-

Ross Stores Earned 91 Cents per Share for Q3

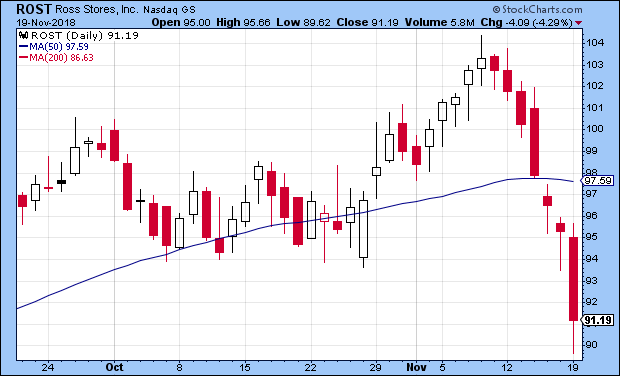

Posted by Eddy Elfenbein on November 20th, 2018 at 9:00 amThis morning, Ross Stores (ROST) reported fiscal Q3 earnings of 91 cents per share. Sales rose 7% to $3.5 billion. The important metric, same-store sales, rose by 3%. Going into this quarter, Ross told us to expect earnings between 84 and 88 cents per share, and same-store sales growth of 1% to 2%. Wall Street had been expecting 90 cents per share.

Barbara Rentler, Chief Executive Officer, commented, “Both sales and earnings for the quarter were ahead of our forecast, despite being up against very strong multi-year comparisons. Though above plan, operating margin of 12.4% was down from last year as higher merchandise margin was more than offset by increases in freight costs and this year’s wage investments.”

Ms. Rentler continued, “During the third quarter and first nine months of fiscal 2018, we repurchased 2.9 million and 9.4 million shares of common stock, respectively, for an aggregate price of $278 million in the quarter and $807 million year-to-date. We remain on track to buy back a total of $1.075 billion in common stock during fiscal 2018.”

For Q4, which is the important holiday quarter, Ross projects same-store sales growth of 1% to 2%. For EPS, they see that ranging between $1.09 and $1.14 per share. That’s the same as the previous guidance but it now includes a gain of seven cents per share due to the resolution of a tax matter. For the entire year, Ross sees earnings of $4.15 to $4.20 per share.

This is basically what I expected. Their Q3 guidance was low, but that’s what they often do. Wall Street wasn’t fooled. The outlook for Q4 is the same as before. Still, the stock gapped down more than 7% at the open. This was on top of a pronounced slide over the last seven days. At today’s low, Ross was down nearly 9%. From the low, the stock was off more than 20% from its high of just eight trading days ago. All of this happened, even though the company did exactly what they said they’d do.

Update: Ross lost 9.38% today to close at $82.64 per share. The stock dropped at the open, then rallied, but gradually pulled back at the end of the day.

-

Hormel Foods Earns 51 Cents per Share

Posted by Eddy Elfenbein on November 20th, 2018 at 8:16 amHormel Foods (HRL), a leading global branded food company, today reported results for the fourth quarter of fiscal 2018. All comparisons are to the fourth quarter of fiscal 2017 unless otherwise noted.

EXECUTIVE SUMMARY – FISCAL 2018

Record diluted earnings per share of $1.86, up 18% from 2017 EPS of $1.57

Excluding a non-cash impairment, adjusted diluted earnings per share1 of $1.89, up 20%

Record cash flow from operations of $1.24 billion, up 20%

Volume of 4.80 billion lbs., up 1%; organic volume1 down 1%

Record net sales of $9.55 billion, up 4%; organic net sales1 down 1%

Operating margin of 12.6% compared to 14.0% last year

Effective tax rate of 14.3% compared to 33.7% last yearEXECUTIVE SUMMARY – FOURTH QUARTER

Record diluted earnings per share of $0.48, up 17% from 2017 EPS of $0.41

Adjusted diluted earnings per share1 of $0.51, up 24%

Volume of 1.27 billion lbs., down 1%; organic volume1 down 3%

Net sales of $2.52 billion, up 1%; organic net sales1 down 3%

Operating margin of 12.8% compared to 13.2% last year

Effective tax rate of 18.7% compared to 33.8% last yearFISCAL 2019 OUTLOOK

“Fiscal 2019 is a continuation of our long-term evolution as a global branded food company,” said Jim Snee, chairman of the board, president, and chief executive officer. “Our focus on building brands, delivering meaningful innovation to the marketplace, making strategic acquisitions, and creating intentional balance will ensure we are able to meet our growth goals. We are confident in our plan to deliver growth in each business segment in 2019.”

