-

The Eight Best Predictors of the Stock Market

Posted by Eddy Elfenbein on August 6th, 2018 at 11:48 amIn the WSJ, Mark Hulbert look at the eight best metrics to predict the stock market. The best is from the blog Philosophical Economics.

The blog’s indicator is based on the percentage of household financial assets—stocks, bonds and cash—that is allocated to stocks. This proportion tends to be highest at market tops and lowest at market bottoms.

According to data collected by Ned Davis Research from the Federal Reserve, this percentage currently looks to be at 56.3%, more than 10 percentage points higher than its historical average of 45.3%. At the top of the bull market in 2007, it stood at 56.8%.

Ned Davis, the eponymous founder of Ned Davis Research, calls the indicator’s record “remarkable.” I can confirm that its record is superior to seven other well-known valuation indicators analyzed by my firm, Hulbert Ratings.

This metric has an R-square of 0.61. Here are the seven others:

• The Q ratio, with an R-squared of 46%. This ratio—which is calculated by dividing market value by the replacement cost of assets—was the outgrowth of research conducted by the late James Tobin, the 1981 Nobel laureate in economics.

• The price/sales ratio, with an R-squared of 44%, is calculated by dividing the S&P 500’s price by total per-share sales of its 500 component companies.

• The Buffett indicator was the next-highest, with an R-squared of 39%. This indicator, which is the ratio of the total value of equities in the U.S. to gross domestic product, is so named because Berkshire Hathaway Inc.’s Warren Buffett suggested in 2001 that is it “probably the best single measure of where valuations stand at any given moment.”

• CAPE, the cyclically adjusted price/earnings ratio, came next in the ranking, with an R-squared of 35%. This is also known as the Shiller P/E, after Robert Shiller, the Yale finance professor and 2012 Nobel laureate in economics, who made it famous in his 1990s book “Irrational Exuberance.”

The CAPE is similar to the traditional P/E except the denominator is based on 10-year average inflation-adjusted earnings instead of focusing on trailing one-year earnings.

• Dividend yield, the percentage that dividends represent of the S&P 500 index, sports an R-squared of 26%.

• Traditional price/earnings ratio has an R-squared of 24%.

• Price/book ratio—calculated by dividing the S&P 500’s price by total per-share book value of its 500 component companies—has an R-squared of 21%.

According to various tests of statistical significance, each of these indicators’ track records is significant at the 95% confidence level that statisticians often use when assessing whether a pattern is genuine.

However, the differences between the R-squareds of the top four or five indicators I studied probably aren’t statistically significant, I was told by Prof. Shiller. That means you’re overreaching if you argue that you should pay more attention to, say, the average household equity allocation than the price/sales ratio.

For the record, I’m a bit skeptical of these metrics. Sure, they’re interesting to look at, but I try to place them within a larger framework.

It’s not terribly hard to find a measure that shows an overvalued market and then use a long time period to show the market has performed below average during your defined overvalued period. That’s easy.

The difficulty is in timing the market. For example, during the housing bubble, what I found interesting was how many people were right that housing was indeed in a bubble.

Lots of people realized it. Also, lots of people thought it would burst in 2004. Then in 2005. Then in 2006. They were right, but their timing was way off. This happened to Michael Burry of The Big Short fame. Even if you know the market is overpriced, that doesn’t tell you much about how to invest today.

-

Morning News: August 6, 2018

Posted by Eddy Elfenbein on August 6th, 2018 at 7:17 amFriendship No More: How Russian Gas is a Problem for Germany

A Culture War Is Brewing Between Bitcoin’s Old and New Money

Jamie Dimon Warns of 5% Treasury Yields

China Meets Trump’s Tariff Hardball With Pledge to Endure

Steel Giants With Ties to Trump Officials Block Tariff Relief for Hundreds of Firms

Power Worth Less Than Zero Spreads as Green Energy Floods the Grid

Profits Surge at Big U.S. Firms

Apple’s Value Hit $1 Trillion. Add Disney to Bank of America and…You’re Halfway There.

