-

CWS Market Review – November 26, 2024

Posted by Eddy Elfenbein on November 26th, 2024 at 7:09 pm(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Healthcare Stocks Have Lagged the Market for Two Years

The stock market closed at another new all-time high today. The S&P 500 has closed higher for seven days in a row. This was the index’s 52nd new high for this year. There were zero last year. The big caps did the heavy lifting today while the Russell 2000 was down by 0.73%.

Lately, I’ve been asking, what’s going on with healthcare stocks? For years, this was one of the best-performing sectors on Wall Street. Not lately!

Make no mistake, there’s a lot to like about healthcare investing. The industry is heavily supported by the government. That’s a great customer to have. The sector is also helped by demographics. All those Baby Boomers need to have their joints replaced, and not how they used to have their joints replaced.

Investors also like that healthcare performance tends to be steady. There are several healthcare companies who regularly deliver consistent gains. That makes analyzing these stocks much easier. I love many cyclical stocks but those tend to follow boom-and-bust cycles. With healthcare, the lines on the graph are nice and smooth.

But healthcare has been badly lagging! Look at this chart below. I’ve included the S&P 500 Healthcare ETF (XLV, in black) along with the S&P 500 ex Healthcare ETF (SPXV, in blue), meaning everything in the index besides healthcare.

Over the last two years, healthcare stocks have lagged the rest of the market by nearly seven to one. Healthcare stocks currently make up about 11% of the S&P 500. That means that if you combine the two lines above at a nine-to-one ratio (nine black and one blue), that roughly makes up the S&P 500.

Until two years ago, just about any lagging performance from healthcare was a reliable signal to buy. Part of the reason for healthcare’s poor performance can be chalked up to the superior performance of other sectors, particularly large-cap tech.

Some investors think that healthcare stocks were held back by an unfriendly administration in Washington. That could be, but healthcare stocks continued to lag in the days after the election. To be fair, the sector has acted a little better in the last week.

There’s also a far simpler explanation: perhaps healthcare stocks were badly overpriced two years ago. For example, shares of Eli Lilly (LLY) have broken down over the past few months, and it’s still very pricey.

There are currently 62 stocks in the S&P 500 healthcare sector. On our Buy List, we own four of them: Abbott Labs (ABT), Cencora (COR), Stryker (SYK) and Thermo Fisher Scientific (TMO). Over the year, Stryker has been a particularly successful stock for us.

I also suspect that healthcare has done poorly because defensive stocks have been on the outs on Wall Street. That will quickly change in a recession. When things get rough, investors flock to those steady stocks.

I always take notice when an entire sector flounders, especially one that has done so well over the years. That’s a good place to find bargains. For now, if you’re willing to have a little patience, the healthcare sector may be a rich source of long-term winners. I obviously like our four the best. When the cycle turns, I expect to see some very nice gains.

Consumer Confidence Rises to a 16-Month High

Wall Street had some good mixed news today. On the positive front, consumer confidence rose to a 16-month high. This is important to watch. Without confidence, the economy can’t do much. For November, the consumer confidence index increased to 111.7. That’s up from 109.2 for October. Wall Street had been expecting 111.0.

What’s the reason for the optimism? The labor market is still holding up well, although I’d like to see greater wage gains. Also, the outlook for inflation is much better than it was two years ago.

Within the consumer confidence report, there’s also an index of consumer expectations. That index rose to 92.3 which is the highest reading in nearly three years. Earlier this year, the expectations index got very low.

While that’s the good news, the bad news is that the Census Bureau said today that the sales of single-family homes dropped to its lowest level in nearly two years. Clearly, the recent storms impacted these numbers. For October, new home sales fell by 17.3% to 610,000. Wall Street had been expecting 725,000.

Sales in the south fell 28% to 339,000. You have to go back to the early days of Covid to find numbers that bad. Home prices are still going up. Last month, the median price for a new home sold was $437,300.

Tomorrow, the government will update its numbers for Q3 GDP growth. Last month, we got the initial report, and it said that the U.S. economy grew in real annualized terms of 2.8%. That’s not bad. I don’t think the revision will be very different than the original report.

What about Q4? We’re a little over halfway through Q4, and the Atlanta Fed’s GDPNow model estimates that the economy grew at a real, annualized rate of 2.6%. That estimate was recently increased by 0.1%. It will be adjusted again tomorrow. If these numbers are right, then we successfully averted a recession in 2024. That would have surprised a lot of people 18 months ago.