“We anticipate another year of strong cash flows. We plan to reinvest to expand capacity for branded value-added products while returning cash back to shareholders through a 12 percent dividend increase,” Snee said. “This coming year will require strong execution from every business unit in order to manage through commodity market volatility and global trade uncertainty. I know our team is up to the challenge.”

“Growth from leading brands such as Wholly Guacamole®, Applegate®, Jennie-O®, and SPAM® will be important to our success in 2019,” Snee said. “We expect continued growth from our many new innovative items such as Herdez® guacamole salsa, Hormel® Bacon 1™ fully cooked bacon, Hormel® Natural Choice® products, and Hormel® Fire Braised™ meats.”

Fiscal 2019 Outlook

Net Sales Guidance (in billions)

$9.70 – $10.20

Earnings per Share Guidance

$1.77 – $1.91

The following items are included in the company’s guidance range. The company plans to deliver $75 million in cost reductions in 2019 which excludes any planned synergies from recent acquisitions. The company will use the savings to help offset inflation, reinvest into key brands, and contribute to earnings growth. The company also expects to complete the Fremont divestiture in December 2018, incurring approximately $12 million in expenses. This transaction reduces earnings volatility and decreases the company’s reliance on commodity profits.

DIVIDENDS

“This morning we announced a 12 percent increase to our annual dividend, making the new dividend $0.84 per share,” Snee said. “This is the 53rd consecutive year in which we’ve increased our dividend and the 10th consecutive year of double-digit increases. This demonstrates the confidence we have in our business going forward.”

Effective November 15, 2018, the company paid its 361st consecutive quarterly dividend at the annual rate of $0.75 per share.

COMMENTARY – FOURTH QUARTER

“Our team delivered a record quarter of earnings,” Snee said. “Refrigerated Foods had a particularly solid quarter led by value-added growth in retail, deli, and foodservice channels which offset a continued decline in commodity profits.”

“We reached many milestones this quarter including the startup of two new lines to support growth of Hormel® Fire Braised™ products and Hormel® Bacon 1™ fully cooked bacon,” Snee said. “We also announced expansions at our Burke manufacturing facility in Nevada, Iowa, and our Fontanini plant in McCook, Ill. These expansions will allow us to continue growing our pizza toppings business as well as our line of authentic premium Italian meats and sausages. These strategic investments reinforce the strength we are seeing in our value-added businesses.”

-

Morning News: November 20, 2018

Posted by Eddy Elfenbein on November 20th, 2018 at 7:12 amOil Prices Slide As Russia Says Wait And See on Production Cuts

No End in Sight for Crypto Sell-Off as Bitcoin Breaches $4,500

Bitcoin-Rigging Criminal Probe Focused on Tie to Tether

FAANG Stocks Drop a Combined $728 Billion — More Than Saudi Arabia’s GDP — in 6-Week Pummeling

Goldman Says It’s Time for Equity Investors to Boost Their Cash

Walmart’s Black Friday 2018 Sale Has A New Nasty Surprise

Societe Generale to Pay $1.4 Billion to Settle Cases in the U.S.

Founder’s Big Idea to Revive BuzzFeed’s Fortunes? A Merger With Rivals

Lowe’s to Get Rid of Mexico Stores in Further Restructuring

David’s Bridal Files For Bankruptcy But Brides Will Get Their Dresses

Ghosn Downfall Ripples From Tokyo to Paris as Allegations Grow

Facebook Deserves Criticism. The Country Deserves Solutions.