Linde, Praxair Fall as U.S. Antitrust Demands Threaten Deal

Pepsi’s First Female CEO to End 12-Year Run, Replaced by Insider

Rising Costs and U.S. Settlement Crimp HSBC’s First-Half Profit

Disney’s Streaming Service Starts to Come Into Focus

Michael Batnick: The Longest Bull Market of All-Time?

Ben Carlson: If It Sounds Too Good to Be True…

Joshua Brown: Hot Chart: The A-D Line is Roaring Higher

Be sure to follow me on Twitter.

-

Sandler O’Neill on AFL

Posted by Eddy Elfenbein on August 5th, 2018 at 9:04 amThis week, Sandler O’Neill upgraded AFLAC (AFL). Here’s some of what they had to say:

We are upgrading shares of the provider of mostly supplemental health and life insurance, primarily in Japan and the U.S., to a Buy rating from a Hold. We’ve done this for four reasons. 1) With the company’s Japan-branch conversion and reorganization completed, second-quarter 2018’s earnings results revealed that there was considerable pent-up Japanese agent demand for Japanese products, which is now being taken into account. 2) It appears that the company has finally cracked the mystery of getting U.S. distribution of its Japanese products. 3) It has also become a beat-and-raise story with the shift in its products into third sector from first sector, which in Japan allows the sale of a wider range of insurance products under one company name. 4) While Aflac is often described as a life insurance company when it’s compared with other insurers, it will be more attractive to investors if it clearly presents the wider range of its products.

Our target price stands at $52.

-

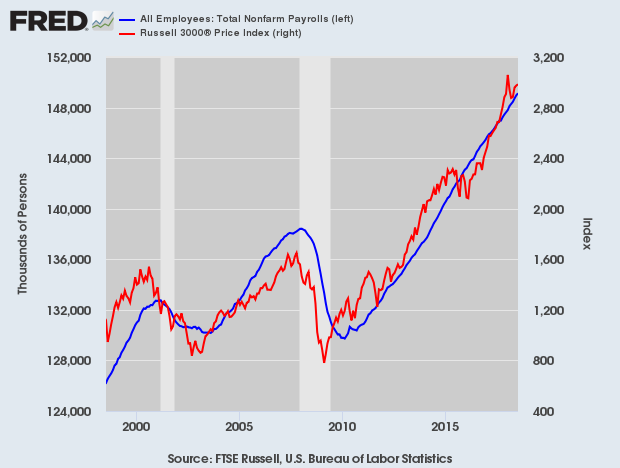

July NFP = +157%. Unemployment = 3.9%

Posted by Eddy Elfenbein on August 3rd, 2018 at 11:38 amToday’s jobs report showed that the U.S. economy created 157,000 net new jobs last month. That’s a bit light, but nothing serious. The number tends to wiggle around some. The numbers for May and June were revised up by 59,000. The unemployment rate ticked down to 3.9%. That’s close to a 50-year low.

Average hourly earnings rose by seven cents in July to $27.05. In the last year, wages are up 2.7%. The labor force participation rate is at 62.9%. (That number had barely moved in five years.)

Here’s the last 20 years of nonfarm payrolls along with the Russell 3000.

-

CWS Market Review – August 3, 2018

Posted by Eddy Elfenbein on August 3rd, 2018 at 7:08 am“Paying attention to simple little things that most men neglect makes a few men rich.” – Henry Ford

I think we just set a record. Nine of our Buy List stocks reported Q2 earnings this week including seven on Thursday. I can’t remember a single day with so many reports to go through. Fortunately, this was the final batch for us this earnings season. This was an outstanding earnings season for us. Over the last two weeks, 21 out of our 25 Buy List stocks have reported earnings. All but two beat Wall Street’s estimates.

In this week’s CWS Market Review, I’ll run through all the reports. Plus, I have some new Buy Below prices for you. I promise to have more thoughts on the broader economy in upcoming issues, but this week’s issue is all about earnings. I was also happy to see how many of our companies reiterated, or even raised, their full-year guidance. That’s a very positive sign for the rest of the year.

