-

The Economy Grew by 3.2% for the First Quarter

Posted by Eddy Elfenbein on April 30th, 2010 at 9:34 amThe government reported that the economy grew by 3.2% for the first quarter. Normally, that’s not so bad but for coming out of a deep recession, it’s very unimpressive.

Federal government spending, which includes remaining stimulus money, grew at an annualized rate of 1.4 percent in the first quarter of 2010. But this was more than offset by continued spending cuts from state and local governments, whose spending decreased 3.8 percent. It was the third quarter in a row in which state and local spending fell.

“Government spending contracted, for all the ballyhoo about stimulus,” said John Ryding, chief economist at RDQ Economics. “This recovery is going to have to stand on the backs of private-sector demand, not on government demand, given all the current fiscal challenges.” Even though any pickup in business is welcome, modest improvement may not be enough to alleviate the pain caused by the so-called Great Recession, many economists say.

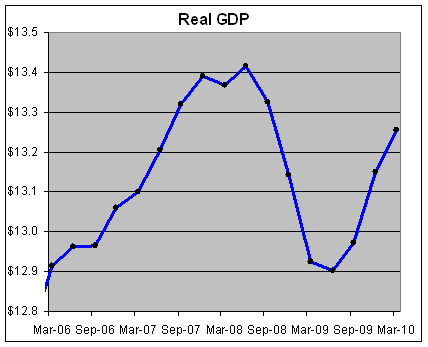

The nation’s gross domestic product — a broad measure of goods and services produced in the country — is far below its potential, according to economists’ projections of where the economy would have been if it followed its long-term trend. Output would need to grow at least 5 percent annually for several years to get back on track — and perhaps more importantly, to lead to enough job creation to employ the 15 million Americans already out of work and the 100,000 new workers joining the labor force each month.Earlier this week, I took a stab at giving a letter name to this recovery. My guess for Q1 was pretty close but a tad too high (I had 3.5% instead of 3.2%). Here’s the up-to-date chart:

Thanks to several emailers, I’m going to call it an N-Shaped recovery.

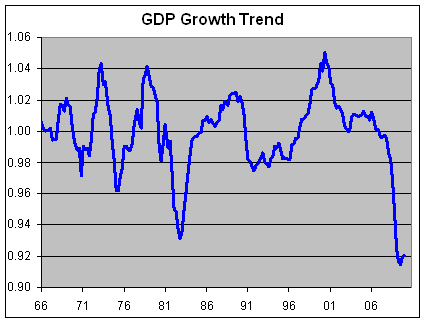

Here’s a more sobering way to look at GDP. This chart shows real GDP divided by a trendline growing at 3.08% which is about the long-term rate of growth.

In other words, this shows you how well GDP is doing compared with its historic growth rate. We’ve fallen off a cliff and are in the process of splatting.

In previous recessions, the economy has snapped back sharply to its historic trendline (1.0 on the chart). By growing at 3.2% last quarter, the economy is barely making headway.

At 0.92, we’re 8% below the trendline. This is what the NYT means by growing at 5% for a few years to get back on track. If the economy grew by 5% a year — 2% higher than the long-term trend — for four years, then we’d finally get back to something resembling normal. -

Behold!

Posted by Eddy Elfenbein on April 29th, 2010 at 3:09 pmWhen Alexander saw the breadth of his domain he wept for there were no more worlds to conquer.

In other news: -

Do Superstitious Beliefs Affect Investment Decisions?

Posted by Eddy Elfenbein on April 29th, 2010 at 11:21 amDark Omens in the Sky: Do Superstitious Beliefs Affect Investment Decisions?

By Gabriele M. Lepori

Psychological research documents that individuals are more likely to resort to superstitious practices when operating in environments dominated by uncertainty, high stakes, and perceived lack of control over the outcomes. Based on these findings, we suggest that the stock market represents an ideal breeding ground for superstition and then test whether superstition-induced behavior affects investment decisions. Our empirical analysis focuses on some beliefs associated with eclipses, phenomena that are typically interpreted as bad omens by the superstitious both in Asian and Western societies, and we employ a dataset containing 362 such events over the period 1928-2008. Using four broad indices of the U.S. stock market, we uncover strong evidence in support of our superstition hypothesis in four distinct ways. First, the occurrence of negative superstitious events (i.e. eclipses) is associated with below-average stock returns, which is consistent with a diminished buying pressure coming from the superstitious. Second, the size of the superstition effect is estimated to increase in times of high market uncertainty and when eclipses draw wide media coverage and public attention. Third, the negative performance of the market during the superstitious event is followed by a reversal effect of similar magnitude (10 basis points per day) on the subsequent trading days. Fourth, eclipses are accompanied by a trading volume decline. When we extend our analysis to a sample of Asian countries, we find analogous results. The patterns we document are inconsistent with the Efficient Market Theory, as eclipses are perfectly predictable events.If anyone needs me, I’ll be reading entrails.

