddy Elfenbein on May 13th, 2010 at 3:00 pm

Explanation: The Duke brothers have a false crop report claiming a poor orange harvest. Their trader buys orange juice heavily at the open in an attempt to corner the market before the crop report is announced. At 2:38 Dan Aykroyd and Eddie Murphy start shorting orange juice and all the traders are happy to sell to them. Then the real crop report is announced and it reveals that the orange harvest will be fine. The selling continues. Finally, at 5:18, Aykroyd and Murphy start covering their short by buying. So instead of buying then selling, they sold first and bought later — and kept the difference. -

My Thoughts on Gold

Posted by Eddy Elfenbein on May 13th, 2010 at 1:02 pmA reader writes:

Hi Eddy,

I LOVE your blog…I read it everyday and really enjoy your insights. The key is that you keep it just simple enough as to not get too wonky. Please keep it up.

Question: isn’t it about time to short gold? I’m thinking I’d use a little ETF like GLL or DGZ and just sit on it for a while. With the market doing so well and me thinking that things will be looking up for a while, I’m thinking this a nice little play. Any thoughts? Any risks besides gold continuing on its upward path?This is a good topic and I’ve been getting lots of questions about gold recently. I want to take this opportunity to address the topic and I particularly want to focus on folks who may be new to investing.

If you’re not familiar with investing in gold, it may surprise you that many in the pro-gold camp are—shall we say—not terribly helpful for their cause.

Gold is one of those topics that seems to bring the loons out in full force. A sizeable portfolio of goldbugs see the entire world as corrupt and on the verge of bankruptcy, and gold is their only salvation. You can’t help wondering about the distance between their financial and religious beliefs.

Gold is an endlessly fascinating subject. Gold has been used as a store of wealth for thousands of years. Gold never rusts. I mean never! You can take gold out of an Egyptian pyramid and stick it in your cavity (though you might want to clean it first).

Gold is incredibly soft. One ounce can be stretched for 50 miles. It can be pounded down to a few MILLIONTHS of an inch thickness.

Gold is very heavy. Despite what you see in the Treasure of the Sierra Madre (“Badges? We ain’t got no badges!”) gold dust wouldn’t have blown away.

Gold has been found on every continent on earth. Gold has also had strong religious connections. It’s mentioned in the Bible more than 400 times. Karl Marx writes of commodity fetishism, which is meant to have a religious connotation. And I won’t even get into Freud’s talk of the psychological connection of gold to feces (no, I’m not making this up).

When Moses came down from Sinai with the Ten Commandments, the Jews were making a golden calf to worship. God instructed Moses to overlay a sanctuary for him in pure gold. In other words, gold had its bases covered—it was on both sides!

Plato mentions the gold/silver ratio to be 12. Recent historical evidence suggests that Isaac Newton was mainly an alchemist. The other stuff he did was just playing around on the side, and was probably an offshoot of his efforts to makes gold. Pieces of his hair have traces of lead and mercury.

Newton was also Master of the Mint and inadvertently put England in the gold standard. This means that one of the greatest geniuses in human history was also a civil servant who made economic policy based on a forecast. A forecast that was dead wrong.

In the 1964 film, Goldfinger, Auric Goldfinger plans to irradiate all the gold in Fort Knox thus increasing the value of his gold. He would have been a lot better off doing nothing, since gold increased dramatically over the next 16 years.

There’s more gold at the New York Fed, waaaay below 33 Liberty Street, than in Fort Knox. Gold is also a really good conductor. So despite its high prices, it’s used in many electronics.

What you need to understand about investing in gold is that you’re not really investing in gold. You’re investing against the U.S. dollar. It’s not that gold goes up, it’s that the value of a dollar goes down.

Actually, it’s even more subtle than that. What you’re doing is you’re betting against the interest rate on the dollar. I know this sounds odd, but any currency you carry around in your wallet has an interest tied to it. That’s essentially what the currency is—that rate—and it’s the reason why anyone would want to use it. Gold can be seen as the way to keep all those currencies honest.

People mistakenly believe that gold is all about inflation. That’s not quite it, but high inflation is usually very helpful for gold. What gold really likes is to see is very low real (meaning after inflation) interest rates. Gold is almost like a highly-leveraged short on short-term TIPs.