We also had a Federal Reserve meeting on Tuesday and Wednesday. The Fed decided against raising interest rates this meeting, but they noted the recent strength in the economy. I think that means we’ll get another rate hike next month, and there’s a decent change we’ll get one more before Christmas.

But first, we have lots of earnings to get through. Let’s start with Moody’s, which continues to be one my favorite stocks.

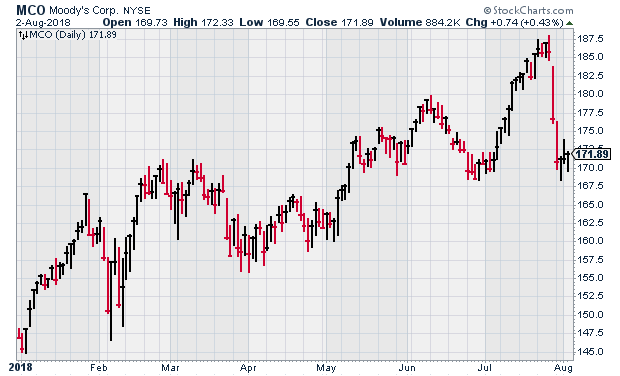

Moody’s Reports Strong Earnings, but the Shares Fall

Yes, I like Moody’s (MCO) a lot. It’s an excellent company. The stock is up 16% this year. Moody’s released their latest earnings report last Friday, not long after I sent you last week’s newsletter. The credit-ratings agency reported Q2 earnings of $2.04 per share. That beat Wall Street’s consensus by 15 cents per share.

This was a solid quarter for Moody’s. Quarterly revenue rose 17% over last year. I’m particularly impressed by the growth of the Moody’s Analytics business, plus Bureau van Dijk. Most importantly, Moody’s reaffirmed their full-year EPS guidance of $7.65 to $7.85. Still, traders weren’t impressed. Perhaps they were expecting higher guidance. Shares of MCO lost nearly 5% on Friday, plus another 3% on Monday.

I’m not worried at all. Moody’s will do well. I know it’s frustrating when a good company reports strong results and the stock takes a hit. Still, we know this can happen with financial markets. Don’t worry about Moody’s. The most important news is the full-year guidance. Due to the pullback, I’m dropping my Buy Below price on Moody’s down to $182 per share.

Earnings from Fiserv and Carriage Services

On Tuesday we got earnings reports from Fiserv and Carriage Services. For Q2, Fiserv (FISV) made 75 cents per share. That was one penny better than estimates. This is another rock-solid financial-services firm. Fiserv reiterated its full-year guidance of $3.02 to $3.15 per share on internal revenue growth of at least 4.5%. That’s good to hear.

Fiserv’s CEO, Jeffery Yabuki, said, “Our first-half performance has set us up for strong full-year results and additional momentum as we look into 2019.”

“Our second-quarter results were excellent and have us well-positioned to achieve our full-year objectives,” said Jeffery Yabuki, President and Chief Executive Officer of Fiserv. “We continue to focus on service quality, innovation and integration, which is reflected in both our current results and sales pipeline entering the second half of the year.”

Corporate boilerplate? Sure, but it’s still true. Since Fiserv has already made $1.51 per share for the first half, the guidance means they expect $1.51 to $1.64 per share for the second half.

I was especially pleased to see Fiserv’s operating margin expand by 0.4% to 32.4% for Q2. That’s often a sign that business is going well. The shares pulled back a little after the earnings report, but it’s nothing too serious. I’m keeping my Buy Below on Fiserv at $81 per share.

Carriage Services (CSV) was our big disappointment this earnings season. This was one of the two that missed Wall Street’s consensus (RPM was the other). Actually, that phrase really doesn’t apply much to Carriage since only two analysts follow the stock. The average of the two was for 37 cents per share, and Carriage earned just 22 cents per share last quarter.

The company blamed the poor showing on two factors: “broadly lower volumes and average revenue due to a spike in cremation rates in both our Same Store and Acquisition Funeral Portfolios, and higher interest costs and an increase in outstanding common shares after our recent balance-sheet recapitalization.”

