-

CWS Market Review – March 5, 2021

Posted by Eddy Elfenbein on March 5th, 2021 at 7:08 am“There seems to be an unwritten rule on Wall Street: If you don’t understand it, then put your life savings into it.” – Peter Lynch

Some jitters have come to Wall Street. On Thursday, the S&P 500 closed at its lowest level in more than a month. For the first time in six months, the index had back-to-back losses of more than 1%. Of course, the losses may seem heavier than they were because the rally hasn’t had much pushback. That is, until now.

Interestingly, the S&P 500 closed below its 50-day moving average on Thursday (the blue line on the chart below). That’s an interesting signal to watch. With one minor exception, the S&P 500 had stayed above its 50-DMA since early November. The index came within a hair of closing below its 50-DMA on Wednesday and again last Friday. But in both cases, the index rallied off the 50-DMA. Not so this time.

All told, the S&P 500 is down a little over 4% from its high, but this is the first time in a long time that the bears appear to have the upper hand. So what’s going on? It seems that higher bond yields are finally making stocks a little nervous. Fed Chairman Jerome Powell backed that up by saying that some inflation could be on its way.

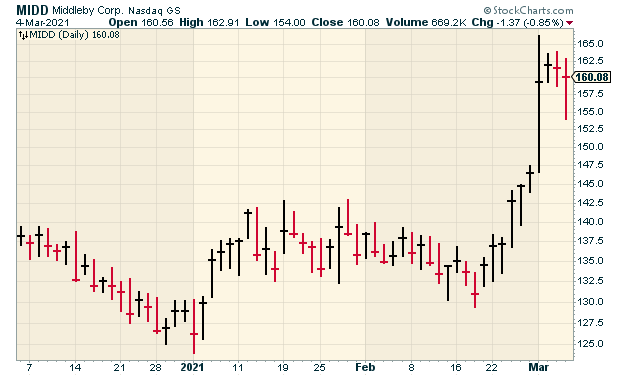

As for us, we had our final three earnings reports this week. The report from Ross Stores wasn’t so hot, but there’s reason for optimism. The deep-discounter reinstated its dividend. We had very good news from Miller Industries and Middleby. At one point on Monday, Middleby was up over 13% for us. It’s now our #1 performing stock this year with a gain of 24.2%. Miller is looking good as well. I’ll have all the details in just a bit. But first, let’s look at what’s making folks so nervous.

Expect Some Higher Inflation

So is the bull taking a little nap, or are we at the start of something worse? Honestly, we can’t say either way just yet. In last week’s issue, I laid out the case for optimism, but that’s for the overall economy. The market can do poorly in a good economy (and vice versa).

In fact, we had more good news for the economy this week. On Monday, the ISM Manufacturing Index tied for its highest level in 17 years. The concern for the market is that long-term interest rates are creeping higher. On Thursday, the yield on the 10-year Treasury bond closed above 1.5%. That hasn’t happened in over a year.

Of course, these bond yields are far from high, but they’re higher than they were. As a very general rule, the bond market tends to lead the stock market by a few months. It’s strange that the stock market would be concerned by a bond yielding just 1.5%.

This week, Fed Chairman Jerome Powell joined the higher-yields club when he said that more inflation could be on its way. Powell said, “We expect that as the economy reopens and hopefully picks up, we will see inflation move up through base effects.” For a central banker, saying that qualifies as a freakout. As soon as Powell said that, stocks started to fall.

Of course, a lot of this is because things are either getting back to normal or are soon expected to be getting back to normal. When the economy is held back, then released, you’re going to see some inflation. In 1946, the inflation rate was 8.3%. That was followed in 1947 by an inflation rate of 14.4%. I’m not expecting numbers like that, but some higher inflation is only natural. Let’s also remember that a $1.9 trillion stimulus is also on the way.

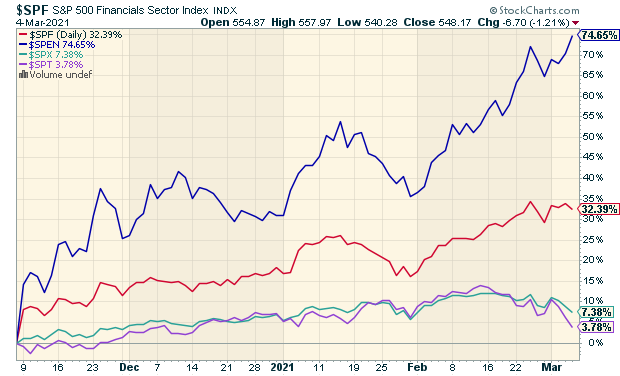

Here’s a telling chart that explains what’s happening. The blue line is the energy sector, and the red line is financials. Both of them have been beating the pants off the overall market. These are precisely the cyclical and low-quality stocks that I’ve talked about in previous issues.