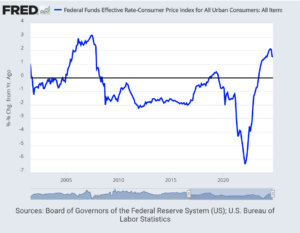

I’ve noticed a growing divergence between what the Federal Reserve expects and what Wall Street expects. The Fed keeps talking tough about interest rates, but market participants don’t buy it. Here’s a look at the Fed funds rate adjusted for inflation:

The Fed meets again in three weeks, and traders think there’s a 63% chance that the Fed will again cut rates by 0.25%. That’s probably too low.

After that, the markets see the Fed cutting rates twice next year, but the Fed sees itself cutting four times next year. When in doubt, I prefer to side with markets over economists. This afternoon, the Fed released the minutes from its most-recent meeting. In it, the Fed confirmed that it’s looking to lower rates but at a gradual pace. As you know, I’m an expert in the bizarre, convoluted dialect known as Fedspeak. I’ll try to translate their foreign language into regular English.

The Fed said that if the current situation continues to improve, then “it would likely be appropriate to move gradually toward a more neutral stance of policy over time.” Note that in the Fed’s mind, it’s not lowering rates but it’s really taking back the rate hikes from 2022-2023. Interestingly, the Fed didn’t say anything about the election or possible tariffs.

The Fed members discussed the “neutral” interest rate. This is the idea that there’s a magic rate of interest and if you go above it, you choke the economy. But if you go below it, then you flood the economy with dollars. The hip econo-name for the neutral rate is R-Star.

The only hitch is that we don’t know where the neutral rate is. We can only guess. Austan Goolsbee, the Chicago Fed President, started calling it “R-Sasquatch.” There’s a general consensus that wherever R-Star is, we’re probably above it.

The minutes said, “Many participants observed that uncertainties concerning the level of the neutral rate of interest complicated the assessment of the degree of restrictiveness of monetary policy and, in their view, made it appropriate to reduce policy restraint gradually.” In other words, they’re as confused as everyone else.

Over the coming few months, I suspect the Fed will gradually reel back its plans for rate cuts for next year.

Milei Looks to Free Argentina’s Economy

Last year, I told you about Javier Milei, the libertarian outsider who was looking to become the president of Argentina. Since then, Milei was elected and he’s upending the political establishment.

He’s also become popular with investors. Bloomberg notes that the Argentina ETF (ARGT) has experienced massive inflows. Last week, ARGT had inflows of $144 million. The ETF has performed well.

I think investors are genuinely shocked that Milei is following through on what he promised. Since Mikei took office, the assets of ARGT have increased sevenfold. The economy in Argentina is getting better and inflation is finally cooling off.

I have to confess that I’m fascinated by Milei and his attempt to fundamentally change his country. It’s like a real-world experiment in macroeconomics.

He’s not done yet. The next big hurdle for Milei is removing capital controls. The fear is that once lifted, money will stampede out of Argentina. That’s happened before when Argentina has moved toward more market-friendly policies. Still, there’s good reason to believe that Milei is an exception.

The capital controls force the currency to be far stronger than it is on the open market. The government tightly controls the exchange rate. Buying foreign currency for savings is limited to $200 per month.

Of all his reforms, ending capital controls could be the most difficult for Milei. The reason is that it’s most likely to cause large-scale disruptions within the economy. Milei probably won’t tackle capital controls for several more months.

Milei is definitely worth following. Argentina is taking a big risk. If he’s right, Milei may offer the blueprint for how other countries can provide shock therapy to their economies.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

-

Morning News: November 26, 2024

Posted by Eddy Elfenbein on November 26th, 2024 at 7:05 amUAE Considers EU-Style Plan to Penalize Polluters for First Time

Italy’s Banco BPM Rebukes UniCredit’s $10.5 Billion Bid

The Bank for Moving On From Communism Questions Rise of Industrial Policy

Trump Plans Tariffs on Mexico, Canada and China That Could Cripple Trade

Trump’s Tariff Threat to Top US Trading Partners Roils Markets

Trump Tests Xi’s Appetite to Play Ball With Early Tariff Threat

After Trump’s Tariff Threat, Is a China Currency War Next?

Bessent Will Have to Fix America’s Finances. Good Luck With That.

