-

Where In the Cycle Are We?

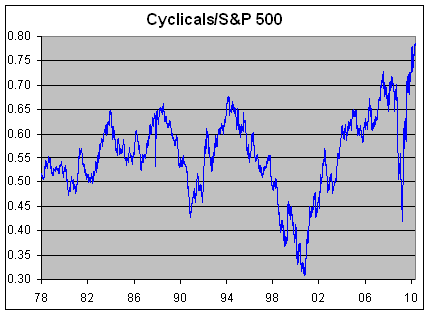

Posted by Eddy Elfenbein on April 21st, 2010 at 2:51 pmOne of the quick-and-dirty metrics I like to look at is the Morgan Stanley Cyclical Index (^CYC) divided by the S&P 500 (^SPX). The Cyclical Index is composed on stocks that are closely tied to the economic cycle. This means industries like autos, chemicals and mining.

When we divided these two indexes, we can tell if cyclicals are outperforming or underperforming. The thing about cyclicals is that they, well, move in cycles. Check out the chart below:

As you can see, there’s historically been a consistent up-and-down wave that averages a few years. This usually, but not always, corresponds with how well the economy is doing. Investors favor cyclicals during the good times, and flee them during the rough patches.

I urge you not to place too much faith in this metric, but I want to show you that the market does, in fact, move in cycles. These are powerful and once the market is locked it, the cycle can last for some time. Therefore it’s important for us to understand where we are in a cycle.

On top of that, the cycle has a double-whammy effect since the market generally does much better when cyclicals are outperforming, meaning they’re outperforming a market that’s already doing well (note the bottoms in 1982, 1990 and March 2009).

You can really see how the last 18 months have dramatically impacted cyclicals. The ratio held up fairly well until September 17, 2009. Within six months, that ratio dropped from 0.7 to 0.42. The Cyclical Index dropped from 871 on September 19 to 283 by March 9. Youch, that’s a staggering loss so you can see that the non-cyclicals provided some shelter from the storm (though not as good as cash).

But once the ratio hit bottom, cyclicals put on an explosive rally. Although the Cyclical Index is still well-below its high from 2007, the ratio has surpassed its high and has gone on to make several all-time highs. That’s about the shortest cycle I’ve ever seen. In fact, it was more like a panic mini-cycle. Last Thursday (pre-Fab), the ratio made its most recent all-time high of 0.786.

Picking cycle peaks is a tricky business and I won’t attempt to do so now, but I’m on the lookout for a harsh drop off in the Cyclical Ratio. Once it gets going, it could down, down, down for a few years. -

Abbott Labs Lowers Guidance

Posted by Eddy Elfenbein on April 21st, 2010 at 10:26 amI’m a big fan of Abbott Labs (ABT), the diversified healthcare company. It’s one of those few companies that consistently churns out steadily growing earnings.

Here are the EPS numbers since 2003; $2.05, $2.27, $2.50, $2.53, $2.84, $3.32 and $3.71. That’s what I like to see, steady increase after steady increase. Except for one bum year in 2006 when they only made $2.53 a share, the rest of the earnings increases were in the double digits.

In January, Abbott said to expect earnings for this year to fall between $4.20 and $4.25 a share. This doesn’t include a 28-cent charge for some acquisition costs and other items.

This morning, the company reported Q1 earnings of 81 cents a share compared with 73 cents a share a year ago. That’s about the growth rate we’ve come to expect from ABT. Sales were up 15%.

Like other healthcare companies, Abbott lowered its full-year guidance due to Obamacare. The company now sees full-year earnings-per-share ranging between $4.13 and $4.18 which is just seven cents off each end. The midpoint is still about 12% higher than last year’s earnings.

I really like Abbott but I’d like to see if come down a little bit more (say, below $50) before I’d call it a really good buy. -

Gilead Takes a Dive

Posted by Eddy Elfenbein on April 21st, 2010 at 10:17 amIt looks like I was wrong about Gilead (GILD) shaking off yesterday’s earnings report. The shares are currently down about 10% this morning. Gilead was also downgraded at Piper Jaffray. I don’t quite get that but I learned a long time ago, never argue with an angry market. I’m not sure what the market expects from them but I still like the stock.

-

U.S. to Get New $100 Bill

Posted by Eddy Elfenbein on April 21st, 2010 at 8:39 am

Cool.Officials from the U.S. Department of the Treasury, the Board of Governors of the Federal Reserve System and the United States Secret Service today unveiled the new design for the $100 note. Complete with advanced technology to combat counterfeiting, the new design for the $100 note retains the traditional look of U.S. currency.

