-

Wright Express Beats By Two Cents

Posted by Eddy Elfenbein on February 12th, 2010 at 10:39 amOn Wednesday, Wright Express (WXS), one of the new stocks on this year’s Buy List, reported Q4 earnings, after costs, of 56 cents a share which was two cents higher than estimates. For 2009, net income pre share rose to $2.18 from $1.88 last year.

On the earnings call, this is what they had to say about future projections:For the first quarter of 2010 we expect to report revenues in the range of 82 to $87 million. This is based on an average retail sales price of $2.78 per gallon. For the full year 2010, we expect revenues ranging from 360 to $370 million based on an average retail sales price of $2.80 per gallon.

In terms of earnings for Q1 of 2009 we expected to report adjusted net income in the range of $21 to $23 million or $0.53 to $0.58 per diluted share. We expected adjusted net income for the full year 2010 in the range of 89 to $97 million or $2.26 to $2.46 per diluted share and approximately 39 million shares outstanding.If we take $2.36 as the midpoint, that means the stock is going for about 12 times this year’s earnings. The stock dropped initially on the news but rallied back yesterday. So far, it’s our biggest loser of the year.

-

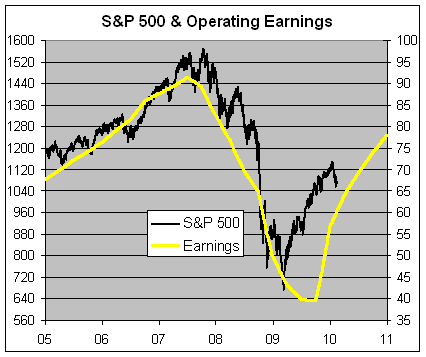

The S&P’s P/E Ratio Falls to 18

Posted by Eddy Elfenbein on February 12th, 2010 at 9:13 amWith the recent dip in the stock market, the P/E Ratio of the S&P 500 is now down to 18. That number, however, is a bit misleading since earnings are still in the process of recovering from a nasty downturn.

Here’s a look at the S&P 500 (left scale) along with its earnings line (right scale). The two scales are plotted at a ratio of 16-to-1 so when the lines cross, the P/E Ratio is exactly 16. The future earnings line is S&P’s estimate.

The total earnings for 2009 will be about $57. Bear in mind that at one point, Goldman Sachs thought that it would be $40. I still think stocks are a good buy, but this is an instance where looking at the P/E ratio doesn’t tell us much. The recent earnings trend is such an outlier. Naturally, if the earnings forecast holds up, then I would expect stocks to be much higher one year from now.

Remember that stocks are best measured by their alternatives. In this case, I think the more telling metric isn’t the Price/Earnings, but the yield curve. The spread between the 30-year T-bond the 90-day T-bill is over 450 basis points, which is gigantic. Even at 5-years out, a Treasury only offers a yield of about 2.3%. With the kind of competition, stocks are the best investment. -

Unraveling the Profit Puzzle at Goldman Sachs

Posted by Eddy Elfenbein on February 12th, 2010 at 9:10 am -

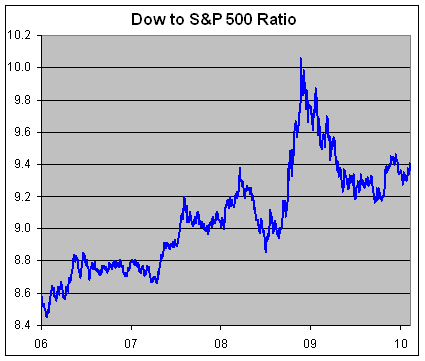

Despite 10,000, the Dow Has Been Beating the S&P 500

Posted by Eddy Elfenbein on February 9th, 2010 at 11:48 amYesterday, the Dow closed below 10,000 for the first time in three month. As far as indexes go, I’m not a big fan of the price-weighted Dow. The cap-weighted S&P 500 is far superior.

Still, I will give the Dow credit for beating the S&P 500 over the past four years. Here’s a look at the Dow/S&P 500 Ratio:

For two days in November 2008, the ratio closed above 10. Before that, the ratio had last been above 10 in 1966. -

Goldman Goes A-Blogging

Posted by Eddy Elfenbein on February 9th, 2010 at 11:00 amGoldman Sachs’ spokesman, Lucas van Praag, responds to the NYT’s article at the Huffington Post. Here’s a sample:

NYT assertion: “Goldman’s demands for billions of dollars from the insurer helped put it in a precarious financial position by bleeding much-needed cash.”