Roger Nusbaum: Cryptopocalypse 2018!

Joshua Brown: Okay Here’s What’s Going On

Jeff Carter: Projections Are Never Right

Be sure to follow me on Twitter.

-

Ross Drops Ahead of Earnings

Posted by Eddy Elfenbein on November 19th, 2018 at 7:12 pmRoss Stores (ROST) has fallen for seven days in a row. The total loss is nearly 12%. The deep-discounter reports fiscal Q3 tomorrow morning. This move may reflect fears of a bad report (or it may be overdone).

In the last earnings report, Ross gave guidance for both Q3 and Q4. For Q3, Ross expects same-store sales growth of 1% to 2% and earnings between 84 and 88 cents per share. Wall Street expects 90 cents per share.

For Q4, which is the all-important holiday-shopping quarter, Ross again expects same-store sales growth of 1 to 2%. For earnings, Ross is looking for $1.02 to $1.07 per share. That translates to full-year earnings of $4.01 to $4.10 per share. For Q4, Wall Street expects $1.08 per share.

-

Hormel Foods Raises Dividend by 12%

Posted by Eddy Elfenbein on November 19th, 2018 at 5:03 pmFor the 53rd year in a row, Hormel Foods (HRL) has increased its dividend. The quarterly payout will rise from 18.75 cents to 21 cents per share. That’s a 12% increase. (I had predicted 20 cents per share.)

The annual dividend on the common stock of the corporation was raised to $0.84 per share from $0.75 per share.

The Board of Directors authorized the first quarterly dividend of 21 cents ($0.21) a share to be paid on Feb. 15, 2019, to stockholders of record at the close of business on Jan. 14, 2019.

The Feb. 15 payment will be the 362nd consecutive quarterly dividend paid by the company. Since becoming a public company in 1928, Hormel Foods Corporation has paid a regular quarterly dividend without interruption.

-

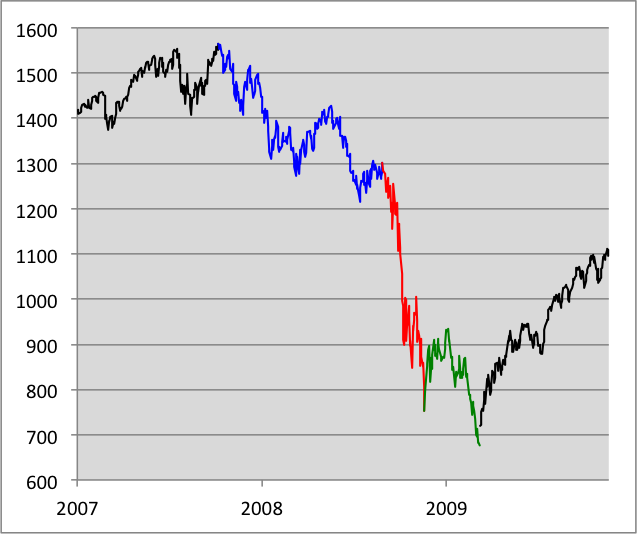

The Panic Low Was Ten Years Ago

Posted by Eddy Elfenbein on November 19th, 2018 at 12:10 pmOne of the important aspects of financial markets is that they tend to be very boring and positive most of the time. Then, very suddenly, they’re very, very exciting and very, very bad for a very, very short period of time. It happens fast.

The market crash of 2008 is a good example. It was ten years ago tomorrow that the stock market reached what I call its “panic low.” I have to explain that I follow a slightly different chronology from convention.

I think it’s better to see the market blowup of 2008-2009 in three segments.

There was the “initial selloff” from October 9, 2007 to August 28, 2008. Then came the “panic phase” from August 29 to November 20, 2008. Finally, there was the “retest phase” from November 20 until March 9, 2009.

The initial selloff lasted 224 days and the S&P 500 lost 16.90% (in blue).

The panic phase lasted 59 days and the market lost 42.15% (in red)

The retest phase was 72 days and the market lost 10.09% (in green)

Others can quibble about precise starting and ending points, but I think my divisions are reasonable.

