-

Still At Zero

Posted by Eddy Elfenbein on January 27th, 2010 at 4:45 pmHere’s the latest Fed statement:

Information received since the Federal Open Market Committee met in December suggests that economic activity has continued to strengthen and that the deterioration in the labor market is abating. Household spending is expanding at a moderate rate but remains constrained by a weak labor market, modest income growth, lower housing wealth, and tight credit. Business spending on equipment and software appears to be picking up, but investment in structures is still contracting and employers remain reluctant to add to payrolls. Firms have brought inventory stocks into better alignment with sales. While bank lending continues to contract, financial market conditions remain supportive of economic growth. Although the pace of economic recovery is likely to be moderate for a time, the Committee anticipates a gradual return to higher levels of resource utilization in a context of price stability.

With substantial resource slack continuing to restrain cost pressures and with longer-term inflation expectations stable, inflation is likely to be subdued for some time.

The Committee will maintain the target range for the federal funds rate at 0 to 1/4 percent and continues to anticipate that economic conditions, including low rates of resource utilization, subdued inflation trends, and stable inflation expectations, are likely to warrant exceptionally low levels of the federal funds rate for an extended period. To provide support to mortgage lending and housing markets and to improve overall conditions in private credit markets, the Federal Reserve is in the process of purchasing $1.25 trillion of agency mortgage-backed securities and about $175 billion of agency debt. In order to promote a smooth transition in markets, the Committee is gradually slowing the pace of these purchases, and it anticipates that these transactions will be executed by the end of the first quarter. The Committee will continue to evaluate its purchases of securities in light of the evolving economic outlook and conditions in financial markets.

In light of improved functioning of financial markets, the Federal Reserve will be closing the Asset-Backed Commercial Paper Money Market Mutual Fund Liquidity Facility, the Commercial Paper Funding Facility, the Primary Dealer Credit Facility, and the Term Securities Lending Facility on February 1, as previously announced. In addition, the temporary liquidity swap arrangements between the Federal Reserve and other central banks will expire on February 1. The Federal Reserve is in the process of winding down its Term Auction Facility: $50 billion in 28-day credit will be offered on February 8 and $25 billion in 28-day credit will be offered at the final auction on March 8. The anticipated expiration dates for the Term Asset-Backed Securities Loan Facility remain set at June 30 for loans backed by new-issue commercial mortgage-backed securities and March 31 for loans backed by all other types of collateral. The Federal Reserve is prepared to modify these plans if necessary to support financial stability and economic growth.

Voting for the FOMC monetary policy action were: Ben S. Bernanke, Chairman; William C. Dudley, Vice Chairman; James Bullard; Elizabeth A. Duke; Donald L. Kohn; Sandra Pianalto; Eric S. Rosengren; Daniel K. Tarullo; and Kevin M. Warsh. Voting against the policy action was Thomas M. Hoenig, who believed that economic and financial conditions had changed sufficiently that the expectation of exceptionally low levels of the federal funds rate for an extended period was no longer warranted. -

Gilead Sciences Leads Our Buy List Higher

Posted by Eddy Elfenbein on January 27th, 2010 at 10:38 amThe market is somewhat soggy this morning, but our Buy List is being helped by a very strong earnings report from Gilead Sciences (GILD). For the fourth-quarter, the company earned 93 cents a share which easily beat Wall Street’s estimate of 85 cents a share. The company now projects 2010 net products sales of $7.6 billion to $7.7 billion, which translates to a growth rate of 17% to 19% for this year. Wall Street had been forecasting earnings of $3.31 a share for this year, but that will now increase.

The shares have been up by as much as 6.6% today. Here’s a look at the earnings call from Seeking Alpha

The other earnings report was from Stryker (SYK), and that wasn’t so strong. On absolute terms, they did just fine as they almost always do. Stryker earned 82 cents a share but that merely matched Wall Street’s consensus. They reiterated their 2010 outlook of $3.20 to $3.30 per share. I’m fine with that but I guess investors wanted a little more.

