-

Four Earnings Reports

Posted by Eddy Elfenbein on October 18th, 2018 at 8:26 amThis morning, Danaher (DHR) reported Q3 earnings of $1.10 per share. That’s a 10% increase over last year. Core revenues rose 6.5%. For Q4, Danaher expected earnings between $1.25 and $1.28 per share. The company again increased its full-year guidance. The old range was $4.43 to $4.50 per share. The new range is $4.49 to $4.52 per share.

Thomas P. Joyce, Jr., President and Chief Executive Officer, stated, “We are very pleased with our performance in the third quarter, as the team maintained strong momentum and delivered outstanding results. We achieved 6.5% core revenue growth, solid operating margin expansion and double-digit adjusted earnings per share growth. Four of our five platforms delivered mid-single digit or better core revenue growth, and we believe our investments in innovation and commercial execution are driving market share gains in many of our businesses.”

Joyce continued, “Our recent performance is a testament to the team’s execution and drive for continuous improvement. We believe the strength and differentiation of our portfolio – combined with the power of the Danaher Business System – provides us with the foundation to deliver sustainable, long-term shareholder value.”

Alliance Data Systems (ADS) reported Q3 core earnings of $6.26 per share. That’s five cents above expectations. Core earnings are up 20% this year to $15.70 per share. That puts ADS on track to hit its full-year target of $22.50 to $23.00 per share.

“There were three significant achievements during the third quarter. First, we are now seeing the benefits from shifting to in-house recovery of charged-off accounts in our Card Services segment as recovery rates moved from a multi-quarter drag toward a growing benefit. Second, also in the Card Services segment, we are trending to a record level of new client signings, which will add as much as $4 billion in card receivables growth over time. And third, our LoyaltyOne® segment had another solid quarter of pro forma revenue growth, coupled with momentum in our AIR MILES® Reward Program as evidenced by a nice step-up in AIR MILES issued.

“Shifting to our strategic direction, we have spent the better part of this year reviewing the portfolio of businesses that constitute Alliance Data. We are nearing the end of this process and feel it’s appropriate to share our current thinking.”

Heffernan continued: “Stated simply, we firmly believe that our current stock price does not reflect the intrinsic value of our portfolio of businesses across the enterprise. We are evaluating which assets would likely thrive under a different steward, while also unlocking value for our stockholders. We know that the right answer could involve significant realignment of our businesses and we are actively evaluating that optimal strategy. We expect to crystallize a game plan of precisely − what and how − before year end, and will continue to communicate our path forward when appropriate.”

Snap-On (SNA) earned $2.88 per share which beat estimates by thee cents per share. Sales fell to $898.1 million from $903.8 million in the year-earlier period. Wall Street had been expecting $931 million according to FactSet.

Chairman and Chief Executive Nick Pinchuk said: “While we experienced sales turbulence in our Repair Systems & Information Group this quarter, we believe the vehicle repair markets in which we operate remain robust and afford ongoing opportunity.”

The company said it expects capital expenditures in 2018 will be in the range of $90 million to $100 million, of which $68.5 million was incurred in the first nine months of the year.

Signature Bank (SBNY) reported Q3 earnings of $2.84 per share. That’s up from $2.29 per share from last year. It also beat Wall Street’s estimate by one penny per share.

Total Deposits increased by $1.10 billion to $36.09 billion. Loans increased by $979.7 million, or 2.9%, to $35.13 billion. Net Interest Margin was 2.88% compared with 2.94% for Q2.

-

Morning News: October 18, 2018

Posted by Eddy Elfenbein on October 18th, 2018 at 7:05 amTreasury Opts Against Labeling China A Currency Manipulator

Trump Opens New Front in His Battle With China: International Shipping

Are Jumpy U.S. Equities Hiding a Nasty Surprise?

Trump Attacks the Weak Link Powell Can’t Ignore in Fed Rate Plan

Invesco to Buy OppenheimerFunds, Adding $246 Billion in Assets

Who’s Ahead in the Battery Race?

Powerful Executives Have Stepped Away From the Saudis. Not Softbank’s.

Netflix’s Cash-Fueled Road to Streaming Dominance

Tesla: A Tough Time To Chase Profits

Trump Administration Releases Prudential From Strict Post-Crisis Oversight

Takeda Gets Japanese Approval for $62 Billion Shire Purchase

Dividend Windfall: Santander Latest Target in Germany’s Giant Fraud Probe

Roger Nusbaum: Are Alternatives Working?

Michael Batnick: Animal Spirits: The Healthy Correction

Howard Lindzon: The Common Knowledge Game and Too Small to Fail

Be sure to follow me on Twitter.

