-

President Obama’s Speech

Posted by Eddy Elfenbein on April 22nd, 2010 at 12:24 pmHere’s the text of the speech President Obama gave today at Cooper Union:

It’s good to be back in the Great Hall at Cooper Union, where generations of leaders and citizens have come to defend their ideas and contest their differences. It’s also good being back in Lower Manhattan, a few blocks from Wall Street, the heart of our nation’s financial sector.

Since I last spoke here two years ago, our country has been through a terrible trial. More than 8 million people have lost their jobs. Countless small businesses have had to shut their doors. Trillions of dollars in savings has been lost, forcing seniors to put off retirement, young people to postpone college, and entrepreneurs to give up on the dream of starting a company. And as a nation we were forced to take unprecedented steps to rescue the financial system and the broader economy.

As a result of the decisions we made – some which were unpopular – we are seeing hopeful signs. Little more than one year ago, we were losing an average of 750,000 jobs each month. Today, America is adding jobs again. One year ago, the economy was shrinking rapidly. Today, the economy is growing. In fact, we’ve seen the fastest turnaround in growth in nearly three decades.

But we have more work to do. Until this progress is felt not just on Wall Street but Main Street we cannot be satisfied. Until the millions of our neighbors who are looking for work can find jobs, and wages are growing at a meaningful pace, we may be able to claim a recovery – but we will not have recovered. And even as we seek to revive this economy, it is incumbent on us to rebuild it stronger than before. That means addressing some of the underlying problems that led to this turmoil and devastation in the first place. -

Don’t Pity Goldman’s Victims

Posted by Eddy Elfenbein on April 22nd, 2010 at 11:54 amJohn Carney has a great piece in the Daily Beast pointing out that the alleged victims of Goldman Sachs were hardly victims:

The crucial question in the SEC’s case against Goldman is whether Rhineland should have been told that Paulson was ultimately the short-seller in this deal or that he had played an important role in selecting the securities that went into Abacus. While it’s not clear that in 2007 anyone would have been worried about a little-known hedge fund being short a deal if they weren’t already worried about Goldman being short, Rhineland certainly should have asked how the portfolio was constructed.

So why didn’t Rhineland—or the managers who controlled it from Dusseldorf—make these inquiries? Most likely, because IKB was playing the game even more aggressively.Fortunately, David Letterman has Goldman’s Top 10 excuses:

-

J&J’s Amazing Dividend Streak Continues

Posted by Eddy Elfenbein on April 22nd, 2010 at 10:39 amJohnson & Johnson (JNJ) just announced its 48th straight annual dividend increase. The company is raising its quarterly dividend by 10.2%, increasing it from 49 cents per share to 54 cents per share. I’ll give Alan Brochstein credit for getting it right on the nose. The stock now yields 3.3%.

As I pointed out earlier, a person who bought JNJ 25 years ago is now getting close 100% a year just in dividends.

-

Baxter Drops on Lower Guidance

Posted by Eddy Elfenbein on April 22nd, 2010 at 10:16 amWe had two more earnings reports from our Buy List this morning. I’ll start with the good. Reynolds American (RAI), the tobacco company, reported Q1 earnings of $1.11 per share which was four cents better than expectations. Revenue grew by 3.4% which was also better than the Street’s expectations. More importantly, Reynolds reaffirmed its full-year forecast of $4.80 to $5 a share, so we’re talking about a forward P/E of around 11. The stock also pays a very rich dividend of 90 cents a quarter which translates to a yield of 6.4%. Reynolds continues to be a very good buy.

The major blow to the Buy List comes today from Baxter International (BAX). The earnings report wasn’t so bad, 93 cents a share which was inline. The problem was that they lowered full-year expectations from the previous range $4.20 to $4.28 per share to $3.92 and $4 per share. For Q2, BAX sees earnings ranging between 90 and 93 cents per share. The Street was expecting $1.06 per share. Ouch! This is a very disappointing report.

Finally, Netflix (NFLX) continues to embarrass me and anyone else with common sense. The stock is up 14% this morning. The stock reminds me of a mighty ocean-going vessel steaming its way through the chilly waters of the North Atlantic. Nothing can stop it now!

-

Tea Party Anyone?

Posted by Eddy Elfenbein on April 22nd, 2010 at 8:58 amFrom the New York Times‘ (NYT) earnings report:

Income Taxes

The Company’s effective income tax rate was 65.6 percent in the first quarter. The high tax rate for the quarter was driven by a $10.9 million one-time tax charge for the reduction in future tax benefits for retiree health benefits resulting from the recently issued federal health care legislation. Excluding the charge, the Company’s effective income tax rate was 39.3 percent in the first quarter.