-

Obama Nominates Three to the Board of the Federal Reserve

Posted by Eddy Elfenbein on April 29th, 2010 at 10:56 amPresident Obama is getting the chance to place his stamp on the Federal Reserve. There were three vacancies and he just sent three nominees to the Senate for confirmation:

The White House tapped Janet Yellen, president of the San Francisco Federal Reserve Bank, to be the board’s vice chairman, and Massachusetts Institute of Technology economist Peter Diamond and Maryland state banking regulator Sarah Bloom Raskin to sit on the seven-member board. The Senate is likely to confirm them.

Just to clear up any confusion, the Federal Reserve is run by its seven-member Board of Governors. That’s what President Obama is filling out.

The interest-rate policy committee is the Federal Open Market Committee (FOMC) which has 12 members—the seven governors plus a rotating selection of five of the twelve regional bank presidents. The President of the New York Fed is always there.

Janet Yellen is currently the President of the San Francisco Fed so she was a member of the FOMC last year. San Francisco rotated off in 2010. -

Becton Dickinson Beats by Four Cents

Posted by Eddy Elfenbein on April 29th, 2010 at 10:48 amI’m happy to see that our stocks are rebounding nicely this morning. Two Buy List earnings reports are due today. Fiserv (FISV) will come after the close. Before the bell, Becton Dickinson (BDX) said it earned $1.27 per share which was four cents better than estimates. The company reaffirmed full-year earnings-per-share of $5.05 to $5.15 which excludes four cents due to Obamacare. Note that the March quarter is BDX’s fiscal second quarter so their fiscal year is already half over.

-

Eddy’s Rule on European Monetary Integration

Posted by Eddy Elfenbein on April 29th, 2010 at 10:30 amNew rule: Everyone with nice beaches, please leave the eurozone.

(This rule may come in handy if Florida and California are kicked out of the dollar.) -

This Won’t End Well

Posted by Eddy Elfenbein on April 28th, 2010 at 6:21 pm

This is a HUGE mistake:Hewlett-Packard Agrees to Buy Palm

Hewlett-Packard has agreed to acquire Palm for $1.4 billion in cash, uniting two companies that have failed to make much recent headway in the smartphone business.

H.P. announced its all-cash purchase of Palm just after the financial markets closed on Tuesday, saying it would pay $5.70 a share. Shares of Palm were down during regular trading on Wednesday, closing at $4.63, and rose in early after-hours trading by 27 percent to $5.90. The $1.4 billion price includes the Series B and Series C shares, most of which are owned by Elevation Partners.

During the last year, shares of Palm have traded as high as $18 a share and as low as $3.65.

Palm listed $400 million in debt at the end of its third quarter, which H.P. would retire using some of the $592 million in cash that Palm has on hand.Let’s look at some of Palm‘s (PALM) recent quarterly results:

Q1 2008: +0.09

Q2 2008: -0.07

Q3 2008: -0.16

Q4 2008: -0.22

Q1 2009: -0.12

Q2 2009: -0.73

Q3 2009: -0.86

Q4 2009: -0.40

Q1 2010: -0.10

Q2 2010: -0.37

Q3 2010: -0.61

That’s not a good tend.

For those of you keeping score at home, Palm was spunoff from 3Com on March 2, 2000.Living up to feverishly high expectations, 3Com’s (COMS) Palm (PALM) division exploded onto the market today, tripling at the open and moving to a high of $165 — up 334% from its offering price of $38 a share. It slid back to around $95.06 by the closing bell, but still stood 150% higher.

The deal — which also included the private placement of shares to AOL (AOL), Motorola (MOT) and Nokia (NOK) — was co-managed by Goldman Sachs and Morgan Stanley Dean Witter. Palm offered 23 million shares, or a 4% stake in the company.At one point, Palm was worth more than 3Com, the company that owned almost all of its shares. Chalk one up for EMH!

By the way, that $165 bolded above is really $1,650 in today’s shares since the company had a 1-for-20 reverse split followed by a 2-for-1 split. HP is agreeing to buy Palm for $5.70.

