-

Saddest Investing Fact of the Day

Posted by Eddy Elfenbein on May 11th, 2010 at 4:17 pmA household with income under $13,000 spends, on average, $645 a year on lottery tickets, or about 9 percent of all income.

-

Intel’s Guidance

Posted by Eddy Elfenbein on May 11th, 2010 at 2:39 pmIntel CEO Paul Otellini said Tuesday that the company’s revenue and net income per share should see a percentage increase in the low double digits over the next few years because of rising demand for its chips in personal computers and other gadgets.

On both measures, Intel Corp.’s numbers have declined over the past two years as business spending on PCs and computer servers collapsed amid the recession. However, strong buying by bargain-hunting consumers has helped lift Intel’s fortunes in recent quarters, and sales of server chips — some of Intel’s most profitable products — have improved.

Otellini told investors and financial analysts at a conference at Intel’s Silicon Valley headquarters that the forecast proves that PCs are “still a growth industry.”

It’s difficult to say, however, how the new guidance compares with analysts’ expectations.

Otellini’s forecast was based on a “compound annual growth rate,” a measure that includes multiple years of results. He did not specify the years.

Analysts polled by Thomson Reuters expected Intel’s recovery from the downturn to show a 23 percent increase in revenue and a more than doubling of earnings per share in 2010 over the year before. For 2011, the analysts expected less-dramatic growth of a 5 percent increase in both revenue and earnings per share, compared with their 2010 forecasts. -

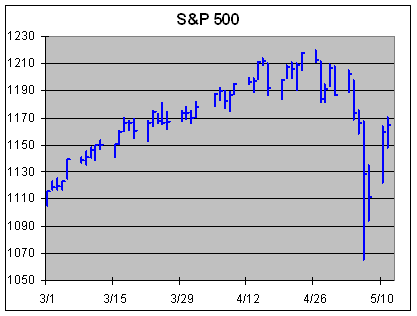

Guess What Index is 100 Points Above Its Thursday Low

Posted by Eddy Elfenbein on May 11th, 2010 at 2:13 pmI’ll give you a hint: The S&P 500.

-

“Even if they fail miserably at a job, they still think they’re great at it.”

Posted by Eddy Elfenbein on May 11th, 2010 at 1:31 pm

New academic report proves that Gen Y is just awful.Gen Y workers get a bad rap in the workplace, with many a geezer complaining that their work ethic is less developed than their sense of entitlement. But is that really fair?

Yes, according to new research that’s yielded actual data to back up that notion.

In a series of studies using surveys that measure psychological entitlement and narcissism, University of New Hampshire management professor Paul Harvey found that Gen Y respondents scored 25 percent higher than respondents ages 40 to 60 and a whopping 50 percent higher than those over 61.

In addition, Gen Y’s were twice as likely to rank in the top 20 percent in their level of entitlement — the “highly entitled range” — as someone between 40 and 60, and four times more likely than a golden-ager.

Harvey’s conclusion? As a group, he says, Gen Yers are characterized by a “very inflated sense of self” that leads to “unrealistic expectations” and, ultimately, “chronic disappointment.”

And if you think the Gen Yers in your workplace are oversensitive as well as entitled, Harvey’s findings back that up, too. Today’s 20-somethings have an “automatic, knee-jerk reaction to criticism,” he says, and tend to dismiss it.

“Even if they fail miserably at a job, they still think they’re great at it.” -

One-Time Audit the Fed Passes the Senate 96-0

Posted by Eddy Elfenbein on May 11th, 2010 at 1:11 pmSenator David Vitter’s amendment to audit the Federal Reserve failed by a vote of 37 to 62. However, Senator Bernie Sanders worked out a compromise to conduct a one-time audit of the Fed. That vote passed 96 to 0.

“At a time when the Federal Reserve has provided the largest taxpayer bailout in the history of the world, the largest financial institutions in this country, trillion-dollar institutions,” Mr. Sanders said in a floor speech, “the Sanders amendment makes it clear that the Fed can no longer operate in the kind of secrecy that it has operated in forever.”

He added, “For the first time the American people will know exactly who received over $2 trillion in zero or virtually zero-interest loans from the Fed, and they will know the exact terms of those financial arrangements.”

