-

Cognizant Earns $1.06 per Share

Posted by Eddy Elfenbein on May 7th, 2018 at 7:43 amThis morning, Cognizant Technology (CTSH) reported fiscal Q1 earnings of $1.06 per share. They had been expecting at least $1.04 per share. Q1 was up from 84 cents per share one year ago. Quarterly revenue rose 18.4% to $3.91 billion. Their operating margin was just over 20%, which is nice to see.

“We achieved solid financial results in the first quarter and progressed our shift to digital services and solutions,” said Francisco D’Souza, Chief Executive Officer. “Cognizant has built the capabilities and scale to help clients digitize their offerings, create personalized customer experiences, instrument their operations, and modernize their IT infrastructure. This digital-at-scale value proposition is winning with clients and positioning us well to deliver a strong 2018.”

Now for guidance. Cognizant expects Q2 earnings of at least $1.09 per share and revenues between $4 and $4.04 billion. Wall Street had been expecting $1.12 per share. Cognizant is lowering its full-year forecast. Originally it was for earnings of at least $4.53 per share. Now they expect at least $4.47 per share.

“First quarter results demonstrate solid execution of our plan to drive sustainable revenue growth while increasing margins,” said Karen McLoughlin, Chief Financial Officer. “Our full year 2018 non-GAAP diluted EPS guidance reflects a higher than originally anticipated effective income tax rate due to the updated interpretation of the U.S. Tax Cuts and Jobs Act of 2017. Our strong balance sheet and cash flows continue to support both our capital return program and our investments in the business to drive future growth and continue our shift to digital services and solutions.”

-

Morning News: May 7, 2018

Posted by Eddy Elfenbein on May 7th, 2018 at 7:12 amChina’s ZTE Applies to Suspend Ban on Buying US Technology

What Europe’s Tough New Data Law Means for You, and the Internet

U.S. Oil Cracks $70, Dollar Heads Towards 2018 High

Nestle Pays $7.2 Billion to Sell Starbucks Coffee

Air France-KLM Shares Plunge After CEO Quits Amid Ongoing Labor Battle

Obama’s Calorie Rule Kicks in Thanks to Trump

YouTube Nerd Taunts Wall Street After Wild Tesla Call

The World’s Fifth Largest Economy Is About to Require Solar Panels for All New Homes

New MIT A.I. Could Send Self-Driving Cars Down Roads Less Traveled

Berkshire’s Annual Meeting: Buffett Approves of Apple’s Buyback Program

Blackstone to Buy Gramercy Property in $7.6 Billion Deal

VW CEO Given Rare U.S. Safe-Passage Deal

Ben Carlson: Bad Advice Can Be Expensive

Jeff Carter: Should The SEC and CFTC Regulate Cryptocurrency?

Jeff Miller: Why Are Stocks Stuck in Neutral?

Be sure to follow me on Twitter.

-

Q1 2018 Earnings Calendar

Posted by Eddy Elfenbein on May 6th, 2018 at 2:30 pmHere’s a list of reporting dates, Wall Street’s consensus estimates and actual reported results.

Company Ticker Date Estimate Result Torchmark TMK 18-Apr $1.45 $1.47 Alliance Data Systems ADS 19-Apr $4.23 $4.44 Danaher DHR 19-Apr $0.94 $0.99 Signature Bank SBNY 19-Apr $2.67 $2.69 Snap-On SNA 19-Apr $2.73 $2.79 Carriage Services CSV 24-Apr $0.58 $0.59 Sherwin-Williams SHW 24-Apr $3.16 $3.57 Wabtec WAB 24-Apr $0.90 $0.92 AFLAC AFL 25-Apr $0.97 $1.02 Check Point Software CHKP 25-Apr $1.28 $1.30 Stryker SYK 26-Apr $1.60 $1.68 Moody’s MCO 27-Apr $1.80 $2.02 Fiserv FISV 1-May $0.73 $0.76 Cerner CERN 2-May $0.58 $0.58 Becton, Dickinson BDX 3-May $2.63 $2.65 Church & Dwight CHD 3-May $0.61 $0.63 Continental Building Products CBPX 3-May $0.37 $0.36 Ingredion INGR 3-May $1.89 $1.94 Intercontinental Exchange ICE 3-May $0.88 $0.90 Cognizant Technology Solutions CTSH 7-May $1.06 $1.06 The Flash Crash Eight Years On

Posted by Eddy Elfenbein on May 6th, 2018 at 10:01 amWatch as the stock market completely unraveled eight years ago today.

