-

Happy Birthday Mr. Bull!

Posted by Eddy Elfenbein on March 9th, 2010 at 10:29 am

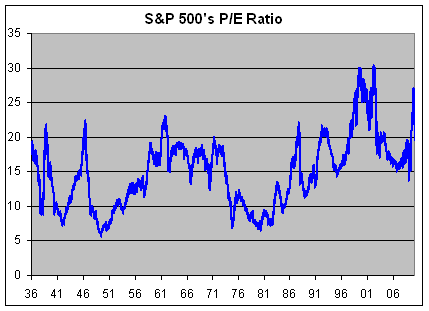

On the first anniversary of the bull market, E.S. Browning looks at the valuation debate between economists Robert Shiller and Jeremy Siegel. Not surprisingly, Dr. Shiller thinks the stock market is expensive and Dr. Siegel thinks it’s cheap.

Both men have held their positions for quite some time. For the last decade, Shiller has clearly won the debate (while Dr. Siegel has made some sloppy mistakes).

Despite Shiller’s accuracy, I’m skeptical of his methodology (after all, a person can be right for the wrong reasons). He relies on the market’s P/E Ratio with earnings going back 10 years. That seems too far for me. Plus, I suspect (both I’m not convinced) that earnings multiples need to be higher compared with decades ago. Shiller is very good at getting tons of data, often from many decades ago, but I’m not so sure such long-term comparisons are helpful. The economy and markets are quite different from the 19th century. Stocks are much safer compared with bonds and that difference should be reflected in valuations.

In fact, higher earnings multiples are nothing new for the market provided that you ignore the inflation racked period from 1966 to 1982. Earnings multiples started to rise in the 1950s and reached very elevated levels in the early 1960s. I think people forget that because the market didn’t suffer a severe reckoning until the 1970s (though there were some painful episodes in between).

Once inflation started creeping into the economy, interest rates soared and earnings multiples took a tumble. However, once Paul “Big Paul” Volcker squeezed inflation from the economy, multiples slowly resumed their climb back to JFK levels. The problem with that analysis, of course, is that you’re adjusting for a heck of a lot of data. So has the normal level for P/E Ratios been around 18 or so for the past 50 years with the inflation era as an aberration? Or are there natural 15 to 20 year periods of multiple expansion and compression? I lean toward the first, but I’m far from certain.

Siegal’s research centers around the fact that stocks have returned 7% a year adjusted for inflation. I’ve used that figure myself many times and it’s interesting to see how we’re doing against the long-term trend. In fact, when you adjust the market’s total return against a 7% trend line, it looks suspiciously like a P/E Ratio chart.

The problem with this method is that it assumes past data is an unbroken trend and all subsequent deviations have been corrected by reversions to the mean. That’s where I hold up a red flag. On top of that, the deviations from the long-term trend are very extreme. If the market can be so vastly out-of-whack from where it should be and for so long, then what’s the point? As an investor, I want to know what looks good right now.

My view is that I’m leery of all market forecasts. I tend to be on the bullish side simply because long-term interest rates continue to be low (Moody’s AAA Corporate Bond Index is currently around 5.2%), the market doesn’t expect a major resurgence of inflation anytime soon (the TIPs spread is fairly quiet) and the yield curve continues to be very wide (all of the market’s capital gains have come when the 3-month/10-year Treasury spread is over 65 basis points—the spread is currently at 355 points).

Still, I’m not investing in the entire market. My advice for investors continues to be to focus on high-quality stocks. The market’s dislocation has left us some bargains. Some of my favorite stocks include AFLAC (AFL), Nicholas Financial (NICK), Dean Foods (DF) and Reynolds American (RAI). -

Missing Home Depot

Posted by Eddy Elfenbein on March 8th, 2010 at 12:15 pmUgh, how did I not see Home Depot (HD)? The stock is at a new 52-week high today.