Officially, the bear market lasted exactly 17 months and the S&P 500 dropped 56.78%.

My point is that even within the parameters of a bear market, there was a much larger and more severe bear market. While the initial phase and retest phases were quite unpleasant, they’re a normal kind of unpleasant.

It’s the panic phase that’s so disquieting (note those performance figures I listed above). The panic phase saw a much bigger drop than the other two combined even though it lasted one-fifth the amount of time.

If you want to try and time the market, you need to be exceedingly precise because the window doesn’t last long. The crash often starts before it’s a news story, and it often ends before people are debating when it will all end.

Things were pretty dicey ten years ago, but it wasn’t a terrible time to go back into the market. Yes — even with another nasty drawdown at the start of 2009. In fact, the entirety of the loss during the retest phase came on its final seven days.

-

Morning News: November 19, 2018

Posted by Eddy Elfenbein on November 19th, 2018 at 7:06 amAPEC Fails to Live Up To Its Name Amid U.S., China Acrimony

An Accountant Stirs Debate as India Central Bank Board Meets

The Trade War Whisperer Battling Trump – One Factory at a Time

Apple Suppliers Suffer as It Struggles to Forecast iPhone Demand

Amazon’s Black Friday 2018 Sale Has Nasty Surprises

Conoco Enters Into Exclusive Talks to Sell U.K. Assets to Ineos

Needing Growth, Uber Returns to Germany. This Time on Best Behavior.

Ghosn Arrested After Icon Is Probed for Financial Violations

Danske’s Cast of Characters Steps Into the Limelight

Yalies Lampert and Freidheim Square Off in Bankruptcy Court

Cullen Roche: Pop Quiz, Hotshot

Michael Batnick: How to Read Performance

Ben Carlson: How the American Consumer Got Addicted to Choice

Be sure to follow me on Twitter.

-

Industrial Production +0.1% in October

Posted by Eddy Elfenbein on November 16th, 2018 at 10:45 amThis morning, the Federal Reserve reported that industrial production rose 0.1% for October. Wall Street had been expecting 0.2%. In the past year, IP is up 4.1%.

Manufacturing production, which accounts for three-quarters of the overall index, continued to grow at a solid pace for the fifth straight month, advancing 0.3% in October from the prior month. Meanwhile, output in the utilities and mining industries fell for the second month in a row in October, declining 0.5% and 0.3%, respectively.

Low unemployment and ramped up wage growth have helped spur consumer demand. At the same time, the late-2017 tax cuts helped stoke business investment, and the U.S. government has increased its defense spending. Rising crude prices in recent years helped the manufacturing industry too, though oil prices have declined in recent weeks.

Capacity utilization, which reflects how much industries are producing compared with what they could potentially produce, fell by 0.1 percentage point to 78.4% in October. Economists had expected 78.2%. Utilization has trended up in recent years, but remains 1.4 percentage points below its long-run average recorded from 1972 to 2017.

-

CWS Market Review – November 16, 2018

Posted by Eddy Elfenbein on November 16th, 2018 at 7:08 am“In a roaring bull market, knowledge is superfluous and experience is a handicap.”

– Benjamin GrahamLast week, I urged caution on the stock market’s rebound. Sure enough, the S&P 500 lost ground five days in a row. The index rebounded on Thursday, but that was after it dropped to its lowest intra-day point this month. The S&P 500 is still below its 200-day moving average, and that’s often a sign that the bears still are in charge.