In the first quarter of 2009, the Company recognized a pre-tax loss of $75.4 million but only an income tax benefit of $1.2 million. The tax provision was unfavorably affected by significant losses at the New England Media Group, for which only a minimum state tax benefit was recognized due to a Massachusetts law change, and various nondeductible losses. These items were partially offset by a $12 million adjustment to reduce the Company’s reserve for uncertain tax positions. -

Starbucks: The Turnaround Continues

Posted by Eddy Elfenbein on April 22nd, 2010 at 7:49 am

One of the best investment opportunities is the Turnaround Stock. The major problem with the Turnaround Stock is that the real deal is very, very hard to find.

In business, success breeds complacency. You see it all the time. Lots of good companies find themselves running into trouble, and soon they start losing market share and watching their profit margins fall. Once trouble comes, it’s not hard for a company to announce a restructuring effort, but it’s very hard to pull one off. What’s worse is that shareholders are notoriously impatient and that often hinders a turnaround effort.

I like to follow Starbucks (SBUX) because it’s a very good example of a company facing their problems and doing something bold about them. The company greatly over-expanded and soon, their same-store sales started to fall. Starbucks fired the CEO, rolled up its sleeves and dramatically cut back on the numbers of stores.

Earnings-per-share peaked in 2007 at 87 cents, then fell to 71 cents in 2008 and rebounded to 80 cents in 2009. The stock plunged from $40 in 2006 to just $7 by November of 2008. That’s the kind of thing shareholders tend to notice.

Well, Starbucks has come a long way. The company just reported earnings and business continues to improve. The company earned 29 cents a share for their fiscal Q2 compared with 16 cents a year ago. The details of the report are pretty good. Net revenues rose 9%. Compared stores sales increased 7%. Most impressively, SBUX’s operating margin rose from 10.4% a year ago to 17.8% this year. Whenever you find expanding margins, take notice!

Starbucks also said they’re increasing their full-year guidance (which is already half over) to $1.19 to $1.22 a share. This is the second time they’ve raised full-year guidance. In November, Starbucks said to expect 92 to 96 cents a share. Then in January, they said to expect $1.02 to $1.05 a share. I like this trend.

Let’s think about this. In November of 2008, SBUX was going for less than nine times what the company earned between September 2008 and September 2009, and less than six times what they’ll probably earn in the 12 months after that. The company also recently paid out its first-ever dividend.

The shares are now up more than 250% from their low 18 months ago. If anyone needs me, I’ll be kicking myself for missing this one. -

Large-Caps Do Well Before Options Expiration

Posted by Eddy Elfenbein on April 21st, 2010 at 11:18 pmOver 1983 to 2008, we find that large-cap stocks with actively traded options tend to have substantially higher average weekly returns during option-expiration weeks (ending on a month’s third-Friday), with consistent subperiod results. This empirical regularity is also evident in large-cap-dominated stock portfolios. Further, over the 1996 to 2008 period with available Option Metrics data, we find that the average weekly stock returns for option-expiration weeks tend to be appreciably larger for option-expiration weeks that also experience a relatively high option trading volume, relative to the underlying stock trading volume. In contrast, the average weekly returns for the option-expiration week are not much different than other weeks for smaller-cap stock portfolios, which contain stocks with relatively less option trading activity. Further, for our sample of large-cap stocks, the average weekly stock returns for the third-Friday of a calendar month are not different than other weeks for a pre-option-market sample over 1948 to 1972. We provide additional evidence that, along with the option market evidence in Lakonishok, Lee, Pearson, and Poteshman (2007), suggests that the sizable written call activity from non-market makers may contribute towards understanding our empirical findings.