Unemployment Rate Drops to 3.9%

Posted by Eddy Elfenbein on May 4th, 2018 at 8:47 amThis morning, the government reported that the U.S. economy created 164,000 net new jobs last month. The unemployment rate fell to 3.9%. That’s the lowest rate in 17 years. In fact, this is very close to the lowest rate since the 1960s.

Economists surveyed by Reuters had expected payroll growth of 192,000 and the jobless rate to drop by one-tenth of a percent to 4.0 percent. The official jobs tally initially showed an increase of an upwardly revised 135,000 in March.

Stock market futures moved lower following the release, while government bond yields also drifted downward.

“The expectations were a little bit elevated going into this probably just because last month’s report was a little bit weaker,” said Charlie Ripley, senior investment strategist at Allianz Investment Management. “Net-net this was a little bit softer than people were expecting. this goes into a lot of the other data that we’ve been seeing … a little bit of a soft patch.”

The closely watched average hourly earnings number rose by 4 cents, equating to a 2.6 percent annualized gain, a bit off the pace from the previous month. The average work week was unchanged at 34.1 hours.

Despite having a similar unemployment rate as April 2000 (3.8% vs. 3.9%), in order to have a similar jobs-to-population ratio as 17 years ago, April 2018 would need 11.4 million more jobs, or 17.6 million fewer people.

In the last year, average hourly earnings are up 2.56%. Here’s the unemployment rate with a red line at 3.8%.

Here’s nonfarm payrolls along with the S&P 500.

CWS Market Review – May 4, 2018

Posted by Eddy Elfenbein on May 4th, 2018 at 7:08 am“Economics is extremely useful as a form of employment for economists.”

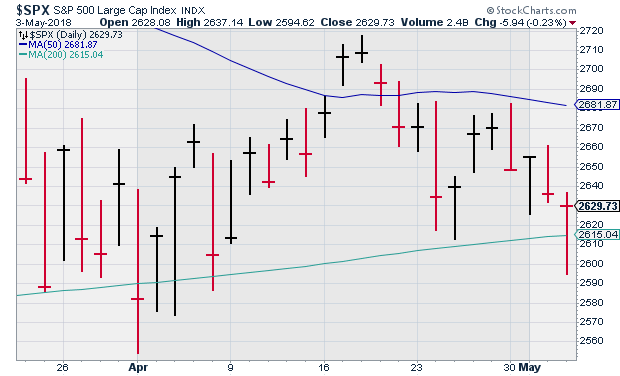

– John Kenneth GalbraithOn Thursday, the S&P 500 closed at its level lowest in nearly a month. We’ve reached an important point for the stock market. For the last ten sessions, the S&P 500 has closed in a tight range between two key levels: the 50-day moving average on the high side, and the 200-day moving average on the low side.

This won’t last. The more a support level is tested, the greater the likelihood that it will fail, and the 200-DMA is looking shaky. In fact, the S&P 500 spent some of the day on Thursday below its 200-DMA even though it eventually closed above it.

Don’t stress out about these technical levels. I just want you to be aware that the market will be choppy for this spring. The storm that hit us in in February isn’t completely gone. Fortunately, we don’t have much to fear because our Buy List stocks are much better than the average stock. So far this earnings season, we’ve had 19 Buy List earnings reports. 17 of our stocks have beaten estimates, one matched and another missed by a penny (see our calendar). This is what our strategy is about.

In this week’s issue, I’ll run down our latest batch of earnings. I’ll also preview one more coming next week, which will be our final one for this cycle. But first, I wanted to say a few words about this week’s (*shudder*) Federal Reserve meeting.

The Federal Reserve Stays on Course

The Federal Reserve met again this week, and I’ll be honest—it was a snoozer. As expected, they didn’t raise rates. The central bank made a few minor tweaks to the last statement, but it was mostly a Xerox copy.

(Side note: Some traders were in a tizzy because the Fed deleted “near-term” from their standard boilerplate, “near-term risks to the outlook appear roughly balanced.” Please. They’re way overanalyzing things.)

The big story is that the Fed appears ready to stay on the path they said they wanted to be on. Let me summarize the outlook for rate hikes at the next few Fed meetings.

June: Yes

August: No

September: Yes

November: No

December: MaaaaaybeI think it’s almost a certainty that the Fed will lift their target on the Fed funds rate to 1.75% – 2% at their June 13th meeting. Next week, we’ll get the CPI report for April. I think it will show that real short-term interest rates (meaning “adjusted for inflation”) are still negative. So as much as the Fed has moved, they’re still a long way from truly hurting the economy.