I should note that the company remains optimistic for the coming quarters. They said they forecast earnings of $1.35 to $1.40 per share for the coming four quarters. The stock dropped for a 4.3% loss on Wednesday. I was afraid it was going to be a lot more. The fall isn’t so bad considering the stock rallied 3.7% on Tuesday. Still, I’m lowering our Buy Below price to $26 per share. I want to see improvement here.

Seven Buy List Earnings Reports on Thursday

Thursday was a very busy day for us. Seven of our Buy List stocks reported. Five were before the opening bell, and two came after after the close.

Let’s start with Cognizant Technology Solutions (CTSH). The IT-outsourcer earned $1.19 for Q2. That was nine cents better than estimates. Quarterly revenue rose 9.2% to $4.01 billion. Very good quarter.

For Q3, CTSH expects earnings of at least $1.13 per share. That was a penny less than where Wall Street was. Also, the revenue guidance was a bit light. For all of this year, Cognizant now expects earnings of at least $4.50 per share. This is notable because three months ago, Cognizant lowered its full-year EPS guidance from $4.53 to $4.47. So they’ve reclaimed some of that lost ground.

Despite the higher earnings guidance, traders focused on the weak revenue outlook. Cognizant lost over 6% on Thursday. I’m not too worried. This probably reflects a temporary slowdown in the financial-services sector rather than deeper business issues. I’m keeping our Buy Below at $81 per share.

Becton, Dickinson (BDX) reported earnings of $2.91 for Q2. That beat the Street by three cents, and it was up 18.3% over last year. Becton also raised its revenue guidance for this year. Plus, they bumped up the low end of their full-year forecast. Becton now sees full-year EPS of $10.95 to $11.05 from a previous range of $10.90 to $11.05. Granted, that’s not a big change, but it’s good to see. Becton is quietly becoming a nice winner for us. I’m keeping our Buy Below at $250 per share.

There’s no way to sugarcoat the problems at Ingredion (INGR). The stock has been a very poor performer for us this year. Ingredion warned that its Q2 results would be between $1.63 and $1.68 per share. That was well below Wall Street’s consensus of $1.92 per share. On Thursday, we got the results. For Q2, Ingredion made $1.66 per share. They stood by their full-year guidance of $7.50 to $7.80 per share. Perhaps the worst is over.

The stock rallied a bit after the earnings, probably in relief that there wasn’t any more bad news. At least we can say that Ingredion is going for a decent valuation. Going by the current guidance, INGR is trading at 12.5 to 13 times earnings. Not much else to say, but I’m not pleased with Ingredion’s performance this year.

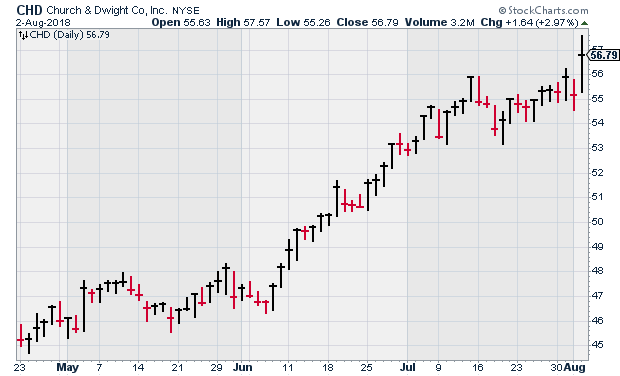

Church & Dwight (CHD) is quickly becoming a favorite around here. The stock is up more than 25% since last April. The company had been expecting Q2 earnings of 46 cents per share. Last week, I said they should beat that, and I was right. CHD made 49 cents for Q2. Net sales grew 14.5% to $1.03 billion. Church & Dwight raised the low end of its guidance. CHD now expects EPS of $2.26 to $2.28 (previously, it was $2.24 to $2.28). For Q3, they’re looking for 53 cents per share. I’m raising my Buy Below to $60 per share.

Intercontinental Exchange (ICE) had Q2 earnings of 90 cents per share. That’s an 18% increase over last year, and it beat the Street by one penny. ICE expects Q3 data revenue between $530 million and $532 million, and for Q4, it’s expected to be between $538 million and $542 million. The CFO said, “In the first half of 2018, we grew revenues, expanded margins and generated over $1.2 billion of operating cash flow.” This is a solid company. Buy up to $79 per share.