The green line at the bottom is the S&P 500. What’s interesting is that the purple line is the tech sector. That’s pretty much moving along with the S&P 500. The reason I call this to attention is that in normal times, investors prefer tech because it doesn’t hug the broader indexes.

Investing in tech is a cheap and easy way to diversify, but now tech is just like everybody else. Nowadays, the different stuff is the energy and financials: “Hey, let’s diversify. Let’s buy Chevron and a bank!” As odd as it sounds, that’s what’s happening.

Don’t let the jitters scare you. The stocks on the Buy List are sound no matter what the market throws our way. Make sure you have a diversified portfolio of high-quality stocks. Now let’s look at this week’s earnings news.

Earnings from Middleby, Ross Stores and Miller Industries

We had our final three earnings reports this week. Here’s the complete Earnings Calendar.

Let’s start with Middleby (MIDD), as the company had an outstanding earnings report on Monday. For its fiscal Q4, Middleby earned $1.62 per share. That easily beat expectations of $1.41 per share. As I look at the numbers, this was a very good quarter for Middleby.

A year ago, the stock got demolished during the market selloff. In fact, MIDD underperformed an already terrible market. The company makes industrial-sized kitchen equipment for hotels and restaurants. The lockdowns were very tough on MIDD’s clients. Still, this is a good example of our buy-and-hold strategy working in our favor. As MIDD plunged, I’m sure a lot of investors cut and ran. From the low point, shares of MIDD have quadrupled.

Adjusting for exchange rates, quarterly sales fell 9.3% in Q4. That’s not much of a surprise. Commercial food service was down 18.9%. The good news is that business is coming back. The company’s backlog now stands at a record $522.7 million. I really like how Middleby has managed itself over the past year. Operating cash flow increased to $208.6 million, compared with $147.7 million for last year’s Q4. Also, MIDD’s EBITDA margin was 20.3%. That’s quite good.

The shares gapped up strongly on Monday. At one point, MIDD was up 13.6% on the day. That jump came after the stock rallied six days in a row going into the earnings report. The stock rallied again this Tuesday, for a combined eight-day winning streak.

Middleby is now our top performer on the year, with a gain of more than 24%. This week, I’m raising our Buy Below to $170 per share.

After the close on Tuesday, Ross Stores (ROST) reported fiscal Q4 earnings of 67 cents per share. That was a pretty weak result. Wall Street had been expecting earnings of $1 per share. This was for the 13 weeks ending January 30, so it included the crucial holiday-selling months of November, December and January. For many retailers, the Christmas season defines much of the fiscal year.

For the quarter, Ross had sales of $4.2 billion. Same-store sales fell 6%. For the year, Ross made 78 cents per share. Total sales were $12.5 billion.

One of the problems is that Ross has many stores in California, and that state has more stringent lockdown measures. The silver lining is that those stores have greater room to bounce back as the economy gets back to normal.

CEO Barbara Rentler said that Q4 sales exceeded their expectations. Q4 operating margin declined to 9.5%.

Now for some good news. Ross is reinstating its quarterly dividend of 28.5 cents per share. Last year, Ross raised its quarterly dividend by 12%, from 25.5 cents to 28.5 cents per share. After the payment last March, the dividend was suspended. Now it’s back.

For Q1 guidance:

Ms. Rentler continued, “Comparable store sales for the 13 weeks ending May 1, 2021 are projected to be down 1% to down 5% compared to the 13 weeks ended May 4, 2019. Earnings per share for the 2021 first quarter are forecast to be $0.74 to $0.86, reflecting the deleveraging effect from the projected decline in same store sales, increased supply chain costs, higher wages, and ongoing COVID-related expenses.”

Wall Street had been expecting 89 cents per share for Q1.

Ms. Rentler said that they plan to open 60 new locations this year (about 40 Ross Dress for Less and 20 dd’s Discounts.) She also said that Ross is well positioned to gain market share, since so many retailers have gone under during the lockdowns.

Shares of Ross fell 5.6% on Wednesday. Ross Stores remains a buy up to $120 per share.

On Wednesday, Miller Industries (MLR) became our final Q4 earnings report. I had been waiting for this one. All things considered, it was a decent quarter. Net sales fell 12.2% to 178.3 million, but net income increased by two cents to $1.05 per share. That’s better than I had been expecting. Miller isn’t followed by any analysts.

This was a very tough year for Miller, but Q4 wasn’t nearly as bad as previous quarters. For the year, Miller made $2.62 per share, which was a big drop from $3.43 per share in 2019. Net sales fell 20.4% to $651.3 million.