An Economic Model That Moves Beyond G.D.P.

The US Gig Economy Is Holding Steady, Not Booming

Why Real Estate Stocks Took a Hit as Developers Cheered Trump

Biden Proposes Medicare, Medicaid Coverage of Obesity Drugs

WorldQuant Stages Shark Tank-Style Contest to Find New Whiz Kids

The Magnificent 7 Are Beginning to Look Average

The World’s Pioneering Tech Cop Is Making Her Exit

The ‘Rocket Docket’ Judge Who Will Decide the Fate of Google’s Ad Technology

China’s Huawei Takes Aim at Apple With Latest Smartphone

Intel Gets $7.9 Billion Chips Award for US Factory Expansion

One of the Hottest Stocks in the Oil Patch is a Defunct 19th-Century Railroad

What Spirit’s Bankruptcy Means for US Holiday Travel

U.S. Airlines Collected More Than $12 Billion From Seat Fees

Best Buy Lowers Full-Year Forecast Amid Turnaround Efforts

Frozen Home-Improvement Spending Could Take Time to Thaw

Target Lost Its Mojo. Hits Like $25 Leggings Are Key to Getting It Back

Dick’s Sporting Lifts Outlook After Strong Back-to-School Season

Sony’s Pursuit of Anime Publisher Holds More Opportunity Than Risk

Be sure to follow me on Twitter.

-

Morning News: November 25, 2024

Posted by Eddy Elfenbein on November 25th, 2024 at 7:05 amG-7 Poised to Boost Pressure on China Over Russian Support

Inside the Frantic Maneuvers That Saved COP29 Talks at a Cost

EU Seeks to Streamline ESG Regulations Amid Growing Backlash

German Businesses Grow More Pessimistic as Geopolitical Pressures Mount

UniCredit Irks Rome with $11 Billion Banco BPM Swoop After German Backlash

The World’s Biggest Debtor Gets a New Manager: Scott Bessent

Dollar, US Yields Fall on Bets Bessent Will Dilute Trump Plans

A Hedge Fund Manager Should Be Able to Run Treasury

Trump Trade Muddles Inflation Outlook in Fed’s Favorite Gauge

Citi Bonuses Buy Time for New Wealth Boss’s Rush to Revamp

Apple’s Cook Joins CEO Summit With China Premier as Economy Sags

Amazon’s Moonshot to Rival NVIDIA in AI Chips

Washington Curtails Intel’s Chip Grant After Company Stumbles

Rocket Lab Signs $23.9M CHIPS Incentives Award to Boost Semiconductor Manufacturing

Google Chrome Sale Could Upend the Browser Market

Adani’s Legal Troubles May Worsen With Risk of Investor Lawsuits

How Trump Could Upend Electric Car Sales

How Southwest Airlines Lost Its Groove

Concrete-Maker Quikrete Strikes $9.2 Billion Deal for Summit Materials

Oneok to Acquire EnLink Midstream in $4.3 Billion Stock Deal

Big Food’s RFK Selloff Looks Overdone, but the Industry Has Other Problems Too

Are Value Meals Worth It for Restaurants?

Macy’s Delays Earnings After Employee Hid Millions in Expenses

Wrangler and Lee Jeans Maker’s Plan for Growth: Sell More to Women

The Charm Bracelet Shop That Keeps Going Viral

Shopping and Shame Share the Shelves in ‘American Bulk’

Without Drama or Banana, Art Auctions Struggle

Be sure to follow me on Twitter.

-

Morning News: November 22, 2024

Posted by Eddy Elfenbein on November 22nd, 2024 at 7:03 amCOP29 Summit Pushes for $250 Billion Deal to Narrow Divisions