-

AFLAC Holds Greek and Portuguese Bonds

Posted by Eddy Elfenbein on April 28th, 2010 at 3:05 pmOn AFLAC’s earnings call, the company revealed that it holds $1.75 billion in Greek and Portuguese bonds.

Aflac Inc., the world’s largest seller of supplemental health insurance, said it holds almost $2 billion of bonds tied to banks in Greece and Portugal, nations that have been cut by ratings firm on mounting debt.

Aflac has about $1 billion in Greek bank bonds and $750 million issued by Portuguese lenders, Chief Investment Officer Jerry Jeffery said in a conference call today. The insurer also holds about $285 million in Greek sovereign bonds, Jeffery said. Greece is waiting on word of a 45 billion-euro ($59 billion) rescue package from the European Union and the International Monetary Fund after the nation’s credit rating was cut to junk by Standard & Poor’s yesterday. The ratings firm lowered its rating on Greece by three levels to BB+ from BBB+ and warned that investors could recover as little as 30 percent of their initial outlay if it restructures its debt.

Aflac is “looking very carefully” at limits on sovereign debt, Jeffery said. “I still don’t think it’s predictable what’s going to happen with Greece, but there is enormous pressure being applied by the EU and IMF as we speak. It will be very instructive as to how we proceed.” -

Today’s FOMC Statement

Posted by Eddy Elfenbein on April 28th, 2010 at 2:41 pmHere’s today’s policy statement:

Information received since the Federal Open Market Committee met in March suggests that economic activity has continued to strengthen and that the labor market is beginning to improve. Growth in household spending has picked up recently but remains constrained by high unemployment, modest income growth, lower housing wealth, and tight credit. Business spending on equipment and software has risen significantly; however, investment in nonresidential structures is declining and employers remain reluctant to add to payrolls. Housing starts have edged up but remain at a depressed level. While bank lending continues to contract, financial market conditions remain supportive of economic growth. Although the pace of economic recovery is likely to be moderate for a time, the Committee anticipates a gradual return to higher levels of resource utilization in a context of price stability.

With substantial resource slack continuing to restrain cost pressures and longer-term inflation expectations stable, inflation is likely to be subdued for some time.

The Committee will maintain the target range for the federal funds rate at 0 to 1/4 percent and continues to anticipate that economic conditions, including low rates of resource utilization, subdued inflation trends, and stable inflation expectations, are likely to warrant exceptionally low levels of the federal funds rate for an extended period. The Committee will continue to monitor the economic outlook and financial developments and will employ its policy tools as necessary to promote economic recovery and price stability.

In light of improved functioning of financial markets, the Federal Reserve has closed all but one of the special liquidity facilities that it created to support markets during the crisis. The only remaining such program, the Term Asset-Backed Securities Loan Facility, is scheduled to close on June 30 for loans backed by new-issue commercial mortgage-backed securities; it closed on March 31 for loans backed by all other types of collateral.

Voting for the FOMC monetary policy action were: Ben S. Bernanke, Chairman; William C. Dudley, Vice Chairman; James Bullard; Elizabeth A. Duke; Donald L. Kohn; Sandra Pianalto; Eric S. Rosengren; Daniel K. Tarullo; and Kevin M. Warsh. Voting against the policy action was Thomas M. Hoenig, who believed that continuing to express the expectation of exceptionally low levels of the federal funds rate for an extended period was no longer warranted because it could lead to a build-up of future imbalances and increase risks to longer run macroeconomic and financial stability, while limiting the Committee’s flexibility to begin raising rates modestly. -

150 Years of Corporate Bond Defaults

Posted by Eddy Elfenbein on April 28th, 2010 at 2:28 pmHere’s a bit of a geeky post. This recent academic paper looks at default rates for corporate bonds over the last 150 years. There are plenty of studies of corporate bond defaults, but none that I know of that go back this far.

The results of the study are pretty interesting. The researchers found that there have been several episodes of high levels of defaults. These episodes are tightly bunched together and they’re separated by many years of very low default rates. The Great Depression wasn’t nearly as bad as some of the 19th century panics. In fact, default periods are only weakly associated with bad economies.

The researches also found that bond spreads are about twice the default rate. Plus, spreads don’t have much forecasting ability although stock market returns and stock volatilities do. They found that over the very long haul, corporate bonds fault about 1.5% of the time.

- Tweets by @EddyElfenbein

-

-

Archives

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His