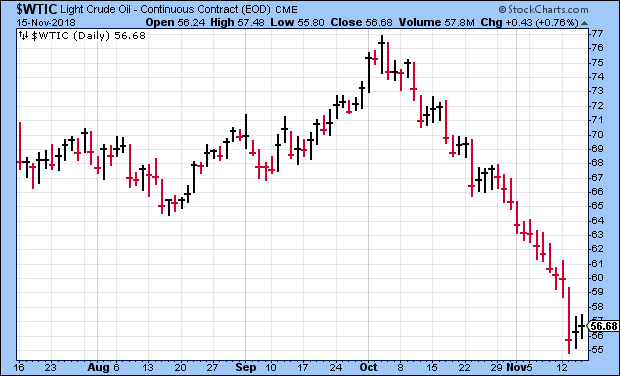

Don’t worry. I’ll explain what this all means for us and our portfolios. Interestingly, the big news recently hasn’t been coming from the stock market. Instead, the oil traders have been making headlines.

The price of crude fell for eleven days in a row. Then on day 12, it had its worst plunge in three years! At one point, West Texas Crude was going for less than $55 per barrel. That’s down from nearly $77 per barrel in early October. The falloff is due to fears of oversupply. Production in the U.S. has been hitting new highs, and the Trump administration granted waivers that are keeping Iran’s oil on the market. (The Saudis are not exactly pleased about that!)

In this week’s CWS Market Review, I’ll break down what it means. I’ll also highlight the performance of our Buy List which has perked up lately. Later on, I’ll preview three Buy List earnings reports coming our way. But first, let’s look at this week’s economic news.

What’s Behind the Plunge in Oil?

On Wednesday, the government reported that consumer inflation had its largest increase in nine months. In last week’s issue, I told you that I suspected that the CPI would run on the high side and might cause the market some drama. For October, consumer prices rose by 0.3%, and over the past year, the CPI is up 2.5%. I also like to look at the “core rate,” which excludes food and energy. Last month, core inflation was 0.2%, and in the past year, it’s been running at 2.2%. That’s quite tame.

The numbers for November will likely be quite different. As I touched on before, oil prices have been tumbling. The Oil Services ETF (OIH) is at a 15-year low. The latest numbers show that domestic crude production rose for the eighth week in a row. OPEC would love to cut production, but it’s not so easy to get everyone on board for that.

Other commodities are down as well. Gold isn’t doing much, and silver recently dropped to a three-year low. This phase might not pass so quickly. With the Fed raising rates, the dollar is now at a 16-month high. The British pound just got hammered due to the chaotic nature of the Brexit drama. Heck, even Bitcoin has been in the dumps.

I don’t believe these recent events will be enough to cause the Fed to pause on rate hikes. There’s a very good chance—though not a rock solid one—that we’ll get another rate hike next month, but after that…well, things get dicey. There’s a decent chance the Fed may take a six-month break to give the economy some breathing room.

The drop in commodities may signal that the world economy isn’t as strong as previously thought. The concern is more about Europe and Asia rather than the United States. As far as America goes, this week’s retail sales report was pretty good, and that could mean we’re in for a strong Q4.

I’m happy to say that our Buy List has been acting better lately. Since November 1, the Buy List is up 2.14% while the S&P 500 is down -0.37%. For the year, we have a slight lead over the S&P 500: +2.65 compared to +2.12% (those figures don’t include dividends; the final numbers will).

Bear in mind that six months ago, our Buy List was trailing the market by more than 3% YTD. This hasn’t been a good climate for stock-pickers, but we’ve held up well. Fourteen of our 25 stocks are beating the market this year. The problem is that the laggards have been pretty bad. Carriage Services (CSV) is down 36% this year which dinged the whole portfolio by 1.6%.

Overall, I’m pleased with our performance. Remember that next month we make our annual changes. According to the rules of the Buy List, we can’t touch our stocks for the entire year. Only at the end of the year are we allowed to break the seal. We’ll add five new stocks, and delete five current stocks. Stay tuned for more details. Now let’s look at three of our stocks that are due to report earnings soon.

Three Upcoming Buy List Earnings Reports

There are three stocks on our Buy List with quarters ending in October. That means they’re due to report earnings soon. Ross Stores and Hormel Foods will report on November 20, while JM Smucker will report on November 28. Let’s run down what to expect.

Ross Stores (ROST) is set to report its fiscal Q3 earnings on Tuesday, November 20. Business has been going well for the deep-discounter, and the share price reflects that. Just last week, ROST hit another new 52-week high, although the shares have pulled back a bit in the last few days due to some weakness in the retail sector.