In fact, last Friday, we got our first look at Q1 GDP. The government said the economy expanded at a 2.3% rate during the first three months of the year. That’s not as strong as I’d like, but it’s about in line with how the economy has behaved during the current expansion. The jobs market is much better. In fact, we’re hearing stories of places like railroads offering hiring bonuses. Same with Disney. The important takeaway is that the economy is better and we’re not at risk of slipping into a recession soon. This is good for the market. Now let’s take a look at our earnings reports.

This Week’s Buy List Earnings Reports

It’s the busy season for earnings reports. Last Friday, shortly after I sent last week’s issue, Moody’s (MCO) released a very strong earnings report. For Q1, the credit-ratings agency earned $2.02 per share. That was well above Wall Street’s expectations of $1.80 per share. Quarterly revenue rose 16% to $1.1 billion.

As I looked at the details of the report, I could see that Moody’s business is humming along. I really like their Moody’s Analytics business as well. Moody’s also reaffirmed their full-year earnings forecast of $7.65 to $7.85 per share. Going by that, I can’t say the stock is exactly a bargain, but I’m willing to stick with Moody’s as long as the business is strong. It’s our second-biggest winner YTD. Moody’s remains a buy up to $172 per share.

We had seven more earnings reports this week. After the bell on Tuesday, it was Fiserv’s (FISV) turn to report. Wall Street was expecting 73 cents per share. In last week’s issue, I said I was expecting them to beat that. Well, I was right. For Q1, Fiserv made 76 cents per share. That’s an increase of 23% over last year.

This is basically what I was expecting. Quarterly revenue rose 4% to $1.37 billion. Their operating margin was 32.5%. That’s very good. During the quarter, Fiserv bought back 5.7 million shares of stock for $398 million. They have another 15.8 million shares left in the current authorization.

Fiserv reiterated their full EPS forecast of $3.02 to $3.15 per share. That’s an increase of 22% to 27% over last year. (The previous guidance was a pre-split level of $6.05 to $6.30 per share.) Fiserv also expects internal revenue growth of at least 4.5% this year. The stock got dinged up in Wednesday’s trading, but it’s nothing too serious. I’m keeping our Buy Below at $72 per share.

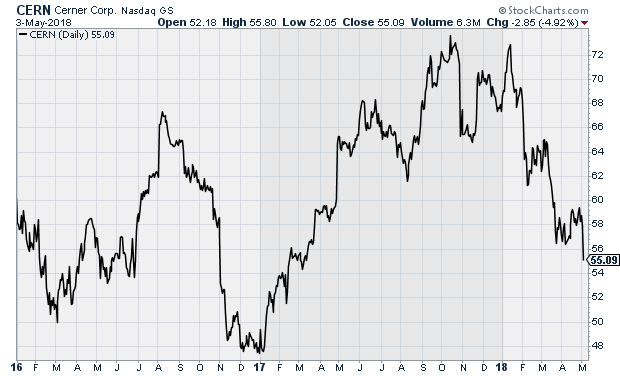

On Wednesday, Cerner (CERN) became our first dud of this earnings season. This company has done so well for so long, so it’s a surprise to see any bad news. Actually, the numbers weren’t that bad, but traders didn’t like the poor guidance. For Q1, Cerner made 58 cents per share which matched expectations. The first quarter was okay, although revenue was a bit light. Bookings rose 12% to $1.4 billion. Operating cash flow was $409 million while revenue was up 3%.

Now for guidance. For Q2, the healthcare-IT firm sees earnings coming in between 59 and 61 cents per share. They also lowered their full-year earnings range. The old range was $2.57 to $2.73 per share. The new range is $2.45 to $2.55 per share. The company blamed the lower guidance on “the delay of a large contract and a less predictable end market.” I’m not sure what that means. The stock dropped about 5% on Thursday. At one point, CERN was down over 10%. This week, I’m dropping our Buy Below on Cerner to $61 per share.

Thursday was especially busy for us with five earnings reports. Let’s start off with Becton, Dickinson (BDX). For their fiscal Q2, the company earned $2.65 per share which was two cents better than expectations. I think the addition of CR Bard was a great move for them. Becton is also raising its full-year guidance by five cents per share at both ends. BDX now sees 2018 coming in between $10.90 and $11.05 per share. That’s growth of 15% to 16.5% over last year. The company was helped by exchange rates, but they expected 12% on a currency neutral basis. I’m going to lift my Buy Below to $235 per share.