Here’s a good rule of thumb. Gold goes up anytime real rates on short-term U.S. debt are below 2% (or are perceived to stay below 2%). It will fall if real rates rise above 2%. When rates are at 2%, then gold holds steady. That’s not a perfect relationship but I want to put it in an easy why for new investors to grap. This also helps explain why we’re in the odd situation today of seeing gold rise even though inflation is low. It’s not the inflation, it’s the low real rates that gold likes.

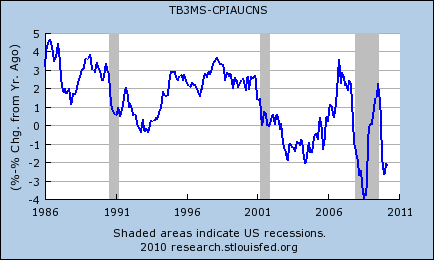

This chart shows the three-month Treasury bill rate minus the one-year inflation rate (low is good for gold, high is bad):

In February, gold took a big hit when the Fed announced it was lifting the discount rate. This isn’t the all-important Fed funds rates, but you can see how nervous the market was over the threat of higher real rates.

This rule of thumb also tells us that gold can rise very quickly and it can fall very quickly. One Ben and his pals at the Fed raise rates, gold is in for a world of hurt. The history of the price of gold is long boring periods with sharp dramatic spikes. The up part of the spike is fun. The downside, less fun.

What’s tricky about gold is that it’s also impacted by geo-politics. Gold peaked in 1980 shortly after the Soviets invaded Afghanistan. It reached a low point not long before we did the same.

The pricing of any commodity can be tricky because commodities are subject to substitution. Let’s say that gold, despite its high price, is the cheapest way to make a part for a certain kind of semiconductor. That will drive demand for gold. However, let’s say that once gold crosses a certain level, it’s no longer the cheapest way to make the part. Maybe unobtanium is a better way to go. That will, in turn, undermine gold’s value. It’s price impacts its price.

This is a major difference between investing in equities and investing in commodities. Stocks are companies, filled with people aiming to make a profit. Gold is just a rock. It just sits there. In 10,000 years, it will still be a rock.

My view is that the Federal Reserve will raise interest rates earlier than expected. I don’t know exactly when that will be but it will put gold on a dangerous path. For now, my advice is to stay away from gold, either long or short. -

Best. Stock. Name. Ever.

Posted by Eddy Elfenbein on May 13th, 2010 at 12:14 pmI give you — Crazy Woman Creek Bancorp (CRZY)

-

Progressive +40,000%

Posted by Eddy Elfenbein on May 13th, 2010 at 11:34 amHere’s another entry in our series, “boring but highly profitable stocks.” Today’s entry is Progressive (PGR) the auto insurance company.

Insurance stock? You’re thinking snores-ville right? Well, check this out. Thirty years ago you could have picked up a share for a split-adjusted price of five cents.

The gold line is the S&P 500. It’s barely visible in comparison. -

Wendy’s Posts Loss

Posted by Eddy Elfenbein on May 13th, 2010 at 10:09 am

Now we know a little more about the turnaround at Wendy’s/Arby’s Group (WEN). The company just posted a loss for its first quarter (before charges). However, the company’s new focusing wasn’t fully implemented for the entire quarter.Revenue at Arby’s restaurants fell 12 percent in the quarter.

The lackluster Arby’s showing weighed on overall results, as the owner of Wendy’s and Arby’s restaurants said Thursday that it lost $3.4 million, or a penny per share, for the three months ended April 4. That compares with a loss of $10.9 million, or 2 cents per share, last year.

Removing 3 cents per share in charges, profit was 2 cents per share.

Total revenue fell 3 percent to $837.4 million from $864 million.

Wall Street expected the Atlanta company to earn 1 cent per share on revenue of $835.2 million. The estimates of analysts surveyed by Thomson Reuters generally exclude one-time items.The stock is down today about 3% although I don’t think the earnings report says much about WEN’s future. If this turnaround does work, it will take more time. On the other hand, we can see that this situation isn’t getting worse. I still view WEN as a highly speculative value stock.

- Tweets by @EddyElfenbein

-

-

Archives

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His