In the last earnings report, Ross gave guidance for both Q3 and Q4. For Q3, Ross expects same-store sales growth of 1% to 2% and earnings between 84 and 88 cents per share. That sounds about right. For Q4, which is the all-important holiday-shopping quarter, Ross again expects same-store sales growth of 1 to 2%. For earnings, Ross is looking for $1.02 to $1.07 per share. That translates to full-year earnings of $4.01 to $4.10 per share.

The company has bold plans for the future. They’re aiming to buy back more than $1 billion of stock. Ross also plans to open 3,000 stores which is up from the previous goal of 2,500. Fifteen months ago, I said that Ross looks to be “a good value here.” The stock is up 54.80% since then. Let me caution you that the stock has taken near-term hits after the last few earnings reports even though results have been good. The stock eventually shook off all the hits.

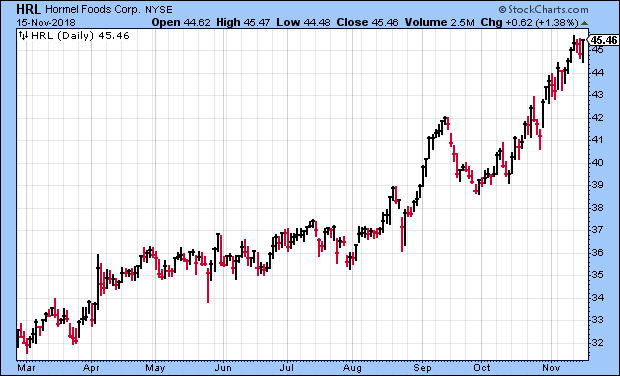

In August, Hormel Foods (HRL) had an OK earnings report, but not a great one. The Spam people said they made 39 cents per share for their fiscal Q3. That matched Wall Street’s expectations. Net sales were up 7% while organic sales were flat. The company said it’s feeling the squeeze from tariffs on U.S. agricultural products. Lean hog prices have been slammed this year, and as a result, Hormel has had to cut prices.

In August, Hormel trimmed its full-year sales range to $9.4 – $9.6 billion but stood by its EPS forecast of $1.81 to $1.95 per share. Since they’ve already made $1.38 per share for the first three quarters of their fiscal year, that implies Q4 earnings of 43 to 57 cents per share. Wall Street expects 49 cents per share.

The stock has been holding up very well this autumn. Since September 27, shares of HRL are up 16.9%. The stock made a new high earlier this week. I also predict that Hormel will increase its dividend. I make this claim based on a detailed analysis of the company’s financial statements. Also, they’ve raised their dividend every year for the last 52 years. Expect #53 soon. The current quarterly dividend is 18.75 cents per share. My guess is that they’ll raise it to 20 cents per share.

JM Smucker (SJM) will report its fiscal Q2 earnings on November 28. In August, the jelly people reported fiscal Q1 earnings of $1.78 per share. That was two cents better than estimates. However, that total included a charge of seven cents due to “a purchase accounting adjustment attributable to acquired Ainsworth inventory.”

Let me explain what’s going on with Smucker and some other big food companies. Basically, this is a fine company. At the moment, however, they’re caught by falling prices. The cost for a lot of the things they make is dropping, and that means they have to pass on the lower prices to consumers. As a result, dollar sales are flat even though sales by volume are doing fine.

Smucker knows what the problem is, and they’re working to address it. That’s why they recently sold off Pillsbury for a cool $375 million and picked up Ainsworth. Of course, it will take a few quarters to see the results of this strategy.

In August, Smucker updated its financial guidance. Importantly, they didn’t alter their full-year EPS range which is still $8.40 to $8.65 per share. They did pare back their revenue estimate from $8.3 billion to $8.0 billion. Smucker also lowered their free-cash range from between $800 million and $850 million to between $770 million and $820 million. The guidance reflects “the anticipated impact from the pending divestiture of its U.S. baking business.”