The facts: Relative to the size of AIG’s overall business, Goldman Sachs was a small counterparty. We don’t believe our marks were “aggressive,” they reflected market prices at the time. We requested the collateral we were entitled to under the terms of our agreements. The idea that AIG collapsed because of our marks is not credible. In any event, the story later asserts that, by the spring of 2008, AIG’s dispute with Goldman Sachs was just one of its many woes.

NYT assertion: “In addition, according to two people with knowledge of the positions a portion of the $11 billion in taxpayer money that went to Societe Generale, a French bank that traded with A.I.G, was subsequently transferred to Goldman under a deal the two banks had struck.”

The facts: The assertion is false and misleading. Goldman Sachs provided financing to many counterparties, but in that role we would not have known whether a counterparty had obtained credit default protection, let alone from whom or in what amount.(HT: Felix)

-

The Geography of a Recession

Posted by Eddy Elfenbein on February 8th, 2010 at 2:02 pm -

Academic Study on Media Bias in Financial Newspapers

Posted by Eddy Elfenbein on February 8th, 2010 at 1:21 pmMedia Bias in Financial Newspapers: Evidence from Early-Twentieth-Century France

Abstract:

The financial market was well developed in France in the years before World War I, and there were many newspapers that provided information to investors. Yet commentators at the time faulted the financial press for inaccuracy and biases, which they linked to the existence of payments made by companies for coverage in the editorial section. This paper tests whether the payment scheme induced a systematic bias in the coverage of companies listed on the Paris stock exchanges by newspapers. The results show that, although firms’ media coverage was affected, the performance of firms actually touted by the press was good. Thus, the media bias can also be explained by newspapers choosing the companies’ exposures according to their editorial policy. -

Mortgage Bankers Association Sells Headquarters at Big Loss

Posted by Eddy Elfenbein on February 8th, 2010 at 11:58 amOuch.

On Friday, CoStar Group Inc., a provider of commercial real estate data, announced that it had agreed to buy the MBA’s 10-story headquarters building in Washington, D.C., for $41.3 million. The price is far below the $79 million the trade group says it paid for the glass-walled building in 2007, while it was still under construction. The price also is far below the $75 million financing that the MBA received from a group of banks led by PNC Financial Services Group Inc. to finance the purchase.

-

Telegraph: Roubini Gets It Wrong

Posted by Eddy Elfenbein on February 8th, 2010 at 11:49 amThere’s finally some big media pushback against the Great Predictors, all of whom missed one of the greatest stock rallies in history:

Never mind what Nouriel Roubini, the New York economist credited with having seen the economic meltdown coming, is predicting for next year – surprise, surprise, he’s pessimistic – let’s take a look at what he forecast at the time of the World Economic Forum in Davos this time last year.

Er, well, the great sooth sayer and now standing feature of this mountain top conference for the elite of business and finance thought that even if governments and central bankers did everything right in terms of fiscal and monetary policy, we’d all still be in recession across the advanced economies for all of 2009 and 2010. And for sure, the S & P was going to 600. Admittedly, it did get as low as 650, but now it’s back above 1,000. If you’d listened to Mr Roubini, you would have missed out on one of the greatest stock market rallies ever. As for recession, some economies were growing again by the second quarter of last year, and even Britain is now showing marginal growth.

Still, these forecasting errors are perhaps forgiveable for one who got the big call spot on. Except that he was making it as far back as 2002. Which all goes to show that if you say something consistently enough for long enough, eventually you will be proved right.(HT: TBI)

-

The Goldman/AIG Battle

Posted by Eddy Elfenbein on February 8th, 2010 at 11:44 amThe must-read story of the weekend was Gretchen Morgenson and Louise Story’s account of the battle between Goldman Sachs and AIG.

I have no independent love for Goldman Sachs and I’m perfectly happy to portray them as the villain. Still, I keep finding myself being attractive to another narrative—Goldman was smarter than everyone else.

Yves Smith and Tom Adams have more.

- Tweets by @EddyElfenbein

-

-

Archives

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His