Zambia Weighs $900 Million Coal-Power Plan as Drought Hits Hydro

Putin’s Nuclear Threat Is a Magic Trick, but a Dangerous One

Ex-Goldman Banker Turned Lithium CEO Vows to Ride Out Downturn

China’s Plan B to Save the Economy: A Crusade Against Busywork

Japan Approves $141 Billion Stimulus to Boost Economy, Offset Living Costs

ECB’s Lagarde Sees Europe Under Growing Trade Threat

European Farmer Angst Revs Up Again Over Trade Deal and Tax

Inside the Deadliest Job in America

Why Trump Allies Say Immigration Hurts American Workers

While You Do 5-Day RTO I’ll Watch Your Best Workers Quit

What Bondi Might Do as Attorney General

The High Risk, High Reward Trump Market

Dollar Set for Longest Run of Gains in a Year Amid Haven Demand

Goldman Gives the Blockchain Revolution a Home

Crypto Tokens Targeted by US SEC Jump on Gensler’s Planned Exit

Private Equity Financier’s Returns Slump in a $1.2 Trillion Market

US Probes JPMorgan’s Ties to Iranian Oil Kingpin’s Hedge Fund

China’s Hacking Reached Deep Into U.S. Telecoms

How Adani’s Indictment Rocked His Empire and What Comes Next

MicroStrategy’s Infinite Money Glitch Won’t Last

Future-Proofing Biden’s Chips Legacy

Japanese Chip Maker Kioxia Plans Tokyo Market Debut

Jeff Bezos Says Elon Musk’s Claims Are ‘100% Not True’ After the Tesla CEO Reignites Their Feud

Roadrunner Scores Fresh Investment, Eyes Deals

What Happens When US Hospitals Go Big on Nurse Practitioners

McDonald’s Reaches for Choosy Diners With Value Menu Revamp

Amazon’s Black Friday NFL Game Is a Play to Keep You Paying for Prime

Be sure to follow me on Twitter.

-

Morning News: November 21, 2024

Posted by Eddy Elfenbein on November 21st, 2024 at 6:57 amBOJ Will Consider Impact of Weak Yen in Making Price Forecasts, Gov Ueda Says

Europe Is Gaslighting Itself About Its Energy Woes

Turkey Holds Rates, Signals Cuts Coming on Slowing Inflation

French Bond Risk Rises as Budget Tensions Keep Markets on Edge

French Factories Shrug off Trump Tariff Threat as November Mood Lightens

Trump Recruits His Season 2 Cast Straight From the Small Screen

Trump Seeks His Perfect Treasury Candidate as Search Drags On

Trump’s Economic Policy Can’t Be Just Nostalgia

Banks Hoping For Looser Trump Reins Are Too Giddy

The US Stablecoin Startup Fueling a $3 Billion Boom in Africa

Worldline to Raise New Debt After Tumultuous Year Hurts Earnings

Nvidia Says New Chip on Track After Forecast Disappoints

Apple Pay, Other Tech Firms Come Under CFPB Regulatory Oversight

U.S. Proposes Breakup of Google to Fix Search Monopoly

US Watchdog Issues Final Rule to Supervise Big Tech Payments, Digital Wallets

Clear’s Dominance in Airports Could Be Coming to an End

Baidu Revenue Falls Again as Advertising Demand Remains Weak

Alibaba Integrates E-Commerce Operations Into Single Business Group

Adani Charged by US in $250 Million Bribery Case, Shaking India

US Charges Erase $15 Billion From Gautam Adani’s Wealth in Hours

Archegos Founder Bill Hwang Is Sentenced to 18 Years

Brazil Finds Chinese Ally in Its Feud with Elon Musk

What Elon Musk Might Want From America

How Froot Loops Landed at the Center of U.S. Food Politics

Be sure to follow me on Twitter.

-

Morning News: November 20, 2024

Posted by Eddy Elfenbein on November 20th, 2024 at 7:08 amCOP29 Summit Enters Final Stretch With Nations Far Apart on Finance

The Clandestine Oil Shipping Hub Funneling Iranian Crude to China

Asia’s Dark Fleet Hub Highlights Trump’s Oil Sanctions Headache

Trump’s Treasury Search Gains Steam With Fresh Round of Meetings

How Howard Lutnick Could Shake Up Global Trade

Trump’s Cabinet Blitz Is Straight From Orban’s Playbook

Trump and the Triumph of America’s New Elite

Wall Street Is Too Pumped About Trump to Worry About His Policies

American Companies Are Stocking Up to Get Ahead of Trump’s China Tariffs

VCs Look to Secondary Share Sales as The New Exit While M&A Falters

Senator Warren Urges Fed to Keep Wells Fargo Asset Cap

Archegos’ Bill Hwang to Be Sentenced for Massive US Fraud

Why Some Tax Cuts Can Be Better Than Others

To Get the Housing Market Moving, Raise Property Taxes

Miami Condo King Extends Bet on Wealth Boom Spreading up Florida Coast

Resentment is Building as More Workers Feel Stuck

Nvidia Traders Brace for Potential $300 Billion Earnings Move

How Google Spent 15 Years Creating a Culture of Concealment

Iger’s Hero Act Could Leave His Successor Playing the Fool

Comcast to Spin Off Cable Networks, Including MSNBC and CNBC

The Onion’s Bid to Acquire Infowars Has Gotten Messy

Traffic on Bluesky, an X Competitor, Is Up 500% Since the Election. How Will It Handle the Surge?