Cerner (CERN) reported after the closing bell on Thursday. The company made 62 cents per share which was two cents ahead of estimates. Revenue for Q2 was up 6% to $1.368 billion. For Q3, Cerner expects revenue between $1.335 billion and $1.385 billion and earnings between 62 and 64 cents per share. Wall Street had been expecting 65 cents per share. Cerner also stood by its full-year EPS range of $2.45 to $2.55.

“I am pleased with our second-quarter results, which included all key metrics being at or above expected levels,” said Zane Burke, President. “Our results were solid across all of our major solution and services categories and included good contributions from U.S. and non-U.S. regions. Looking ahead, we believe our solutions and tech-enabled services are well aligned with the challenges providers and other healthcare stakeholders are facing, and we have a significant opportunity to grow as we help them with their transition to value-based care in coming years.”

This was a good report. I’m going to bump up my Buy Below price on Cerner to $67 per share.

Continental Building Products (CBPX) had a blow-out earnings report. The wallboard outfit made 59 cents per share, which was 14 cents more than estimates. The details of the report are quite good. Net sales were up 15.5%, while EBITDA rose more than 21%. Gross margins improved to 29.4% from 25.5%. It’s not just about price increases; wallboard sales volume rose from 647 million square feet last year to 722 million square feet this year.

Continental doesn’t provide EPS guidance, but they do give expected ranges for some internal budget numbers. They pared back some of those by a little bit in this latest report. For now, I’m keeping our Buy Below at $34 per share, but I may raise it soon depending on how the market reacts.

That’s all for now. With earnings out of the way, next week should be a lot calmer. Later today, we’ll get the jobs report for July and it could be another big one. There’s not much in the way of economic reports next week. However, I will be curious to see next Friday’s CPI report. I suspect that some inflation may slowly be brewing, but I want to see hard data first. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Syndication Partners

I’ve teamed up with Investors Alley to feature some of their content. I think they have really good stuff. Check it out!

Buy These 3 High-Yield Stocks with Positive Earnings Surprises

Earnings season is in full swing, with a large portion of the high yield stock universe reporting in the first half of August. Predicting what will happen with individual company earnings is a tough sport and guessing how share prices will react is more like wagering on sports events. However, earnings is the time when a company can show that the market price of a stock is far out of line with the business fundamentals.

I seem to always have a handful of companies on my watch list where I believe the underlying business fundamentals are much stronger than the current stock market value indicates. These stocks may be down for a variety of reasons such as a one time bad earnings report, or a misperception of the company’s growth potential. Here are three stocks that could move up nicely after hopefully positive earnings reports.

Is It Time to Bail on the FAANGs?

In recent months, it has gotten harder to separate the performance of the U.S. stock market from the performance of the FAANG stocks (Facebook, Amazon, Apple, Netflix and Google).

Despite Facebook’s face-plant, after its earnings announcement led to the worst one-day loss ever for any stock, the overall performance of the market year-to-date has been supported by the FAANG group. While they’re only a 13.6% weight in the S&P 500’s market cap, they’re driving the market up to the tune of almost half of its year-to-date gains. Impressive stuff for just 5 stocks on their own.

The question facing investors is, of course, whether the FAANG stocks will continue carrying the market or if their leadership is beginning to fade.

-

Morning News: August 3, 2018

Posted by Eddy Elfenbein on August 3rd, 2018 at 7:05 amChina Dethroned by Japan as World’s Second-Biggest Stock Market

Is Something Important Happening To Oil Prices?

U.S. Is Expanding Power to Block Chinese Firms. HNA Was Already No Match.