Mr. Sanders, a self-described socialist, has long demanded greater transparency at the central bank, and his original plan could have subjected the Fed to ongoing audits of some routine operations. But he agreed to scale back the proposal in the face of opposition by the White House, the Fed, the Treasury and some Senate colleagues.

The critics said that more aggressive audits would impede on the Fed’s independence and potentially interfere with its ability to set monetary policy. Mr. Sanders and other proponents of fuller audits of the Fed rejected those assertions and said they were providing sufficient safeguards to protect the central bank’s integrity.This issue seems to confuse many people. In a traditional sense, the Federal Reserve is already audited. Current law bars an audit of the Fed’s open market operations. The belief is that such an audit would undermine the Fed’s independence.

The idea is that auditing the Fed’s open market operations would really serve as a policy veto. I’ll give you an example. Let’s say you conduct an audit of the Department of Bureaucracy. The auditors room through the books and find out that the DOB spent $1.2 million on a ham sandwich. You’ll notice that this is in no way a policy decision. The auditors have made a judgment that this was too much too spend for a ham sandwich. But the Federal Reserve is a different animal. Perhaps it was the Fed’s intent to buy a ham sandwich for $1.2 million. Sure, it may sound crazy but this is what central banks do. That was the policy decision. What the Fed does is buy and sell stuff so an audit (so the argument goes) opens up auditors to not merely audit, but question the Fed’s policy decisions. Those policy decisions (again, so the argument goes) are already held accountable when the Fed Chair appears before Congress.

Personally, I think the Fed’s independence is given a level of sacredness it doesn’t deserve. Quite simply: If the people want 20% inflation, they should get it. The Fed is a creation of Congress and Congress should be able to do whatever it wants with the Fed. The central bank is not independent. I fail to see why it’s so important that the Fed “remain independent.” I would agree that the Fed needs latitude to act, but not independence. -

Volatility Does Not Equal Risk

Posted by Eddy Elfenbein on May 11th, 2010 at 12:36 pmI don’t easily go about criticizing Finance Blogger King Felix Salmon (especially after he said such nice things about me), but I have to speak up when he equates volatility with risk. Felix says that stocks aren’t a good buy and adds that “when an asset class gets more volatile, it gets riskier.”

Hmmm. Let’s take a step back. Risk is a very peculiar concept in finance. The problem is that we use this one word “risk” to describe many different things. What does risk mean? Well, you can take your pick. There’s the risk of what you don’t know. There’s systemic risk. There’s the risk that you won’t do as well as everybody else. There’s the risk that you’ll lose everything. The list of risks goes on and on.

Gold is a good case study on which to contemplate the meaning of risk. Gold is popular with goldbugs because it’s the least risky investment possible. In this sense, we’re defining risk as an investment losing its inherent value. In other words, gold can’t go bankrupt. Governments? Sure, they go belly up all the time, but even in our Mad Max future, gold will still be around.

But in another sense of the word risk, gold is highly risky. Gold tends to be very volatile. It bounces up a lot each day. On the other hand, gold tends to have a very low, and even negative, beta. So which is it? Is gold risky or not? It really depends on the kind of risk you’re talking about.

My point is that there’s no evidence that greater equity volatility leads to poorer performance. The risk of a market plunge is the kind of risk that matters. Except at very low levels, the historical evidence is that volatility doesn’t much affect future returns. Only when the VIX gets down below 13 does that market show some outperformance.

I know it seems counter-intuitive but volatility does not equal danger. -

Gilead Announces $5 Billion Buyback

Posted by Eddy Elfenbein on May 11th, 2010 at 10:48 amGilead Sciences Inc. (GILD) announced a 3-year, $5 billion stock-buyback effort, with the board and management considering the move “an appropriate and strategic use of the company’s cash.”

A host of companies have been boosting or initiating repurchase plans in recent months as the need to hoard cash recedes. The drug maker, known more for its HIV treatments, announced Tuesday it has completed a $1 billion buyback effort authorized in January, buying 24.1 million shares for an average $41.43.

The stock was up 1.6% premarket at $39.00 and was down 11% this year through Monday. Gilead’s market value is about $35 billion.