This is from the Wall Street Journal:

Divesting the baking line, which makes Pillsbury cake mixes, and acquiring pet-snack maker Ainsworth were appropriate moves to adjust Smucker’s portfolio. Ainsworth sales were up 28% from a year earlier in the July quarter, and the company said it expects this growth to be sustained for the full year.

But what Smucker really needs, like fellow struggling food giant Campbell, is a convincing plan to turn around its core brands. With respect to Folgers, Chief Executive Mark Smucker said the company is working on “longer-term initiatives to reinvigorate coffee rituals for this iconic brand.” It was unclear what he meant.

I know what he meant. Smucker will continue to jettison older businesses while concentrating on niche areas. That’s the smart play. This is a company that generates a lot of cash and can easily put those dollars to use.

Let’s look at some numbers: SJM is now going for just 13.2 to 13.6 times this year’s guidance range, plus the dividend yields 3%. In September, Smucker raised its dividend by 9%. That is SJM’s 17th annual dividend hike in a row. Wall Street is expecting earnings of $2.33 per share.

Buy List Updates

On Wednesday, Shareholders of Wabtec (WAB) approved the combination with GE Transportation. At the meeting, 99% of the shares that were voted approved the deal. That’s nice to see. The stock got taken to the woodshed last month, but it seems to have found a base. The GE deal is expected to close in early 2019.

Last month, Sherwin-Williams (SHW) got caught up in the great housing panic of October 2018. In a few weeks, the stock lost one-quarter of its value. On October 25, Sherwin missed earnings and lowered the upper end of its guidance range. Interestingly, that marked the low point for shares of SHW. Since then, the stock has rebounded smartly. At one point, SHW closed higher for eight days in a row. I’m going to cautiously raise my Buy Below on Sherwin to $420 per share (no, that’s not an homage to Elon).

Intercontinental Exchange (ICE) had a good earnings report two weeks ago. The exchange operator beat earnings by five cents per share, and the board announced a $2 billion share buyback. Last quarter was ICE’s 22nd quarter in a row of year-over-year revenue growth. The stock hit a new high on Thursday. This week, I’m hiking my Buy Below on Intercontinental Exchange to $85 per share.

That’s all for now. There will be no newsletter next week. I’m taking my traditional Thanksgiving break. The U.S. stock market will be closed on Thursday for Thanksgiving, and it will close at 1 p.m. on Friday, November 23. There’s not much in the way of economic news scheduled for next week. The housing-starts report will come out on Tuesday, following by the durable-goods report on Wednesday. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

P.S. I’ve recently started a premium Twitter feed where I discuss the markets and investing in greater detail (and without any trolls or stock promoters). This is a great resource for investors. Check it out!

-

Morning News: November 16, 2018

Posted by Eddy Elfenbein on November 16th, 2018 at 7:04 amChip Stock Carnage Seeps Into Asia With $11 Billion Lost

Two Words That Sent the Oil Market Plunging: Negative Gamma

F.D.A. Seeks Restrictions on Teens’ Access to Flavored E-Cigarettes and a Ban on Menthol Cigarettes

The Best Shopping Holiday for Travelers May Not Be Black Friday (But It’s Close)

Deutsche Bank, BofA, JPM Are Drawn Into Danske Probe

Mark Zuckerberg Defends Facebook as Furor Over Its Tactics Grows

Why Amazon Chose the Wrong Locations For Its HQ2

T-Mobile Says Sprint Deal May Close as Early as First-Quarter Next Year

Bankrupt Sears Wins Court Approval for Plans to Sell Stores

Tractor Maker Deere Aims to Ride Green Revolution in Africa

Cryptocurrency Hangover Weighs on Nvidia

PG&E Shares Surge 40% on Report Regulator Wants to Avoid Bankruptcy From Wildfire

Ben Carlson: Revisiting the 4% Rule

Jeff Carter: Eloquence and Bluntness

Jeff Miller: Boost Your JM Smuckers Dividend Yield

Be sure to follow me on Twitter.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His