“As with previous U.S. currency redesigns, this note incorporates the best technology available to ensure we’re staying ahead of counterfeiters,” said Secretary of the Treasury Tim Geithner.

“When the new design $100 note is issued on February 10, 2011, the approximately 6.5 billion older design $100s already in circulation will remain legal tender,” said Chairman of the Federal Reserve Board Ben S. Bernanke. “U.S. currency users should know they will not have to trade in their older design $100 notes when the new ones begin circulating.”

There are a number of security features in the redesigned $100 note, including two new features, the 3-D Security Ribbon and the Bell in the Inkwell. These security features are easy for consumers and merchants to use to authenticate their currency.

The blue 3-D Security Ribbon on the front of the new $100 note contains images of bells and 100s that move and change from one to the other as you tilt the note. The Bell in the Inkwell on the front of the note is another new security feature. The bell changes color from copper to green when the note is tilted, an effect that makes it seem to appear and disappear within the copper inkwell.

“The new security features announced today come after more than a decade of research and development to protect our currency from counterfeiting. To ensure a seamless introduction of the new $100 note into the financial system, we will conduct a global public education program to ensure that users of U.S. currency are aware of the new security features,” said Treasurer of the United States Rosie Rios.

“For 145 years, the men and women of the United States Secret Service have worked diligently to protect the integrity of U.S. currency from counterfeiters,” said Director Mark Sullivan. “During that time, our agency has evolved to keep pace with the advanced methodologies employed by the criminals we pursue. What has remained constant in combating counterfeiting, however, is the effectiveness of consumer education initiatives that urge merchants and customers to examine the security features on the notes they receive.”

Although less than 1/100th of one percent of the value of all U.S. currency in circulation is reported counterfeit, the $100 note is the most widely circulated and most often counterfeited denomination outside the U.S.

“The $100 is the highest value denomination that we issue, and it circulates broadly around the world,” said Michael Lambert, Assistant Director for Cash at the Federal Reserve Board. “Therefore, we took the necessary time to develop advanced security features that are easy for the public to use in everyday transactions, but difficult for counterfeiters to replicate.”

“The advanced security features we’ve included in the new $100 note will hinder potential counterfeiters from producing high-quality fakes that can deceive consumers and merchants,” said Larry R. Felix, Director of the Treasury’s Bureau of Engraving and Printing. “Protect yourself – it only takes a few seconds to check the new $100 note and know it’s real.”

The new design for the $100 note retains three effective security features from the previous design: the portrait watermark of Benjamin Franklin, the security thread, and the color-shifting numeral 100.

The new $100 note also displays American symbols of freedom, including phrases from the Declaration of Independence and the quill the Founding Fathers used to sign this historic document. Both are located to the right of the portrait on the front of the note.

The back of the note has a new vignette of Independence Hall featuring the rear, rather than the front, of the building. Both the vignette on the back of the note and the portrait on the front have been enlarged, and the oval that previously appeared around both images has been removed. -

Earnings from Stryker and Gilead

Posted by Eddy Elfenbein on April 20th, 2010 at 5:23 pmThe stock market continues to recover from last Friday’s sell-off. The S&P 500 is now just slightly below its pre-Fab high from last Thursday. Our Buy List also continues to do well. We were up 0.72% today to bring us up to +14.02% for the year (not including dividends).

Two of our Buy List stocks reported after the bell (JNJ reported earlier). Gilead Sciences (GILD) reported earnings of 99 cents per share which beat the Street’s estimate of 96 cents per share. Revenues jumped 36.3% to $2.09 billion. That’s a very good number. Gilead also lowered its sales outlook for the year by $200 million due to Obamacare. The stock is down about 2% in the after-hours market but I don’t expect that to last. The stock is now going for about 12 times this year’s earnings estimate. This is a very good buy.