Target Shares Tumble After Retailer Cuts Profit Outlook

U.S. Military Selects Little-Known Utah Supplier for Drone Program

Hennessy Workers Strike Over Plans to Bottle Cognac in China

The Unusual Power of VW’s Union Boss Is Being Put to the Test

NIO’s Net Loss Widens on Lower Revenue Amid EV Pricing Pressure

Be sure to follow me on Twitter.

-

CWS Market Review – November 19, 2024

Posted by Eddy Elfenbein on November 19th, 2024 at 5:06 pm(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Fifty Years Since the Big Low

We’re soon coming up on a major market anniversary. Two weeks from Friday marks the 50th anniversary of one of the most dramatic lows in Wall Street history. On December 6, 1974, the S&P 500 closed at 65.01. That was the market’s lowest close in the last 60 years.

It’s hard to convey just how low this low was. This was near the low point for post-war American optimism. The stock market had given back all its gains from the previous 12 years. At its low, the market was not far above its peak from 45 years before. In fact, adjusted for inflation, the market was about where it had been in 1929.

Here’s the inflation-adjusted S&P 500 over the last 12 decades:

According to data I saw at Professor Robert Shiller’s data library, the stock market’s P/E ratio in December 1974 was 7.5. It’s more than three times that today. The dividend yield for the entire S&P 500 reached 5.4%.

This was a brutal time for investors. Watergate, Vietnam and inflation dominated the news. In less than two years, the stock market was cut in half. The 1960s saw an explosion in optimism and faith in the future. All of that seemed to unravel by the 1970s.

It’s interesting to note how nostalgic the 1970s was. People were looking backward not forward. One month after the market’s low, President Ford said in his State of the Union Address that the state of the union was “not good.”

Today’s investors assume a constantly rising market that will hit some bumps along the way. That belief hasn’t always been so widespread. Many investors, especially those who had lived during the Great Depression, thought that the stock market was a useless casino that was rigged against them.

As terrible as the headlines were in December 1974, it was a great time to invest. It just took a little courage and a lot of patience. Not including dividends, the stock market has risen more than 90-fold over the last half century. That works out to an annual gain of about 9.5%.

The market works, you just have to wait a little.

Walmart Hits All-Time High

Last Friday, the government released its retail sales report, but today we got an even better report, Walmart’s (WMT) earnings. The retail giant’s earnings are probably a better barometer of how happy consumers are than any government report.

The good news is that Walmart’s customers seem to be pleased. Interestingly, Walmart seems to be doing better with affluent shoppers.

For the quarter, Walmart made 58 cents per share which was a nickel ahead of expectations. Quarterly revenue was $169.59 billion compared with expectations of $167.72 billion. On average, Walmart generates $1.3 million of revenue every minute of every hour of every day for the entire quarter. The stock rose to an all-time high today.

Walmart now expects full-year sales growth of 4.8% to 5.1%. That’s up from the previous forecast of 3.75% to 4.75%. Sales of general merchandise had year-over-year sales growth for the second straight month, but that comes after 11 straight quarters of declines.

The current quarter, which ends in January, is the all-important holiday shopping quarter. For many retailers, this quarter is the biggie. That’s why so many retailers have off-cycle reporting dates. They don’t want to have December and January in different reporting quarters. Last week, I told you about the encouraging report from Home Depot (HD). We’ll soon hear from other big box retailers.

Walmart said it expects sales growth of 3% to 4% for this quarter. Last quarter, Walmart’s e-commerce sales increased by 22%. It’s now 18% of Walmart’s overall business. This was a solid quarter for Walmart and it could be an omen for a good holiday shopping season.

Housing Starts Plunged Last Month

This morning, the Commerce Department said that single-family housing starts fell last month. The drop was most likely due to the recent hurricanes in the South. Still, higher mortgage rates are holding back the housing market.

Even though the Fed is lowering interest rates now, the housing sector is still dealing with the Fed’s aggressive rate hikes of 2022-2023.

