-

The Fed’s Suez Crisis

Posted by Eddy Elfenbein on September 15th, 2008 at 3:10 pmSomething that struck me about Lehman’s demise is how little power the Federal Reserve really has. Don’t get me wrong, the Fed is darn powerful, but it’s not all-knowing and all-seeing, despite what some folks think. The Fed is powerful because people think it’s powerful.

Analysts hang on every word in a statement or testimony, but in the case of Lehman Brothers (LEH), the Fed really couldn’t do much. Wall Street basically stood up to the Fed and the central bank was exposed. Since Bear was the first, the Fed can open its mouth and get its way. But the Fed can’t make the weaker argument the stronger, and that’s what was needed with Lehman.

I’d say the Lehman story was a combination of too much debt—at one time they were leverage 40-to-1, they didn’t know what they owned, and they refused to listen to any criticism. To top it off, they had horrible luck too. That’s not a good combination.

With Level 3 assets (these are basically assets that can’t be priced easily so we have to trust Lehman for the price), Lehman once claim they their Level 3 stuff was up 9%, even though the market was down by 10%. When people called them on it, Lehman got mad and blamed the shorts. That’s just arrogance. Then they spent something like $22 billion on Archstone? I mean, what the hell? Talk about the wrong price, the wrong industry at the wrong time. Aside from that, it was a great deal!

Einhirn and other shorts said they didn’t know what their stuff was worth and they were undercapitalized. Fuld & Co. just refused to listen. I don’t think they’re crooks at all, they sincerely believed in what they were doing. Until the end, the company was offering assurance to investors.

With Bear and Lehman we often heard about counterparty risk. Well, that theory got shot down with Lehman. I’m going to go on the idea that the reason there wasn’t a deal for Lehman is that no one wanted one. If someone wanted, it would have happened. Novel thinking I know. But it tells us that the Street is hardly concerned about counterparty risk. JPM was concerned about with Bear because it was mostly their risk.

I heard Hank Paulson talk about bringing stability to the markets. Yeah, right. That’s basically like the flea giving orders to the dog. The Fed and the Treasury do not have this thing contained. If the housing market recovers, then the problem goes away. It’s as simple as that. -

Eddy TV

Posted by Eddy Elfenbein on September 15th, 2008 at 2:40 pmI was just on Britain’s SkyTV discussing Lehman’s implosion. If I can find the video, I’ll post it here.

-

91-Day Treasuries

Posted by Eddy Elfenbein on September 15th, 2008 at 11:03 amThe yield on the 91-day Treasury basically got chopped in half today. At one point, the yield got down to 0.67%.10-year Treasury futures had their best one-day gain in nearly 20 years. Now if I can only remember what happened in October 1987.

-

Happy Birthday General Motors!

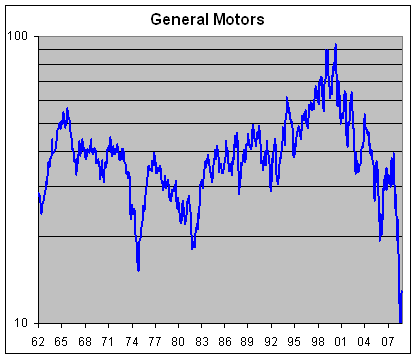

Posted by Eddy Elfenbein on September 15th, 2008 at 9:17 amGM turns 100 years old today.

The stock is currently around $13. Unfortunately, their book value per share is about -$100.

Someone alert Hank Paulson.

-

Yale and Harvard’s Endowments

Posted by Eddy Elfenbein on September 15th, 2008 at 8:32 amFrom June 30, 2007 to June 20, 2008, the S&P 500 lost -13.1%. But Harvard and Yale managed to eek out gains for their endowments. Yale hasn’t announced the figure yet, but it’s expected to be positive in the single digits. Harvard gained 8.6%, which is better than 95% of institutional managers, to reach a total of $36.9 billion. Yale’s endowment now stands at $23 billion.

-

Just a Reminder

Posted by Eddy Elfenbein on September 15th, 2008 at 7:19 amErin Callan from Lehman’s conference call in June:

Lowering gross and net leverage to less than 25 times and less than 12.5 times respectively, both of those numbers are prior to today’s capital raise; reducing our gross assets by approximately $130 billion and our net assets by approximately $60 billion with a large part of the reduction, as I will talk about in detail, coming from less liquid asset categories and also providing significant price visibility for marking the remainder of our inventory.