The other news is that Stryker (SYK) reported earnings of 80 cents per share which was two cents more than the Street’s estimate. Revenues were up 12.4% to $1.8 billion. Stryker said it expects full-year EPS of $3.20 to $3.30. This reiterates the guidance they made in January. I always like to hear companies confirm guidance. This just lets shareholders know where they stand. Even saying “what we said before still stands” is nice to hear. For 2009, SYK earned $2.95 per share. Stryker is another very good buy. -

The Absolute Worst Stock to Buy Right Now

Posted by Eddy Elfenbein on April 20th, 2010 at 12:50 pm

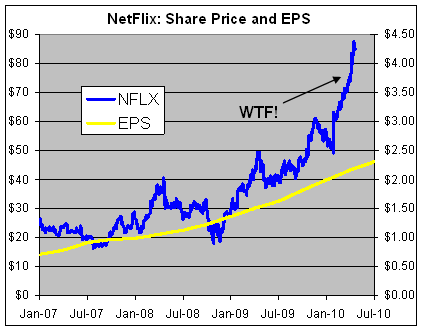

Lots of folks on Wall Street want to know which stock to buy. Today, I want to look at the absolute worst one to buy. My friends, that stock is Netflix (NFLX).

Now before anyone says that I’m being mean to the company, please bear in mind that I’m not offering a judgment on the managers or the employees. There’s a very big difference between a good company and a good stock. Netflix has a business record that anyone should be proud of. The stock, however, is terribly, terribly overpriced.

Let’s look at some numbers. Last year, Netflix made $115.9 million of sales of $1.67 billion. That works out to earnings of $1.98 a share. The stock, however, is currently around $86 or 43 times trailing earnings. The shares were overpriced at the start of the year and they’re up another 55% since then.

When the fourth-quarter earnings came out in January, Netflix said that it expects full-year earnings-per-share for 2010 to range between $2.28 and $2.50. So even going by the top end of forward earnings, NFLX is still trading with a P/E ratio of around 35 which is more than twice the S&P 500. That’s just crazy.

Netflix also said that it expects revenues between $2.05 and $2.11 billion. That’s a growth rate of 23% to 26% which is slightly better than last year’s 22%. The problem with the valuation is that a lot of NFLX’s earnings growth has come from profit-margin expansion. That’s a very good thing to have, but I’m skeptical of how much more that can improve without the company exposing itself to potential rivals like Redbox. On top of that, business could be hurt by higher postal rates and the elimination of Saturday delivery. Also, companies like Walmart (WMT), Amazon (AMZN) and Best Buy (BBY) loom in the background.

Netflix’s net margins improved from 5.6% in 2007 to 6.1% in 2008 to 6.9% last year. Earnings are coming out tomorrow and it could be bad news. I have little doubt that the company will top the Street’s expectations of 54 cents pet share. In January, Netflix said to expect Q1 earnings between 47 and 58 cents per share. With the stock so high, NFLX has zero room for error. The stock is simply far too high to expect a reasonable return.

If you own Netflix, you ought to sell it as soon as possible. The next 12 months won’t be pretty.

The chart above has NFLX’s stock in the blue line which follows the left scale. The right scale has the EPS line which is in yellow. The two lines are scaled at 20-to-1 which means when the lines cross, the P/E Ratio is exactly 20. -

Remembrance of Stocks Past

Posted by Eddy Elfenbein on April 20th, 2010 at 12:16 pmAt the end of last year, I decided to remove Amphenol (APH) from our Buy List. The stock had a great run in 2009 as it gained 91%. Even though I still like the company, which makes electronic and fiber optic connectors, I thought the stock needed to rest.

It looks like I was right. Through yesterday’s close Amphenol was down 5% for the year. I’m happy to see that the stock is up nicely today on news of very strong earnings.The company earned $98.4 million, or 56 cents per share, up 32 percent from $74.4 million, or 43 cents per share, in the same period a year earlier.

Excluding a tax-related gain, it earned 55 cents per share in the latest quarter.

Revenue rose 17 percent to $771 million from $660 million. Currency translation boosted sales by about 2 percent, or $15 million.

Analysts, on average, were expecting a profit of 51 cents per share on revenue of $749.2 million, according to a poll by Thomson Reuters.If business continues to improve the stock is reasonably priced, I’d love to welcome APH back to the Buy List.

Another former Buy List stock, Harley Davidson (HOG), is having a good day. The stock was a member of the Buy List in 2006, 2007 and 2008. HOG did well in 2006, but after that, it was an awful pick for us. I let it go last year and, wouldn’t you know, the shares sprung to life so my timing with HOG isn’t so good.

Today’s news is that profits plunged…but beat expectations!!Harley-Davidson Inc. said Tuesday its first-quarter profit fell 72 percent as sales of its high-end bikes remained sluggish.

Harley-Davidson CEO Keith Wandell said the uncertain economy is likely to make business conditions challenging throughout the year.