-

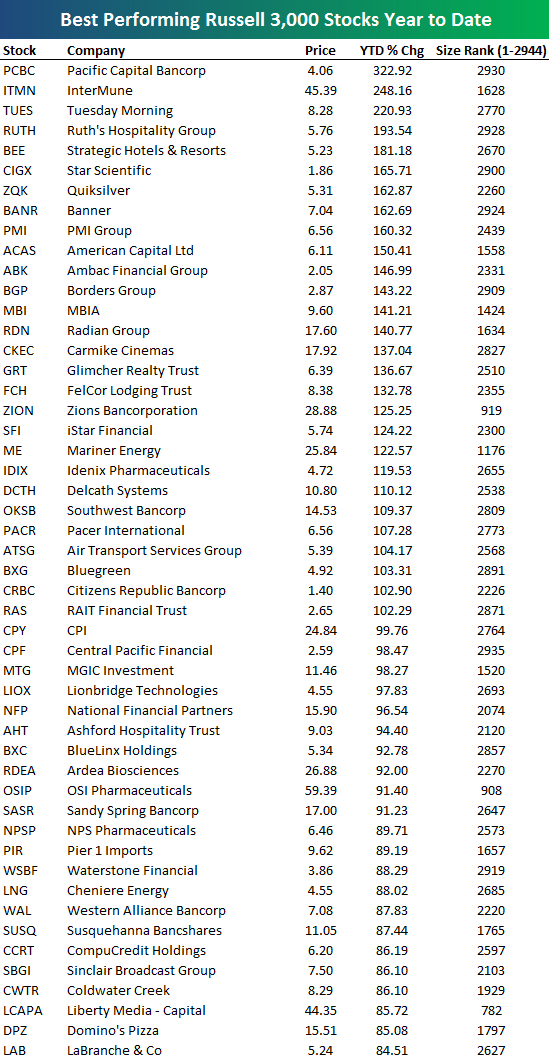

The Top Performing Russell 3000 Stocks YTD

Posted by Eddy Elfenbein on April 21st, 2010 at 5:39 pmIt’s still earlier, but Bespoke Investment Group lists the best-performing stocks in the Russell 3000 (^RUA) for 2010. Here’s a look:

-

Netflix Earns 59 Cents a Share

Posted by Eddy Elfenbein on April 21st, 2010 at 4:41 pmYesterday I said that Netflix (NFLX) was an awful stock to buy, and it looks like the market may finally be agreeing with me. The company reported outstanding quarterly results, but the stock is down in the after-hours market. I won’t say “I told you so” even though I, in fact, told you so.

The problem isn’t NFLX’s business which is doing extremely well. It’s that the valuation is so high, there’s almost nothing Netflix can do to justify the sky-high share price.

Let’s run through some of the numbers. After the bell, Netflix reported Q1 earnings of 59 cents a share, five cents more than Wall Street was expecting. In January, the company said to expect Q1 EPS between 47 and 58 cents, so they even beat their top-end. A year ago, they earned 37 cents a share. Revenues rose 25.3% to $493.7 million. What else can I say? Businesswise, this was an outstanding quarter.

For Q2, Netflix said to expect EPS between 62 and 73 cents. For all of 2010, they raised their EPS range from $2.28 to $2.50, to $2.41 to $2.63. That’s impressive but I’d hardly call it unexpected. This stock is still way, way WAY overpriced.

Netflix continues to be a Strong Sell.

Update: OK, now NFLX is up slightly after-hours.

-

The Fed Paid $47.4 Billion to the U.S. Treasury

Posted by Eddy Elfenbein on April 21st, 2010 at 3:23 pmOne of the more unhinged conspiracy theories is that the Federal Reserve is a private bank. Even noted monetary economists Spencer and Heidi have commented on this (warnings: the video will slaughter your brain cells — you’ve been warned).

Unfortunately, it’s not true. Everything the Fed makes over 6% goes right to Uncle Sam and last year it was a nice haul.Taxpayers got a record $47.4 billion last year from the Federal Reserve, new documents released Wednesday showed.

The payment to the Treasury Department is slightly higher than the $46.1 billion first estimated in January. The new figure is based on more complete information contained in audited financial statements for the Fed’s 12 regional banks and related units.

The amount handed over to Treasury last year is $15.7 billion more_ or a 50 percent increase — from 2008, the Fed says.

The bigger windfall to taxpayers reflects gains from the Fed’s efforts to fight the financial crisis and revive the economy. Critics have worried that the Fed’s actions could put taxpayers at risk by reducing the amount turned over to Treasury coffers.

Interest earned from the Fed’s portfolio of mortgage securities came to $20.4 billion last year. The Fed had bought mortgage securities from Fannie Mae and Freddie Mac to lower mortgage rates and bolster the housing market. The program — a centerpiece of the Fed’s efforts to turn around the economy — ended last month.

Two programs the Fed set up during the crisis to ease credit clogs, along with assets it took over with the bailouts of Bear Stearns and American International Group in 2008, generated net earnings of $5.6 billion last year. That marked a turnaround from the net loss of $1.7 billion in 2008.

Of those two crisis-era programs, one involved strengthening the commercial paper market, a crucial short-term financing mechanism companies rely on to pay for everything from salaries to supplies. The other was designed to spur more lending to consumers and small businesses. Virtually all of the Fed’s crisis-era programs have wound down. The one program still in place, which aims to aid the troubled commercial real-estate market, will shut down at the end of June.

- Tweets by @EddyElfenbein

-

-

Archives

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His