Actually, I did see it but still didn’t pull the trigger. These are the trades that really annoy me. Here’s what I wrote last June after HD raised guidance:Last year, HD earned $1.78 a share. In May, the company said that it expects to see EPS fall by 26% and sales to fall by 9%. That translates to full-year earnings of $1.32. Today they said to expect EPS to fall by 20% to 26%. A 20% drop works out to $1.42 which is slightly above Wall Street’s consensus of $1.40.

Make no mistake, this isn’t great news but it’s not awful and all the news until now has been awful. HD’s earnings peaked in 2007 at $2.83 a share so we’re going to see earnings fall in half—so has the stock price.

At its current price, I wouldn’t say Home Depot is a good buy, but it’s not unreasonable to see year-over-year earnings increases within a few quarters. If there’s more good news from HD, it could be a good buy before the end of the year.The good news did come. HD beat earnings in August, November and a very nice beat a few weeks ago (24 cents per share vs. 17 cents per share), but moron me didn’t step it up.

The shares dipped below $25 in early November and it’s been off to the races ever since. Since November 4, HD is up 28% compared with 9% for the S&P 500. I let that one get away. -

The Bull Market Turns One

Posted by Eddy Elfenbein on March 8th, 2010 at 10:22 amThis is going to be a big week for market anniversaries.

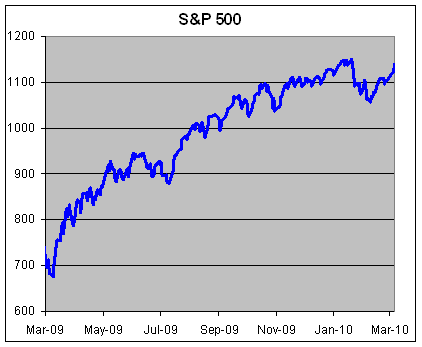

Tomorrow is the first anniversary of the bull market. The S&P 500 closed March 9, 2009 at 676.53. That was a Monday. During the day on the previous Friday, March 6, the index got to its spooky intra-day low of 666.79.

The day after tomorrow is the seventh anniversary of the 2003 market low. On March 11, 2003, the S&P 500 closed at 800.73. The intra-day low came the follow day at 788.90.

This month will also market the tenth anniversary of the bull market high of 2000. The S&P 500 reached its closing peak of 1527.46 on March 24. However, the index that everyone was watching back then was the Nasdaq which marked its closing high of 5,048.62 ten years ago this Wednesday.

We’re still than half of where we were. -

SEI Investments Rallies on Upgrade

Posted by Eddy Elfenbein on March 8th, 2010 at 10:00 amSo far, it’s a good morning for our stocks on the Buy List. SEI Investments (SEIC) is up over 4% thanks to an upgrade from Janney Montgomery Scott. It’s about time someone noticed them. Also, Jos. A Banks (JOSB) just announced it’s “risk-free” promotion:

JoS. A. Bank Clothiers, Inc. announces it is bringing back its popular “Risk Free” promotion. As part of the promotion, the Company will refund the price of a suit or sportcoat if the purchaser loses his job, and also allow him to keep the garment.

“We believe that our customers will appreciate another opportunity to look great at work and at the same time be assured that their purchase will be free if they lose their job,” stated R. Neal Black, President and CEO of JoS. A. Bank. “We think our 5.2 million customers and potential new customers deserve our support in these uncertain times,” continued Mr. Black. -

The Power of Long-Term Investing

Posted by Eddy Elfenbein on March 8th, 2010 at 9:35 amIn 1935, Grace Goner invested $180 in Abbott Labs (ABT). She died earlier this year at the age of 100.

Oh..and those ABT shares: $7 million.Like many people who lived through the Great Depression, Grace Groner was exceptionally restrained with her money.

She got her clothes from rummage sales. She walked everywhere rather than buy a car. And her one-bedroom house in Lake Forest held little more than a few plain pieces of furniture, some mismatched dishes and a hulking TV set that appeared left over from the Johnson administration.

Her one splurge was a small scholarship program she had created for Lake Forest College, her alma mater. She planned to contribute more upon her death, and when she passed away in January, at the age of 100, her attorney informed the college president what that gift added up to.