Still, the Milwaukee company’s results beat analysts’ forecasts, and investors were cheered by a return to profitability at its financial services unit. The stock gained $2.58, or 7.9 percent, to $35.35 in morning trading.

Harley-Davidson reported a profit of $33.3 million, or 14 cents per share, in the three months ended March 28. That’s down from $117.3 million, or 50 cents per share, during the same period last year.

Excluding losses from discontinued operations, the Milwaukee company made 29 cents per share. Revenue during the quarter fell 19 percent to $1.04 billion.

Analysts expected a profit of 22 cents per share on $1.02 billion in revenue. Such estimates typically exclude one-time items.HOG is now up more than four-fold from its March 2009 low. Before I’d add it to the Buy List, I’d like to see its profits growing again.

-

Midday Market Update

Posted by Eddy Elfenbein on April 20th, 2010 at 11:40 amVery solid gains this morning. The Buy List is up over 0.5% so far today. We’ve seen new 52-week highs from Sysco (SYY) and Fiserv (FISV). We’re still waiting on earnings reports from Stryker (SYK) and Gilead Sciences (GILD).

The S&P 500 has been as high as 1,205.65 today which isn’t very far from its pre-Fabulous Fabrice Tourre high of 1,213.92. -

Goldman Sachs Earns $3.46 Billion

Posted by Eddy Elfenbein on April 20th, 2010 at 10:34 amAnother day on Wall Street, and we’re still talking about Goldman Sachs (GS). To reiterate, I don’t think Goldman is a good buy right now.

Goldman is still doing what it does best—making ridiculous amounts of money. Earnings for the first quarter nearly doubled to $3.46 billion. That comes to $5.59 a share which creamed Wall Street’s estimate of $4.14 a share.

Goldman has always been a bit of a black box so the Street’s earnings estimates can be wildly off the mark. Still, this is a phenomenon ally wealthy firm. The firm’s conference call was dominated by questions about the SEC’s investigation.

I remain unimpressed by the SEC’s case against Goldman Sachs. This seems to be a very well-timed charge especially considering that financial reform has taken center stage in Washington. We also just learned that the SEC dragged its feet on the Allen Stanford case for over 10 years. Furthermore, the SEC vote on the Goldman charge was 3-to-2, so even folks in the government see how thin this case is.

Bloomberg says that the Goldman case may come down to what the meaning of the word “selected” is.The Securities and Exchange Commission must prove that the most profitable company in Wall Street history defrauded investors by failing to disclose that a hedge-fund firm betting against them played a role in creating what they bought. It must also counter Goldman Sachs’s assertion that an independent asset manager, which the SEC said rejected more than half of the securities initially proposed by Paulson & Co. for a collateralized debt obligation, signed off on the selections.

“The question is whether Paulson’s undisclosed role in portfolio selection was material,” said Larry Ribstein, a law professor at the University of Illinois in Champaign who has written about 140 articles and 10 books on topics including securities law and professional ethics. “There’s no clear and well-defined definition of what you have to disclose in this type of transaction.”So the 90s was about the definition of “is” and this decade is about the definition of “selected.” Not sure if we’ve improved.

-

Johnson & Johnson Earns $1.29 a Share

Posted by Eddy Elfenbein on April 20th, 2010 at 9:58 amGood news and bad news this morning from Johnson & Johnson (JNJ), one of our Buy List stocks. The good news is that the company reported Q1 earnings of $1.29 per share which beat Wall Street’s estimate by two cents a share. Woo hoo! Revenues rose by 4% to $15.63 billion which was a teeny bit better than expectations.

The bad news is that the company pared back its full-year EPS guidance due to foreign exchange rates. JNJ’s initial full-year guidance was a range of $4.85 to $4.95. They’ve pulled each end down a nickel to a new range of $4.80 to $4.90.

Truthfully, the bad news isn’t very bad. I’m never terribly worried about things outside a company’s control like foreign exchange. If they had experienced an issue related to their operations, that would have been one thing. Foreign exchange is one of those things you simply have to deal with. Sometimes it helps you, sometime it doesn’t. It’s a bit like playing against the wind in football.

The lowered guidance also includes the impact of Obamacare which JNJ pegs at 10 cents per share and a revenues loss of $400 million. Overall, JNJ is still trading at less than 14 times this year’s estimate which is less than the broader market. JNJ remains an excellent buy.

- Tweets by @EddyElfenbein

-

-

Archives

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His