Jeffrey I. Badgley, the Co-CEO, said:

In the first half of the first quarter of 2021, we experienced significant delays in deliveries to our distributors caused by changes we made to our legacy business processes during the implementation of our new enterprise software system. During the same period, we also experienced significant supply chain disruptions due primarily to continued impacts from COVID-19, and extreme weather conditions across parts of the U.S. and tightening availability of freight trucks caused delays in delivering products to our facilities as well as to our customers. These factors caused substantial downward pressures on our revenues, margins and earnings during the first half of the first quarter of 2021. The business process improvements critical to developing our new software system are now essentially operational, allowing our delivery schedule to return to meeting current customer demand. The supply chain issues have now been greatly reduced but could recur. Based on our strong backlog and the current status of our process improvements, we believe we have the opportunity to substantially improve our operating results in 2021 beyond the first quarter.

On Thursday, shares of Miller touched a new 52-week high. We have a gain this year of 9%. I’m raising our Buy Below on Miller to $45 per share.

Buy List Updates

After this week, we’re basically done with earnings for the next seven weeks. The lone exception will be FactSet (FDS). This week, the company announced that it will report its fiscal-Q2 results on March 30. The company expects earnings this year to range between $10.75 and $11.15 per share. This week, I’m lowering FactSet’s Buy Below to $340 per share.

I’m also lowering our Buy Below on Check Point Software (CHKP). I probably should have done this after the last earnings report. The earnings beat expectations, but guidance was soft. For Q1, Check Point sees earnings ranging between $1.45 and $1.55 per share. Check Point is a buy up to $120 per share.

That’s all for now. There’s not a whole lot on tap for next week. The February CPI report is due out on Wednesday. Even though inflation expectations have risen, there hasn’t been much evidence of higher inflation. At least, not yet. Also on Wednesday, the government will update on the federal budget. On Thursday, we’ll get another jobless-claims report. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: March 5, 2021

Posted by Eddy Elfenbein on March 5th, 2021 at 7:01 amA Confident China Promises Robust Growth and a Hard Line on Hong Kong

China Pledges to Build ‘Polar Silk Road’ Over 2021-2025

Libor Moves to Its ‘Final Chapter’ as U.K. Sets End Dates

Bond Fires Smoulder, Shares Drop Ahead of U.S. Jobs Data

A Leading Critic of Big Tech Is Expected to Join the White House

Bitcoin Storm Brewing Over Trump’s Anti-Money Laundering Push

Wealth Managers Frustrated Over Bitcoin, Anxious for Piece of the Action

OPEC And Allies Keep Oil Production Steady As Saudi Arabia Urges ‘Caution’

Texas Grid Operator Made $16 Billion Price Error During Winter Storm, Watchdog Says

When Amazon Raises Wages, Local Companies Follow Suit

BUZZ, the ETF of Social-Media Darlings, Drops in Trading Debut

Costco Sales Rise 15% in Latest Quarter

Howard Lindzon: SPAC Week…SPACs Are Here To Stay This Time…BUT….

Michael Batnick: I’m All In On Audio & It’s Not Different This Time

Ben Carlson: Investments as a Status Symbol

Be sure to follow me on Twitter.

-

The S&P 500 May Close Below Its 50-DMA

Posted by Eddy Elfenbein on March 4th, 2021 at 12:51 pmYesterday the stock market closed right at its 50-day moving average. This is one of those silly rules that actually is important. I would guess that if you told someone unfamiliar with the stock market that the average of the previous 50 days plays an important part in the market, they might not believe you.

Yesterday was actually the second recent close near the 50-DMA. Also this morning, the initial jobless claims report came in at 745,000. Expectations were for 750,000. We’re close to our lowest level in nearly a year. We’re coming up on the one-year anniversary when everything fell apart. Last March, the Dow Jones had its 4th and 11th best days in history and its 2nd, 5th and 13th worst days in history.

Miller Industries (MLR) reported its earnings yesterday. This morning, the stock popped to $44.06, which is a new high.

-

Morning News: March 4, 2021

Posted by Eddy Elfenbein on March 4th, 2021 at 7:07 amAsia’s Ultra-Rich Are Piling Investments Into Blank-Check Firms

Bond Scares Linger, Investors Look to Powell

Investors Are Focused on Treasurys. Here’s What the Fed Could Do.

Jittery Stocks, Jumpy Bonds: Why Investors Are Troubled by Signs of Growth

New Biden Economic Hires Point Toward Infrastructure, Manufacturing Emphasis

Texas Farmers Tally Up the Damage From a Winter Storm ‘Massacre’

Robinhood Faces a Feared Regulator With Even More Tools Than the SEC

Inside Pfizer’s Fast, Fraught, and Lucrative Vaccine Distribution

Disney Shuttering At Least 20% of Disney Stores as It Shifts Focus to e-Commerce

As Online Shopping Surged, Amazon Planned Its New York Takeover

Amazon in Talks to Carry Many NFL Games Exclusively on Prime Video

Private Equity Firm Acquires Michaels in $5 Billion Deal

Joshua Brown: They Will Flood the Market with Collectibles & The New New Bull Market

Howard Lindzon: SPAC Week Continues…Bigger, Louder, Faster…The SPAC Locomotive Continues…For Now

Michael Batnick: The Stock Market Is Usually Right

Be sure to follow me on Twitter.