-

Fed Minutes Show Hawkish Plan

Posted by Eddy Elfenbein on October 17th, 2018 at 4:26 pmThis afternoon, the Federal Reserve released the minutes of their last meeting. These minutes always take a bit of deciphering to figure exactly what’s going on. Here’s how I see it.

The Fed appears to be on a firm path to continue to raise interest rates. This is despite President Trump’s seeming displeasure with their plans. The market currently expects a rate increase in December, plus three more next year. I should add that the last Fed meeting happened before the stock market started to get antsy.

In the last Fed policy statement, they removed the word “accommodative.” Jay Powell, the Fed chair, downplayed any concerns that it was a change of pace for the Fed. The minutes made it clear that removing the word was not a signal that the rate hikes were coming to an end.

I still think the Fed is being needlessly aggressive with interest rates. Inflation just doesn’t seem to be a problem. I wouldn’t be surprised if the Fed has to ditch its plans for three rate increases in 2019.

-

“Buy American. I Am.” Ten Years Later

Posted by Eddy Elfenbein on October 17th, 2018 at 10:20 amTen years ago yesterday, the New York Times ran an op-ed “Buy American. I Am.” by Warren Buffett. Buffett said that he’s been buying American stocks in his personal account (not Berkshire).

A simple rule dictates my buying: Be fearful when others are greedy, and be greedy when others are fearful. And most certainly, fear is now widespread, gripping even seasoned investors. To be sure, investors are right to be wary of highly leveraged entities or businesses in weak competitive positions. But fears regarding the long-term prosperity of the nation’s many sound companies make no sense. These businesses will indeed suffer earnings hiccups, as they always have. But most major companies will be setting new profit records 5, 10 and 20 years from now.

Let me be clear on one point: I can’t predict the short-term movements of the stock market. I haven’t the faintest idea as to whether stocks will be higher or lower a month — or a year — from now. What is likely, however, is that the market will move higher, perhaps substantially so, well before either sentiment or the economy turns up. So if you wait for the robins, spring will be over.

A little history here: During the Depression, the Dow hit its low, 41, on July 8, 1932. Economic conditions, though, kept deteriorating until Franklin D. Roosevelt took office in March 1933. By that time, the market had already advanced 30 percent. Or think back to the early days of World War II, when things were going badly for the United States in Europe and the Pacific. The market hit bottom in April 1942, well before Allied fortunes turned. Again, in the early 1980s, the time to buy stocks was when inflation raged and the economy was in the tank. In short, bad news is an investor’s best friend. It lets you buy a slice of America’s future at a marked-down price.

Over the long term, the stock market news will be good. In the 20th century, the United States endured two world wars and other traumatic and expensive military conflicts; the Depression; a dozen or so recessions and financial panics; oil shocks; a flu epidemic; and the resignation of a disgraced president. Yet the Dow rose from 66 to 11,497.

(…)

Equities will almost certainly outperform cash over the next decade, probably by a substantial degree. Those investors who cling now to cash are betting they can efficiently time their move away from it later. In waiting for the comfort of good news, they are ignoring Wayne Gretzky’s advice: “I skate to where the puck is going to be, not to where it has been.”

I don’t like to opine on the stock market, and again I emphasize that I have no idea what the market will do in the short term. Nevertheless, I’ll follow the lead of a restaurant that opened in an empty bank building and then advertised: “Put your mouth where your money was.” Today my money and my mouth both say equities.

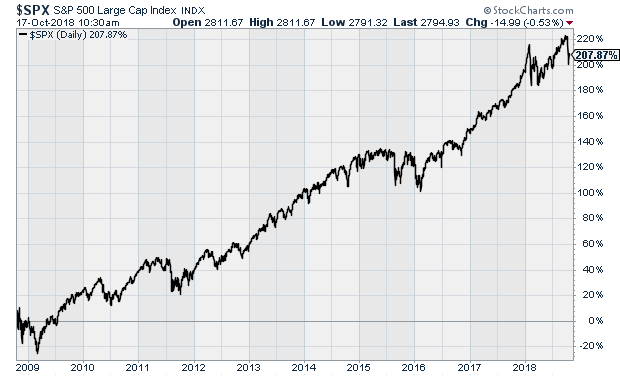

Ten years on and the S&P 500 has more than tripled.

The Total Return Index is up 280%.

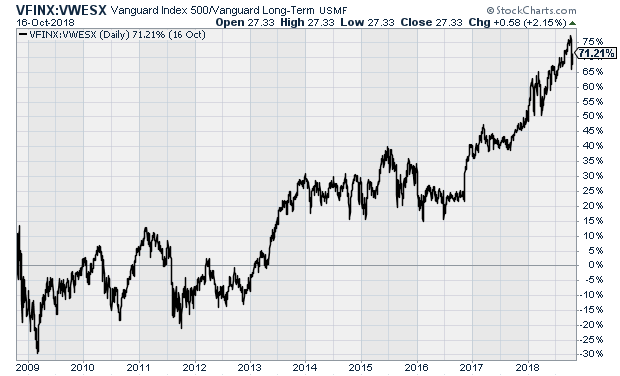

And what about his call that stocks would beat cash? He was correct. Cash has paid almost nothing. In fact, stocks have creamed bonds as well.