Don’t Count Out The Growth Stocks Just Yet

Cisco to Acquire Security Unicorn Duo for $2.35 Billion

BMW Weighs Measures to Counter Tariff Impact

All The Reasons Tesla Stock Popped After The Q2 Conference Call

Heineken Strikes Multibillion-Dollar China Deal

Amazon Prime Video is Coming to Comcast’s Cable Boxes

Three Theories on Why MoviePass Failed

Roger Nusbaum: Trillion Dollar Hats

Howard Lindzon: Fintech Week – The Language Of The Markets

Blue Harbinger: Stock Exchange: What Is Your Typical Timeframe?

Be sure to follow me on Twitter.

-

Cerner Earns 62 Cents per Share

Posted by Eddy Elfenbein on August 2nd, 2018 at 4:12 pmBookings in the second quarter of 2018 were $1.775 billion, an increase of 9 percent compared to $1.636 billion in the second quarter of 2017.

Second quarter revenue was $1.368 billion, an increase of 6 percent compared to $1.292 billion in the second quarter of 2017.

Adjusted Net Earnings for the second quarter of 2018 were $207.0 million compared to $205.5 million of Adjusted Net Earnings in the second quarter of 2017. Adjusted Diluted Earnings Per Share (EPS) were $0.62 in the second quarter of 2018 compared to $0.61 of Adjusted Diluted EPS in the year-ago quarter. Analysts’ consensus estimate for second quarter 2018 Adjusted Diluted EPS was $0.60.

“I am pleased with our second quarter results, which included all key metrics being at or above expected levels,” said Zane Burke, President. “Our results were solid across all of our major solution and services categories and included good contributions from U.S. and non-U.S. regions. Looking ahead, we believe our solutions and tech-enabled services are well aligned with the challenges providers and other health care stakeholders are facing, and we have a significant opportunity to grow as we help them with their transition to value-based care in coming years.”

Cerner currently expects:

-Third quarter 2018 revenue between $1.335 billion and $1.385 billion

-Full year 2018 revenue between $5.325 billion and $5.450 billion, consistent with previously provided full year guidance

-Third quarter 2018 Adjusted Diluted Earnings Per Share between $0.62 and $0.64

-Full year 2018 Adjusted Diluted Earnings Per Share between $2.45 and $2.55, consistent with previously provided guidance

-Third quarter 2018 new business bookings between $1.450 billion and $1.650 billion -

Five Earnings Reports this Morning

Posted by Eddy Elfenbein on August 2nd, 2018 at 8:23 amThis is a busy morning for us. We had five of our Buy List stocks report earnings, plus two more will come later today. Here’s a summary.

Cognizant Technology Solutions (CTSH) earned $1.19 for Q2. Quarterly revenue rose 9.2% to $4.01 billion. For Q3, CTSH expects earnings of at least $1.13 per share. For all of this year they expect at least $4.50 per share.

Becton, Dickinson (BDX) had EPS of $2.91. That’s up 18.3% or 11.0% on a currency-neutral basis.

BDX raised its 2018 revenue guidance and now expects growth to exceed 31.5% on a reported basis compared to previous guidance of approximately 31.0% to 31.5%.

Becton bumped up the low end of their full-year forecast. They now see full-year EPS of $10.95 to $11.05 up from a previous range of $10.90 to $11.05.

Ingredion (INGR) had second quarter EPS of $1.66. 2018 adjusted EPS were expected to be in the range of $7.50 to $7.80. During the second quarter, the company repurchased 1.25 million shares.

Church & Dwight (CHD) earned 49 cents per share. That’s up 19.5% from a year ago. Net sales grew 14.5% to $1,027.9 million. The company raised the low end of its guidance. CHD now expects EPS of $2.26 to $2.28 (previously, it was $2.24 to $2.28). For Q3, they’re looking for 53 cents per share.

Intercontinental Exchange (ICE) had Q2 earnings of 90 cents per share. That’s an 18% increase over last year.

The company expects Q3 data revenue between $530 million and $532 million. For Q4, it’s expected to be in the range of $538 million to $542 million.

-

Q2 2018 Earnings Calendar

Posted by Eddy Elfenbein on August 2nd, 2018 at 7:12 amIn this current earnings season, 21 of our 25 Buy List stocks are reporting Q2 earnings. Here’s a list of reporting dates, Wall Street’s consensus estimates and actual reported results.

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His