Single-family housing starts, which account for the bulk of homebuilding, plunged 6.9% to a seasonally adjusted annual rate of 970,000 units last month, the Commerce Department’s Census Bureau said. Data for September was revised higher to show homebuilding rising to a rate of 1.042 million units from the previously reported pace of 1.027 million units.

Single-family starts dropped 10.2% in the densely populated South, large parts of which were devastated by Helene in late September. Milton struck Florida in October. Ground-breaking on single-family housing projects plummeted 28.7% in the Northeast, but increased 4.6% in the Midwest and the West.

Single-family homebuilding slipped 0.5% from a year ago.

Starts for multi-family housing jumped 9.8% to a pace of 326,000 units. Overall housing starts dropped 3.1% to a rate of 1.311 million units. That was below Wall Street’s forecast. What’s happening is that many homeowners already locked in low rates on their mortgages so they’re reluctant to move now.

The yield on the 10-year Treasury, which tends to track mortgage rates, recently touched a five-month high. Longer yields have moved against the Fed’s policy of lower short-term rates.

This is a good reminder that it takes time for the Fed’s policies to impact the real economy. Traders currently think there’s a 60% chance that the Fed will cut again next month. That’s much lower than I expected. Perhaps Wall Street thinks there will soon be good reasons for the Fed to pause.

Get Ready for Nvidia’s Earnings

One more item. Nvidia (NVDA) is set to report earnings tomorrow. Get ready because this report could move the entire market. I confess, I have no idea what to expect, and neither does anyone else. The company now has a market value of roughly $3.6 trillion.

A year ago, Nvidia made 40 cents per share. The consensus this time is for earnings of 75 cents per share. Sales are expected to increase from $18.12 billion to $33.14 billion.

We can look at the action in the options market and see what to expect. For example, options traders expect shares of NVDA to swing by 8.5% after the earnings report comes out. That’s up or down and that average swing is roughly $300 billion. That amount is far larger than the vast majority of companies in the S&P 500.

NVDA has had several impressive after-earnings rallies, but that didn’t happen last time. Reuters quoted Matt Amberson who said that of the last 12 quarterly earnings reports, five post-earnings moves have been outside what has been expected by the market. “Of those, all have seen the stock price go higher, Amberson said.”

Nvidia’s CEO recently said that demand for the company’s next-generation AI chip Blackwell is “insane.” What would people in 1974 have said?

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

-

Morning News: November 19, 2024

Posted by Eddy Elfenbein on November 19th, 2024 at 7:07 amOil Glut Set to Thwart Trump’s Call to ‘Frack, Frack, Frack’

German Defense Chief Sees Baltic Cable Breaches as Sabotage

Why US Will Let Ukraine Strike Inside Russia With American Missiles

Gold Is at the Mercy of Trump, China and King Dollar

Things Are Quiet in Consumer Credit. Too Quiet.

Trump’s Impossible Task: Delivering for the Working Class and Billionaires

Rethinking the Worst-Case Fears About Trump Tariffs

Wall Street’s Top Cop Plans to Exit Before Trump Takes Power

Five Ways R.F.K. Jr. Could Undermine Lifesaving Childhood Vaccines

RFK Jr. Would Put the Economy at Risk, Too

Companies With Immigrant Workforces Are Preparing for Raids

While You Were Voting, Corporate America Made Bank

Goldman Sachs Chairman Expects Deals to Pick Up in 2025

Morgan Stanley Courts Employees of Near-IPO Companies for Wealth Management

China’s Chip Advances Stall as US Curbs Hit Huawei AI Product

When IR Met AI: How the Technology Is Shaping Earnings-Day Prep

Nvidia’s Options Primed for $300-Billion Price Swing After Earnings

Google’s Anthropic AI Deal Cleared by UK Antitrust Agency

DOJ Will Push Google to Sell Chrome to Break Search Monopoly

Amcor to Acquire Berry Global in $8.4 Billion Packaging Deal

The Future of Abortion Rights Could Be Decided by Accident

Lowe’s Lifts Sales Forecast on Improving Housing Spend

Robots Struggle to Match Warehouse Workers on ‘Really Hard’ Jobs

Walmart Raises Outlook on Strong Spending From Value-Seekers

Shoppers Are Ditching Classic Brands They Once Loved

Blackstone Strikes Deal for Jersey Mike’s Subs

Swiss Watch Exports Fall Again Amid Plummeting Demand in China

Be sure to follow me on Twitter.