Here’s the Vanguard S&P 500 Index Fund divided by their Long-Term Corporate Bond Index Fund.

-

Morning News: October 17, 2018

Posted by Eddy Elfenbein on October 17th, 2018 at 7:05 amDon’t Mention the Oil Price – U.S. Legal Threat Prompts Change at OPEC

No, Trump’s Tax Cut Isn’t Paying for Itself (At Least Not Yet)

Trump Economy Needs California, Which Scorns Trump Economics

Bond Traders Are Paid Big to Dump U.S. Treasuries and Go Abroad

America Is Drowning in Milk Nobody Wants

Disney Bets $20 Million to Ensure Florida Isn’t the Next Vegas

Netflix Keeps Adding Subscribers, and Market Investors Could Profit

Tesla Secures Shanghai Site for $2 Billion China Gigafactory

Uber and Lyft Charge Toward Potential IPOs Next Year

Express Scripts Covers Amgen, Lilly Migraine Therapies, Excludes Teva Drug

Clueless on What to Save for Retirement? You’re in Good Company

Ben Carlson: The Worst Kind of Bear Market

Howard Lindzon: Momentum Monday – Weed and Gold?

Jeff Carter: Different Strokes For Different Exchanges

Be sure to follow me on Twitter.

-

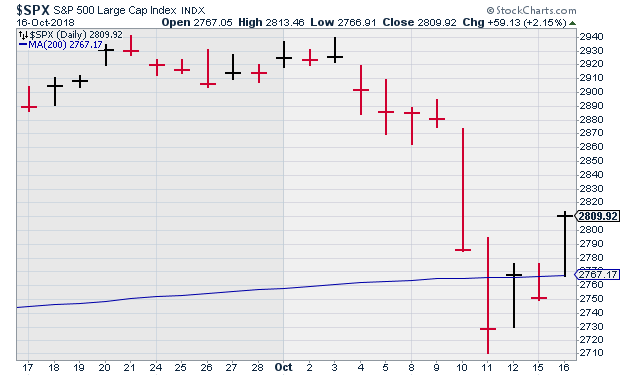

Another Close Above the 200-DMA

Posted by Eddy Elfenbein on October 16th, 2018 at 4:09 pmThanks to a strong rally today, the S&P 500 closed above its 200-day moving average.

On Thursday, we closed below the 200-DMA but rallied above it on Friday. We repeated that this week, closing below the 200-DMA yesterday and above today.

We still haven’t had back-to-back closes below the 200-DMA in more than two years.

-

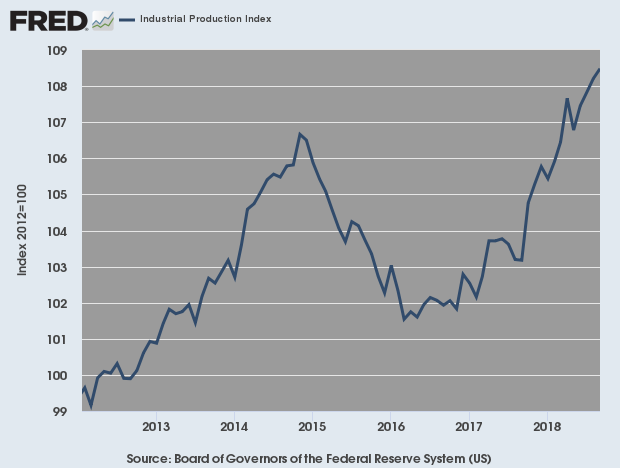

Industrial Production Rose 0.3%

Posted by Eddy Elfenbein on October 16th, 2018 at 9:52 amMore good news for the economy.

U.S. industrial production increased for a fourth straight month in September, boosted by gains in manufacturing and mining output, but momentum slowed sharply in the third quarter.

The Federal Reserve said on Tuesday industrial production rose 0.3 percent last month after an unrevised 0.4 percent increase in August. Industrial output grew at a 3.3 percent annualized rate in the third quarter after accelerating at a 5.3 percent pace in the second quarter.

The Fed said industrial output in September had been held down “slightly” by Hurricane Florence, which drenched South and North Carolina in mid-September. The U.S. central bank estimated the impact of the storm on industrial production as “less than 0.1 percentage point.”

Manufacturing output increased 0.2 percent in September after rising 0.3 percent in August.

