-

The Black Swan

Posted by Eddy Elfenbein on February 6th, 2008 at 12:55 pmI finally got around to reading The Black Swan: The Impact of the Highly Improbable by Nassim Nicholas Taleb. It’s fascinating, albeit, infuriating book.

In it, Taleb critics the idea that financial markets follow the classic bell curve. As a result, much of understanding about markets—everything from risk control to options values—is completely wrong. While this is an intriguing idea, and I believe he’s correct, The Black Swan is largely unreadable.

Taleb’s writing isn’t merely bad, it’s downright offensive. The entire book is written in a smug and obnoxious style filled with pointless asides. He’s argument is barely coherent and nearly every page includes parentheticals or scare quotes that simply aren’t needed. Taleb, like all writers, ought to adhere to Mark Twain’s dictum: eschew surplusage

Taleb could have written the book in 50 pages, tops. He also could have spared us his opinion on everything I don’t care about. Taleb constantly reminds us that he’s an aesthete, which you would think would lead him to be a better writer.

He’s one of the people, and I’m sure you’ve met someone like this, who needs to call everything by its less-well-known variant. Do you remember the guy in college who did one semester abroad and came back suddenly using “lift” and “petrol”? That’s Taleb. Now imagine 300 pages of it. Muslims are “Moslems”; he’s “Levantine” not Lebanese. First and second become “primo” and “secondo” (I had to Google it).Strangely, even Daniel Kahneman is routinely called “Danny.”

Leaving the writing aside, the subject is very important. The question that I think it most interesting is, how do we quantify the risk of outliers—meaning, very rare events. Or, due to their nature, is that impossible? Interestingly, we’re been watching a Black Swan event unfold (fly out?) before us in real time. The subprime crisis has exposed many financial firms to far more risk than they believed.

All the major investment banks report their “value at risk,” or if you’re a cool kid, their VAR. They all use different equations to reach their VAR but basically, it designed to measure how much money is at risk with a 95% confidence level. But this is where some problems are coming. For example, Merrill Lynch’s VAR indicated that it couldn’t be expected to lose more than $5.8 billion in a single quarter. Well, they lost $8.4 billion.

I don’t have any answers to the issues Taleb raises, but it’s not an academic point. The worst part of the subprime debacle is that we don’t know what we don’t know. The odd thing about Black Swans is that even if we suspect their existence, then they no longer exist. -

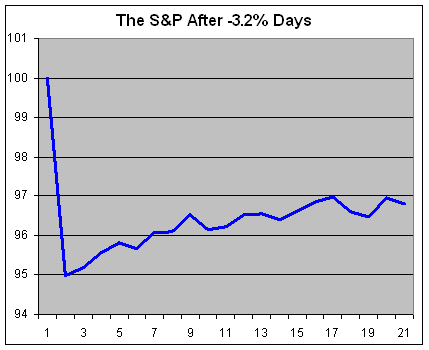

How the Market Behaves After Big Down Days

Posted by Eddy Elfenbein on February 6th, 2008 at 10:56 amI once remember hearing that the market tends to retrace one-third of its previous days trend after a large move. I decided to put that theory to the test.

Yesterday, the S&P 500 lost 3.2%. This was the 38th time the index has done that since 1950. Here’s an average of how those 37 previous sell-offs played out.

The average loss for the sell-off is 5.01%. After that, nearly every day is an up day. By the ninth day, the S&P 500 is down 3.48%, which is indeed, a retracement of about one-third.

The market still trends higher to the 17th day where it’s down just 3.01%, or about a 40% retracement. At that point, the linger effects of the sell-off seem to dissolve. -

Strange Market Fact of the Day

Posted by Eddy Elfenbein on February 5th, 2008 at 1:49 pmNever underestimate the power of momentum on Wall Street. Since 1950, every penny of gains in the S&P 500 has come on days following 0.64% up moves. That happens roughly once every five market days.

In other words, if you invested only on days following 0.64% up days, and sat in cash the other 81% of the time, you would have easily beaten the market.

Warning: I’m not advocating such a strategy. That’s your classic sinkhole of back-testing. I merely want to show you how trend sensitive Wall Street can be. -

Nicholas Financial Reports Earnings

Posted by Eddy Elfenbein on February 5th, 2008 at 11:34 amNicholas Financial (NICK) reported earnings today. For the December quarter, the company’s third, NICK earned 22 cents a share which is a big drop from the 27 cents a share it made in last year’s third quarter. The big difference was the 106% rise in “provision for credit losses.” That’s about an increase of 12 cents a share.

If these results are as bad as it gets for NICK, consider that the stock is going for 32 times this past quarter’s earnings. -

The Myths of Innovation

Posted by Eddy Elfenbein on February 5th, 2008 at 10:07 amHere’s an interesting article from the Sunday New York Times. It questions the idea that innovation comes from a sudden burst—a Eureka moment—but instead is the result of gradually building smaller insights.