-

Morning News: November 18, 2024

Posted by Eddy Elfenbein on November 18th, 2024 at 7:04 amWhy Oil Companies Are Walking Back From Green Energy

Why Big Oil Doesn’t Mind Big Regulation

A Global Fund for Climate Disasters Is Taking Shape in Trump’s Shadow

Turkmenistan’s Gas Company Will Enlist Experts to Combat Methane Leaks

For Decades, Installing E.V. Chargers Didn’t Pay Off for Retailers. Now It Does.

Indian Students Rush to US Colleges, Driving Attendance Record

Moody’s Cuts Bangladesh Further Into Junk on Political Risks

Greek Banks Looking at Deals Abroad After Painful Restructurings

Eurozone Trade Surplus Rises on Jump in Exports to U.S.

Powell May Be Waiting Until 2026 for Housing Inflation to Cool

Trump Treasury Cabinet Pick in Flux as Jockeying Slows Selection

Trump Picks Brendan Carr to Lead F.C.C.

Four Priorities for Trump’s Top Telecom Regulator

Crypto Prediction Markets Have a Cloudy Future

HSBC Managers Are Competing to Keep Their Jobs in CEO’s Revamp

Bain Capital Raises $5.7 Billion for Global Special Situations

Wall Street Bankers Spot a Fat Payday in $1 Trillion AI Hysteria

Manufacturing Was Set to Rebound. Then Trump Happened.

Tim Berners-Lee Wants the Internet Back

Xiaomi Profit Beats on Robust Sales Across Segments

Why Tech Billionaires Love the Author of Jurassic Park

Ben & Jerry’s Vs. Unilever Is the End of Corporate Do-Gooderism

Spirit Air Files Bankruptcy Following Failed JetBlue Tie-Up

Auto Industry Braces for Whiplash as Trump Takes Power

Novo Nordisk Launches Wegovy in China With Prices Well Below US

Substack’s Great, Big, Messy Political Experiment

Paramount Takes Promotional Stunt to New Level for ‘Gladiator II’

Be sure to follow me on Twitter.

-

Morning News: November 15, 2024

Posted by Eddy Elfenbein on November 15th, 2024 at 7:03 amRussia Envoy Backs Paris Climate Deal, Hopes Trump Will Too

Oil Set for Weekly Loss Amid Demand Worries, Rate-Cut Slowdown Prospects

World Fears a Wider Trade War. Malaysia Sees an Opportunity.

China Stimulus Boosts Domestic Consumption as Trump Tariffs Loom

Eurozone Economy to Grow Less Strongly as Trade Spat Brews, EU Says

Trump US Election Win Comes With a Catch for Israel’s Far-Right

America’s Homes Are Piggy Banks That Few People Can Afford to Raid

CEOs Brace for the Chaos of Another Four Years of Trump

Boston Fed President Says December Rate Cut Isn’t a ‘Done Deal’

‘Flood of Money’ Chases US Banking’s Hottest New Trade

Traders Chase Post-Election Stock Gains in US Options Market

Investors Circle the Trump Trade’s Global Market Victims

Betting on Tesla Helped Ron Baron Beat the Index. Now He’s Getting a Trump Bump

Pay Close Attention to Your Credit Card Balance Under Trump 2.0

Musk’s New Job For Trump Already Exists

How Musk’s DOGE Can Actually Do Some Good

Trump’s Anti-Regulation Pitch Is Exactly What the AI Industry Wants to Hear

Musk Escalates Altman Legal Feud, Casting OpenAI as Monopolist

Super Micro’s Looming Nasdaq Deadline Stokes Delisting Fears

Biden Cements TSMC Grant Before Trump Takes Over

Hokkaido Electric Sees Power Demand Surge With Data Center Boom

Disney Targets $1 Billion in Streaming Profit in New Fiscal Year

DoorDash Wants to Give You a Ride and a TV Show With Dinner

Startups Turn to Ponds to Find the Next Climate-Fighting Superfood

The Onion Wins Bid to Buy Infowars, Alex Jones’s Site, Out of Bankruptcy

Returns Are a Headache. More Retailers Are Saying, Just ‘Keep It.’

Human in Bear Suit Was Used to Defraud Insurance Companies, Officials Say

Be sure to follow me on Twitter.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His