A 1.7 percent increase in motor vehicle production helped to lift manufacturing output last month. Motor vehicle production surged 4.3 percent in August.

This bodes well for the GDP report which is due out next Thursday.

-

Morning News: October 16, 2018

Posted by Eddy Elfenbein on October 16th, 2018 at 6:58 amChina May Have $5.8 Trillion in Hidden Debt With ‘Titanic’ Risks

Currency Manipulation Isn’t Among China’s Trade Sins

U.S. Credit Card Giants Flout India’s New Law on Personal Data

Google’s CEO Defends Potential Return to China

Landlords Across America Are Cheering Sears’ Bankruptcy

Fidelity Says It Will Trade Bitcoin for Hedge Funds

Jeff Bezos Chides Rivals, Says Amazon Will Continue to Work With Pentagon

Bank of America Profit Jumps 32%

Can 18 Hours in the Air Be Bearable? Airlines Bet on Ultra-Long-Haul Flights

Paul Allen, Billionaire Who Co-Founded Microsoft, Dies at 65

Climate Chnge to Cause Global Beer Shortage, Study Says

Nick Maggiulli: What is Your Financial Tipping Point?

Jeff Carter: Different Strokes For Different Exchanges

Joshua Brown: The Company That Saves Portfolio Managers From Themselves

Be sure to follow me on Twitter.

-

Some Stability Returns

Posted by Eddy Elfenbein on October 15th, 2018 at 11:51 amThe market is a lot calmer today after last week’s drama, but we’re not in the clear just yet. I expect more volatility soon.

As expected, Signature Bank (SBNY) confirmed that their earnings report will be on Thursday. I don’t know why it takes them so long. We have four Buy List reports on Thursday.

This morning’s retail sales report showed an increase of 0.1%. Economists were expecting an increase of 0.6%. We also saw the biggest drop in spending at bars and restaurants in nearly two years.

Excluding automobiles, gasoline, building materials and food services, retail sales jumped 0.5 percent last month. These so-called core retail sales correspond most closely with the consumer spending component of gross domestic product.

Data for August was revised down to show core retail sales were unchanged instead of the previously reported 0.1 percent gain. Consumer spending is being driven by a robust labor market, with the unemployment rate near a 49-year low of 3.7 percent. Tight labor market conditions are gradually pushing up wage growth.

The solid core retail sales increase in September pointed to strong consumer spending that should offset anticipated drags on economic growth from a widening trade deficit and persistent weakness in the housing market. Growth estimates for the third quarter are above a 3.0 percent annualized rate. The economy grew at a 4.2 percent pace in the second quarter.

Now I’m curious about next week’s GDP report. This will be our first look at Q3 growth. The Q2 number was pretty good: +4.2%. The problem with this expansion is that it’s been very hard to string together more than a few quarters of decent growth.

-

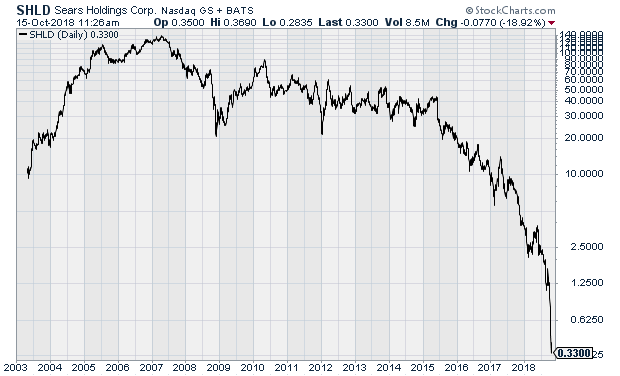

Sears Goes Bankrupt

Posted by Eddy Elfenbein on October 15th, 2018 at 11:19 amAfter 126 years in business, Sears has gone under. This was both unexpected and completely expected. As a student of business, I have a soft spot for Sears. This was the Amazon of its day. The company invented modern retail. Sears catalogues were a regular part of American life for decades.

Sam: Cliff, you look terrible. Was today Sears catalogue day?

Cliff: And that’s not all, Spiegel’s catalogue came out the same day. Yeah, it’s a phenomenon that happens once every 27 years when both marketing strategies are in the same equinox.

Sears had the largest warehouses in the world and the largest building. So many innovations started at Sears: precision inventory control, Allstate, the Discover card, Dean Witter. Sears was a Dow component from 1924 to 1999.

Interestingly, Sears started as a mail-order watch business that eventually branched out into…well, everything. You could even buy a mail-order house.

Four years ago, Sears was going for $48 per share. Today it’s at 35 cents.

“How did you go bankrupt?”

“Two ways. Gradually, then suddenly.”― The Sun Also Rises

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His