“The most useful way to think of epiphany is as an occasional bonus of working on tough problems,” explains Scott Berkun in his 2007 book, “The Myths of Innovation.” “Most innovations come without epiphanies, and when powerful moments do happen, little knowledge is granted for how to find the next one. To focus on the magic moments is to miss the point. The goal isn’t the magic moment: it’s the end result of a useful innovation.”

Everything results from accretion, Mr. Berkun says: “I didn’t invent the English language. I have to use a language that someone else created in order to talk to you. So the process by which something is created is always incremental. It always involves using stuff that other people have made.” -

Politics and the Markets

Posted by Eddy Elfenbein on February 5th, 2008 at 9:49 amRichard Nixon was once asked what he would do if he weren’t president. He said that he’d probably be on Wall Street buying stocks. One old-time Wall Streeter was asked what he thought of that. He said that if Nixon weren’t president, he too would be buying stocks.

Today is Super Duper Tuesday. There are about a million primaries going on in several different states. I don’t have much to say about politics, but I would strongly caution anyone from drawing investing conclusions from today’s results.

People love to talk politics, and people love to talk stocks, but the two really don’t have that much to do with each other. Policy, of course, can have a major impact on stocks but when it does, it’s the kind of policy that’s barely a part of the permanent Republican-Democrat debate. Sarbanes-Oxley, for example, passed the Senate 99-0, and the House 423-3 (Ron Paul being one of the three).

Stocks have done well under Democratic and Republican presidents. Stocks have also crashed under Democratic and Republican presidents. The closest thing to a constant I can find is that the stock market really doesn’t like Quaker presidents (Nixon and Hoover), but the sample size is kinda small.

My advice is to ignore any chatter you may hear that so-and-so is good or bad for the market. The assumption is that politicians are like players on a football field, and the stock market is the score. I think it’s exactly the opposite. What’s really interesting isn’t how the market responds to politicians, it’s how politicians respond to the markets.

The stock market is running unopposed this year. -

Will Ferrell on CNBC

Posted by Eddy Elfenbein on February 4th, 2008 at 1:46 pmThis is a bit old, but here’s Will Ferrell causing havoc on Power Lunch.

-

Profile of Steve Schwarzman

Posted by Eddy Elfenbein on February 4th, 2008 at 12:00 pmThis must be the season for gigantic profiles of financial bigwigs. Now, the New Yorker‘s James B. Grant takes 10,000 words to look at Steve Schwarzman. Here’s a teeny, tiny bit:

There were no dance performances on Yale’s all-male campus, but the New England women’s colleges were filled with aspiring dancers. It occurred to Schwarzman that with these women he could stage a dance performance, and charge admission. “Put attractive women in tights and you’d sell out,” he said. He got in touch with Walter Terry, the dance critic for Saturday Review, and persuaded him to attend. He scheduled the performance for a weeknight, when nothing else was competing for students’ attention. The event sold out, and Terry wrote about it in Saturday Review, in the issue of March 29, 1969. In the article, Schwarzman, asked about his future, said, “I can’t afford the arts right now. That takes money. So I’m going to a school of business administration.”

Schwarzman had majored in Intensive Culture and Behavior, an interdisciplinary subject, and hadn’t taken a single economics or accounting course. Law school or business school seemed a logical next step, but he had little sense of where either would lead. During his senior year, he had sent a letter to W. Averell Harriman, the wartime Ambassador to Russia and former governor of New York, who was serving as the President’s representative at the Paris peace talks. “There weren’t that many people in that era to admire, and I wrote him a letter saying I admired him and wanted to meet him,” Schwarzman recalled. Harriman, a fellow Skull and Bones man, invited him to lunch at his town house, on the Upper East Side, occasionally interrupting their talk to take calls from Cyrus Vance, in Paris. According to Schwarzman, Harriman asked him, “Young man, are you independently wealthy?”

“No, sir, I’m not.”

“Well, I am the son of a very rich man, which has made an enormous difference—that’s the reason you’re seeing me. If you have any interest in the political world, I advise you to become independently wealthy yourself.”You gotta admit, that’s good advice.

-

Google Attacks Microsoft/Yahoo Deal

Posted by Eddy Elfenbein on February 4th, 2008 at 9:26 amThis is a bit pathetic. Google is complaining about the potential merger between Yahoo and Microsoft.

At Google’s blog, the company’s lawyer asks, “Could Microsoft now attempt to exert the same sort of inappropriate and illegal influence over the Internet that it did with the PC?”

That question makes little sense. He’s implying a relationship between the deal and Microsoft’s future attempts at breaking the law. By that logic, how do we know that this deal won’t lead to Microsoft selling crack? If Microsoft wants to overpay for Yahoo, that’s their business. -

Mstislav Rostropovich

Posted by Eddy Elfenbein on February 1st, 2008 at 4:42 pm

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His