“Oh, my God,” the president said. -

Today’s Jobs Report

Posted by Eddy Elfenbein on March 5th, 2010 at 2:39 pmHere’s a strange statistical angle to today’s jobs report. Officially, the unemployment rate was unchanged, 9.7%. But you break down the numbers, the rate was eerily the same.

For January, the unemployment rate was 9.68662%. For February, it was 9.68719%.

That’s an increase of 57/100,000 of one percent. Think of it this way: If the workforce had remained at 175,000 for January and February, then only person lost his job.

I’m not trying make any economic point, I just think it’s an unusual statistical occurrence. -

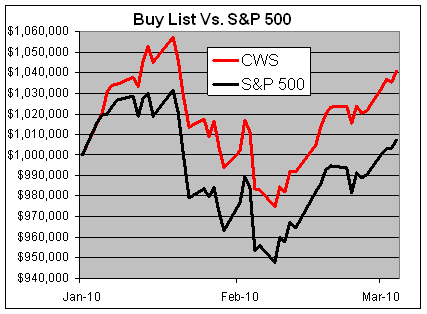

The Buy List YTD

Posted by Eddy Elfenbein on March 4th, 2010 at 4:37 pmIt’s early but the Buy List has gained 4.06% so far this year. The S&P 500 is up just 0.71%.

-

The Day Trader With 40 Computer Screens

Posted by Eddy Elfenbein on March 4th, 2010 at 2:05 pm -

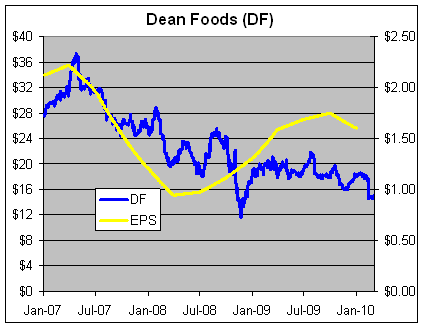

Dean Foods

Posted by Eddy Elfenbein on March 4th, 2010 at 1:57 pmI’ve been looking at Dean Foods (DF) as an attractive value play. Like a lot of value stocks, this company is not without its bruises. The company’s recent earnings history has not been very terribly strong. Still, they are making money and the stock is so beaten down that it could rally 10%-20% from here and still be seen as a bargain.

Dean is a large and well diversified food company. They own about a zillion brands. Despite that lackluster earnings, they are profitable which says a lot in a rough economy. Dean has bought up a ton of businesses over the past several years and they now find themselves fighting not one, not two, but three anti-trust battles. On top of that margins are under attack thanks to retailers using milk as a loss-leader to get folks in the door.

Last month, the company said it earned $1.59 for all 2009. For 2010, Dean said they expect EPS to range between $1.54 and $1.64. The mid-point, of course, is exactly what they made last year. So that means they don’t expect any growth. Still, the stock is going for less than 10 times next year’s earnings. Considering what you can get in the bond market right now, that’s not so bad. For Q1, Dean expects EPS between 25 cents and 30 cents.

The bottom line is that Dean is in rough shape right now, but it things start to turnaround by the middle of 2011, the stock could rally quite handsomely. -

Should Greece Sell Some Islands to Pay Its Debt?

Posted by Eddy Elfenbein on March 4th, 2010 at 12:05 pmSome politicians are floating the idea of Greece selling some of its islands to pay down its debt. The only problem is that the aforementioned politicians aren’t Greek but German.

“The bankrupt one has to do everything he can to make money for the sake of his creditors,” said Josef Schlarmann, a member of Angela Merkel’s Christian Democrat party who heads a lobby of small and midsize businesses that back the CDU. “Greece possesses buildings, businesses and uninhabited islands, which can be used to pay down debt.”

The sentiment was echoed by Frank Schaeffler, a financial expert with the CDU’s coalition partner the FDP. “The chancellor can’t break the law, and may not promise Greece aid. The Greek state needs to get rid of stakes in businesses and sell real estate — e.g. uninhabited islands.”To be fair to the Germans, they’ve always had some difficulties with the concept of sovereignty.

- Tweets by @EddyElfenbein

-

-

Archives

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His