Here’s the CEO on CNBC this morning.

.

Stryker is down about 4% this morning. -

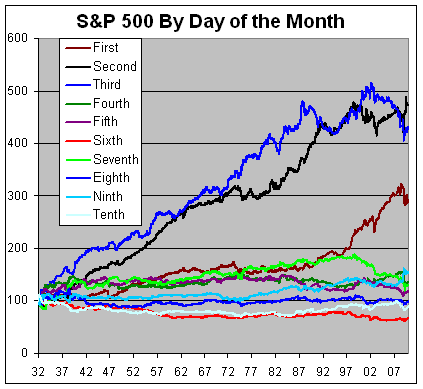

Investing By Day of the Month

Posted by Eddy Elfenbein on January 26th, 2010 at 10:12 pmHere’s a breakdown of how well the stock market has performed during the first 10 trading days of the month. Each line is based on S&P 500’s cumulative gain on each particular trading day of the month (i.e., being long on the X day of the month, then all cash until the X day of the following month).

The clear winners are the first three days of the month. In fact, stocks aren’t worth the bother for the next seven days. (I know the last few days of the month are also quite good, but I’ll look at that another time.)

If you had invested solely during the first three days of each month, you would have made 5,824% (dividends not included) over the last 78 years. Even though this represents a small sliver of time (about 13.7%), it’s still a hefty portion of the S&P 500 gain which is about 14,000%.

The combined return of the fourth through tenth day is a tad over 100% which is less than inflation.

Here’s a breakdown of the average daily gains:Day Gain First 0.115% Second 0.166% Third 0.155% Fourth 0.033% Fifth 0.018% Sixth -0.042% Seventh 0.029% Eighth 0.000% Ninth 0.046% Tenth -0.011% To give you a reference point, a daily return of 0.1% works out to over 28% a year.

-

J&J’s Earnings Beat the Street

Posted by Eddy Elfenbein on January 26th, 2010 at 11:31 amJohnson & Johnson (JNJ) reported fourth-quarter earnings of $1.02 a share which was five cents higher than Street forecasts.

Fourth-quarter sales rose 9% to $16.55 billion, also exceeding Wall Street expectations. Favorable currency-exchange comparisons contributed 4.5 percentage points of the growth, reversing the currency headwinds that J&J and other multinational drug companies had faced in previous quarters.

J&J’s biggest unit, medical devices and diagnostics, had sales of $6.31 billion, up 11.8%. Pharmaceutical sales rose 5.4% to $5.99 billion, while consumer-product sales rose 10.2% to $4.25 billion.

For the full year, J&J said it earned $4.63 a share excluding items, which exceeded the forecast range J&J had provided in October, of earnings between $4.54 and $4.59 a share. Full-year sales were $61.9 billion, in line with the forecast range of $61 billion and $62 billion.

J&J said it expects 2010 earnings of $4.85 to $4.95 a share, excluding certain items.That means that JNJ is going for about 12.8 times this year’s earnings estimates which is about 13% less than the S&P 500.

-

Odd Lots

Posted by Eddy Elfenbein on January 25th, 2010 at 3:38 pmSEC mulled national security status for AIG details

Abnormal Returns & Stocktwits!!

Home sales tumble as tax credit lift wanes

Feinstein throws her support behind Fed chairman Bernanke

The President’s Bank Reforms Don’t Add Up

Reviews of Crossing Wall Street at Investimonials

Clearwater woman called 911 saying she was tired of her husband -

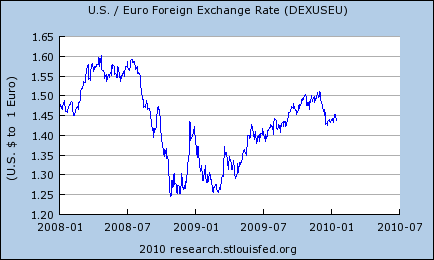

About That Plunging Dollar

Posted by Eddy Elfenbein on January 25th, 2010 at 2:52 pmI hear all the time about the plunging dollar, but if it has plunged, I’m afraid I missed it. You’d never know this by listening to the rhetoric, but the dollar lost only -2.9% against euro last year. The year before that, the dollar gained 4.9% against the euro. Doesn’t sound like a plunge to me.