We significantly reduced our exposure to asset classes such as residential and commercial mortgages, and real estate held for sale of approximately 15% to 20% in each case and acquisition and finance exposure by almost 35%. We also reduced our high yield or non-investment grade debt inventory in the aggregate, which includes our funded acquisition finance position by greater than 20% in the quarter.

I want to be clear at this point that we do not intend to lower our leverage ratios from these levels. From a liquidity perspective, we made great progress growing our cash capital surplus to approximately $15 billion, that’s the surplus, from $7 billion in the first quarter. We grew our liquidity pool to almost $45 billion and that compares with $34 billion at the end of the first quarter. -

Lehman Fills for Chapter 11

Posted by Eddy Elfenbein on September 15th, 2008 at 6:49 amIt’s official. After 158 years of business, Lehman Brothers (LEH) is no more. The company has filed for Chapter 11. I was glad to see the Fed walk away from saving them. A year ago, LEH was going for about $60 a share. The current bid is for 70 cents a share.

In a very exciting Sunday, Bank of America (BAC) announced that it’s buying Merrill Lynch (MER) for $29 a share. Now Morgan (MS) and Goldman (GS) are the last two independent I-banks standing.

That’s not all. There’s talk of a Fed rate cut today (bad idea). Also, AIG (AIG) is in very big trouble and is scrambling to raise money. Oil is also down over $4 and is now below $97. -

Denouement on Wall Street

Posted by Eddy Elfenbein on September 14th, 2008 at 7:08 pmIt’s all falling apart.

Bank of America in Talks to Acquire Merrill Lynch

Lehman Inches Toward Bankruptcy After Potential Buyers Drop Out

The WSJ writes:In a recent note to clients, Oppenheimer analyst Meredith Whitney pointed out that industry revenue was down 63% in the first half of 2008 from the first half of 2007, but expenses were cut by just 10% during that period. Non-compensation expenses, which include buildings and technology, actually rose 25% from the prior year.

Remember when Sunday wasn’t the most newsworthy day on Wall Street.

-

Why Lehman Brothers Is Not Bear Stearns

Posted by Eddy Elfenbein on September 12th, 2008 at 10:05 amFrom the WSJ‘s Market Beat:

Despite similarities in equity and credit markets’ perceptions of Lehman Brothers Holdings this week with views of Bear Stearns in its crisis of confidence during the week ended March 14, there are some glimmers of hope for Lehman in the differences.

The magnitude of Lehman’s drop in the stock market and the widening of the spreads in the market for insuring against events of default certainly recall Bear’s last days. The major difference between Bear and Lehman is continued faith in the latter’s short-term liquidity.

That may explain why the equity-options market on Lehman pivoted Wednesday, and some traders appeared to bet on the firm by buying call options. About 15,700 contracts giving the right to buy Lehman stock for $12.50 a share in October changed hands Wednesday, outweighing open interest. Even as the stock trades down 32% to $4.92, a greater number of calls have traded than puts, suggesting a bullish leaning among option analysts.

While options traders also took both sides on Bear Stearns during its crisis, the bias was more clearly on the bearish put side. “We think Lehman is better off than Bear Stearns in a number of respects,” said Scott Sprinzen, credit analyst at Standard & Poor’s. “Their liquidity is stronger, just given the size of their cash position, and (there is) a lesser dependence on credit-sensitive short-term borrowings.”

Reacting to the liquidity scare on Friday, March 14, Standard & Poor’s cut its rating on Bear Stearns’s short-term and long-term counterparty debt. The difference between the ratings agency’s tone on Bear and that on Lehman is hard to miss:

“Ongoing pressure and anxiety in the markets resulted in significant cash outflows toward the week’s end, leaving Bear with a significantly deteriorated liquidity position at end of business on Thursday,” the agency wrote.

Lehman’s prime-brokerage business is smaller than Bear’s relative to its more diverse portfolio, Mr. Sprinzen noted. And Lehman doesn’t depend on hedge-fund clients’ free credit balances to the same extent. In Bear’s case, the “run on the bank” by prime-brokerage clients was a major contributor to its fall.

On the market for credit default swaps, the spreads on Lehman are not far from those on Bear Stearns when it closed Friday March 14. They have since narrowed from their worst levels of the day of 775 basis points to 745 basis points almost twice as wide as where they were Tuesday, according to Phoenix Partners Group. Still, the swaps have not yet started to trade “up front,” indicating traders would want cash on delivery, as happened with the Bear Stearns. -

Crossing Wall Street Seven Years Ago

Posted by Eddy Elfenbein on September 11th, 2008 at 12:34 am

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His