The drug maker plans to fund the repurchase program with future profit as Gilead said on Tuesday that the company has made significant progress with its HIV pipeline programs to develop a new treatment regimen, which it expects to file for regulatory approval this year.

Gilead reported last month its first-quarter profit jumped 45% on strong sales of its HIV drugs as well as higher royalties from flu-treatment Tamiflu because of worldwide initiatives to plan for a possible influenza pandemic.Just give us the money! The buyback works out to about $5.50 per share and Gilead doesn’t pay a dividend. At least, the stock is up today.

-

Dean Foods Plunges Below $10

Posted by Eddy Elfenbein on May 11th, 2010 at 10:26 amA few weeks ago, I highlighted Dean Foods (DF) as a good value stock. The market, however, seems to have other ideas. Yesterday, the company missed its earnings estimate by five cents a share (23 cents versus 28 cents; in February Dean gave a range of 25 to 30 cents). The stock responded by dropping 28% and it’s down again today. DF is now below $10 a share. It’s never a good idea to tell Wall Street to expect one thing and deliver another.

Wall Street had been expecting Q2 earnings of 41 cents per share. Instead, Dean said it will range between 23 and 28 cents per share. The problem is that there’s a price war going on in the milk business and that’s hurting profit margins. Dean’s Q1 actually beat Wall Street’s revenue target. The issue is turning those sales into profits.

The WSJ reports:Dean Foods Co. Chairman and Chief Executive Gregg Engles said gains by private-label producers are accelerating despite an improving economy, noting that in some regions, a half-gallon of his company’s milk costs more than a gallon of an unbranded product. Major retailers routinely use discounted staples such as milk, bread, eggs and meat to drive foot traffic, and private-label food products gained market share as consumers traded down during the recession.

Cheaper private-label products have been gaining food-industry market share for years, but Mr. Engles is acknowledging that the weak economy may have forced a long-term change in consumption that holds ramifications for margins and investment. Milk prices have firmed in recent months after a volatile period, but Mr. Engles said efforts to push through increases at the retail level have failed to stick.

-

Risk and Return: Not So Easy

Posted by Eddy Elfenbein on May 11th, 2010 at 9:50 amEric Falkenstein is the author of Finding Alpha which argues that, in the real world, risk and return are not related. In fact, if there is a relationship, it’s probably negative. The more risk you take on, the worse you’ll do.

As Eric explains, a good example of this is in corporate bonds. Both the riskiest bonds—high-yield junk bonds—and the least risky—rock-solid AAA bonds—don’t do as well as bonds rated as investment grade but just below top-shelf.

Why is this? Is it that both ends of the risk spectrum unusually crowded? Eric writes:It may be that individual investors expect high returns when investing in high risk assets, only that this is a mass delusion, the triumph of hope over experience. If so, that isn’t the ‘expected return’ one talks about in academic finance, that is, a statistically rational expected return. It is important to think of a return premium as due to two things: randomness and alpha. Randomness or luck we all understand. Alpha, however, is a little trickier. It isn’t something you can buy, because due to competition, no one sells it for less than cost, meaning, the insiders who structure and sell any alpha idea will take out all the extra return, leaving nothing at best, a mean-mode trade* at worst. To get alpha, you don’t buy something passively, you have to actively negotiate, time, or structure an investment, and while people can help you, no one will singularly present you with an extra-normal return. Further, most alpha attempts are like karaoke ballads, well intentioned but ultimately awful, meaning, after fees most alpha is negative (how else do so many alpha-less brokers afford their nice cars!?).

It is difficult to see how the little risk is priced, the big one not, if risk is to have any consistent meaning. If the corporate spread is a function of risk at one end, why is it not at the other, more intuitive end? This is but another reason I think there is no general risk premium, as explained in my series of Camtasia videos on my book here. -

Jon Stewart on the Crash

Posted by Eddy Elfenbein on May 11th, 2010 at 9:09 amThe Daily Show With Jon Stewart Mon – Thurs 11p / 10c A Nightmare on Wall Street Daily Show Full Episodes Political Humor Tea Party

- Tweets by @EddyElfenbein

-

-

Archives

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His