-

Miller Industries Earned $1.05 per Share

Posted by Eddy Elfenbein on March 3rd, 2021 at 4:39 pmBetter late than never. After the closing bell, Miller Industries (MLR) became our final Q4 earnings report. For the fourth quarter, net sales fell 12.2% to 178.3 million, but net income increased by two cents to $1.05 per share. That’s better than I had been expecting. Miller isn’t followed by any analysts.

This was a very tough year for Miller but Q4 wasn’t nearly as bad as previous quarters. For the year, Miller made $2.62 per share which was a big drop from $3.43 per share in 2019. Net sales fell 20.4% to $651.3 million.

Jeffrey I. Badgley, Co-Chief Executive Officer of the Company stated, “During the fourth quarter of 2020, we experienced steady improvement and I am encouraged by the underlying strength of our business and the resilience of our customer demand despite the ongoing impact of the COVID-19 pandemic.”

Mr. Badgley continued, “While we were encouraged to finish the year with such strong operating results, the start to the first quarter of 2021 has not been without its challenges. As we discussed in greater detail in our Form 10-K filing, in the first half of the first quarter of 2021, we experienced significant delays in deliveries to our distributors caused by changes we made to our legacy business processes during the implementation of our new enterprise software system. During the same period, we also experienced significant supply chain disruptions due primarily to continued impacts from COVID-19, and extreme weather conditions across parts of the U.S. and tightening availability of freight trucks caused delays in delivering products to our facilities as well as to our customers. These factors caused substantial downward pressures on our revenues, margins and earnings during the first half of the first quarter of 2021. The business process improvements critical to developing our new software system are now essentially operational, allowing our delivery schedule to return to meeting current customer demand. The supply chain issues have now been greatly reduced but could recur. Based on our strong backlog and the current status of our process improvements, we believe we have the opportunity to substantially improve our operating results in 2021 beyond the first quarter.

Overall, I am extremely proud of our employees’ continued commitment to providing industry leading customer service and I am confident that we will continue to capitalize on all future growth opportunities despite the headwinds we experienced in the first quarter of 2021.”

-

The Stock Market Is *VERY* Concentrated

Posted by Eddy Elfenbein on March 3rd, 2021 at 2:35 pmOne of the important facts about the stock market that I try to stress to new investors is just how big the mega-cap stocks are. These are gigantic companies, even compared with other fairly large stocks.

Apple has a market value in excess of $2 trillion. Google, Microsoft and Amazon are in the $1 trillion club.

The total market value of the S&P 500 is about $32 trillion. That means that those four stocks make up about 20% of the index.

Here’s a good chart that shows how concentrated the stock market is. This chart shows the 50 largest stocks in the S&P 500 (red line) along with the S&P 500 (blue line). In other words, the other 90% of the index adds a little diversification, but not much.

A few years ago, I tried to show how you could build a decent index fund with just eight stocks. (Mimicking the index is the easy part, but it’s a classic case of fat tails. That means that one big outlier can completely wreck your index tracking.)

One of the broad-based indexes is the Russell 3000. They further sub divide that into the 1,000 largest for the Russell 1000. The other 2,000 stocks make up the Russell 2000 which is often a proxy for the small-cap market. My point is that companies in the Russell 2000 are still pretty big. Recently, Apple’s market value surpassed the market value of the entire Russell 2000.

You can build a portfolio with only a few stocks that closely follows the indexes. You can also build a portfolio with hundreds of stocks that moves entirely differently than the market.

-

February ADP = +117,000

Posted by Eddy Elfenbein on March 3rd, 2021 at 12:13 pmThis is jobs week, and there’s a standard order to it.

On Wednesday, ADP releases its report on private payrolls.

Then on Thursday, the government releases its weekly report on jobless claims.

Finally, on Friday, the government releases the big monthly jobs report.

This morning, we got the ADP payrolls report and it indicated that the U.S. economy created 117,000 net new private sector jobs last month. That was well below expectations of 225,000. I’ll add that the ADP report doesn’t always line up well with the government’s numbers.

For this Friday’s government report, Wall Street expects non-farm payrolls to rise by 210,000.

-

Q4 2020 Earnings Calendar

Posted by Eddy Elfenbein on March 3rd, 2021 at 12:03 pmEarnings season wraps up with 22 of our 25 Buy List stocks having reported their Q4 earnings in this cycle. Here’s a list of reporting dates, Wall Street’s consensus estimates and actual reported results.

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His