(The chart above is dollars-per-euro, so a downward line means a strengthening dollar.) -

AXA to Delist from NYSE

Posted by Eddy Elfenbein on January 25th, 2010 at 10:55 amThe French insurance company, AXA (AXA) has announced that it will delist from the NYSE due to lacking of trading volume. This strikes me as very bad news for New York and the American market. I would think that at least some American investors would be interested in trading a $45 billion insurance company. Based on revenue, this is one of the largest companies in the world.

Is this solely about trading volume, or are the French concerned about our regulatory climate? -

Should You Listen to Your Broker?

Posted by Eddy Elfenbein on January 25th, 2010 at 10:34 amNew research shows that you should pay careful attention to what your stock broker says.

Then do the exact opposite.It turns out, there is information in analyst forecasts, specifically, shorting your broker. In Long-Term Earnings Growth Forecasts, Limited Attention, and Return Predictability by Da and Warachka, they find that if you take the long-run earnings growth and divide by the recent earnings growth, you get a straightforward metric of optimism: higher is more optimistic. It turns out, the highest decile has a 4% annualized lower risk-adjusted return than the lowest decile; more optimistic stocks have lower returns.

A simple explanation (see here) is that mutual funds “herd” (trade together) into stocks with consensus analyst upgrades and (especially) herd out of stocks with consensus downgrades. Stronger fund herding occurs when analyst recommendation revisions are more unanimous.

However, there is some information that analyst recommendations are more useful at the industry level. Portfolios long in industries about which analysts are optimistic and short in industries about which analysts are pessimistic generate significant abnormal returns (see here).

So, listen to your broker’s advice on sectors and stocks, just remember to short the stock picks. -

Four More Years

Posted by Eddy Elfenbein on January 25th, 2010 at 10:28 amThe stock market is rebounding this morning and the news that it appears that Ben Bernanke will be confirmed for another term as Fed chair, though of course, it’s hard to tie any one-day rally to a specific news item.

I think the anger at Bernanke closely resembles the Two-Minute Hate Sessions in George Orwell’s 1984. Americans are rightfully angry, but they don’t know exactly who to be angry. They were angry at George Bush and he’s not around. Alan Greenspan? He’s also gone. That leaves Ben Bernanke.

If having him reconfirmed by a whisker placates enough folks, I’m fine with that. But rejecting Bernanke would be an awful, awful move. Consider the take of one Nebraska-based investor:CNBC:….Should he be confirmed?

Buffett: If I could vote twice I would. He should be. He did a magnificent job over this period… We can’t sit here and armchair quarterback him. But when we look back at September and October 2008, he took some extraordinary actions….we talked about it being an economic pearl harbor. He did what he should have done in response.

Q: What happens if he’s not recommended?

Buffett: Well, just tell me a day ahead of time so I can sell some stocks.There seems to be a view that deep with the offices of the Federal Reserve is a large machine called a Bubble Popper. At anytime, the Fed can wheel it out, aim and fire. Then magically, whatever bubble formed will be popped without damaging anything.

My guess is that Bernanke will be passed with just a few votes over 60, but there was no real danger to his reconfirmation. -

What’s Down the Most?

Posted by Eddy Elfenbein on January 23rd, 2010 at 10:16 pmThe S&P 100 is down -5.25% since Tuesday. Here’s a look at how the 100 stocks have performed.

- Tweets by @EddyElfenbein

-

-

Archives

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His