Ingredion (INGR) reported Q1 earnings of $1.94 per share. That was five cents ahead of expectations. While the numbers looked good, the CEO noted that their business was impacted by higher freight costs. Ingredion cut their 2018 range to between $7.90 and $8.20 per share. The previous range was $8.10 to $8.50. The market wasn’t terribly upset by the lower guidance. On Thursday, shares of INGR pulled back 2.4%. I’m dropping our Buy Below to $128 per share.

Not much to say about Church & Dwight (CHD). The consumer-products outfit had Q1 earnings of 63 cents per share. That was two cents better than estimates. They reaffirmed full-year guidance of $2.24 to $2.28 per share. CHD increased their expected sales growth to 9%. For Q2, they expect earnings of 46 cents per share. I’ve been puzzled with CHD’s weakness this year, but this earnings report tells me things are fine. I’m lowering our Buy Below to $61 per share.

Intercontinental Exchange (ICE) earned 90 cents per share for Q1. Wall Street had been expecting 88 cents per share. In last week’s issue, I also told you to expect a beat here. Quarterly revenues rose 5% to $1.23 billion. Despite the beat, the stock pulled back $3.00 on Thursday. I’m not at all worried. I’m keeping my Buy Below at $73 per share.

Continental Building Products (CBPX) became our only miss this earnings season. For Q1, the wallboard company made 36 cents per share which was one penny below Wall Street’s estimates. Plus, I told you expect a beat in last week’s issue.

So what happened? Nothing really. Business is going well. Weather may have a played a role, but importantly, gross margins increased. Continental had announced a price increase for January 1. As a result, a lot of customers bought before that, so results in Q1 reflected the aftermath. The most important news is that they haven’t changed their 2018 outlook. CBPX remain a buy up to $29 per share.

We only have one Buy List earnings report left. Cognizant Technology Solutions (CTSH) is due to report on Monday. For Q1, they expect earnings of at least $1.04 per share. For all of 2018, they’re looking for earnings of at least $4.53. They should be able to hit those targets. This is a very good company, and it’s currently our top performer on the Buy List. In February, Cognizant raised its quarterly dividend by 33% to 20 cents per share.

That’s it for Buy List stocks with quarters ending in March. Later this month and in early June, we’ll get earnings reports from our three Buy List stocks with quarters that end in April: Ross Stores (ROST), Hormel Foods (HRL) and Smucker (SJM).

That’s all for now. Earnings season will start to wind down next week. There’s not a lot on tap in the way of economic news. However, I’ll be very curious to see the next CPI report which comes out Thursday morning. Inflation has been largely contained, but there could be evidence of some price increases, and that will have an impact on future Fed decisions. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Morning News: May 4, 2018

Posted by Eddy Elfenbein on May 4th, 2018 at 7:05 amU.S. Wants $200 Billion Cut in China Trade Imbalance by End of 2020

Jobs Report on Friday: What to Watch For

In Birthplace of Junk, Investors See Risks After Decade of Debt

Buffett’s Berkshire Braces for ‘Wild’ Swings From New Accounting

Xerox Says CEO, Board to Stay After Agreement With Icahn, Deason Expires

Ex-Volkswagen CEO Charged With Fraud Over Diesel Emissions

Activision Blizzard Results Get Boost From In-Game Spending

Walmart Beats Amazon in $15 Billion Flipkart Battle

AT&T Says Selling DirectTV, Turner Would ‘Destroy’ Value of Time Warner Merger

Nike CEO Apologizes for Corporate Culture That Excluded Some Staff

Spotify’s Guidance Does Little to Calm Fears About Its Pricing Power

Blue Harbinger: 3 Anomalies That Beat The Market

Joshua Brown: “Active management really shines in a bear market.”

Cullen Roche: Three Things I Think I Think – China, Tesla And Weird Stuff

Be sure to follow me on Twitter.

Continental Building Products Earned 36 Cents per Share

Posted by Eddy Elfenbein on May 3rd, 2018 at 4:11 pmContinental Building Products, Inc. (NYSE:CPBX) (the “Company”), a leading manufacturer of gypsum wallboard and complementary finishing products, announced today results for the first quarter ended March 31, 2018.

Highlights of First Quarter 2018 as Compared to First Quarter 2017

Net income increased 11.6% to $13.6 million

Earnings per share increased 16.1% to $0.36

Net sales decreased 3.2% to $116.8 million on wallboard volumes down 5.4%

Gross margin increased to 25.8% compared to 25.7%

EBITDA1 decreased to $31.3 million down 4.9% compared to $33.0 million

Deployed $6.4 million in capital investments

Deployed $14.6 million to repurchase 530,600 shares of common stock

Outlook for full year 2018 unchanged“We delivered higher gross margins in the first quarter while facing a challenging operating environment, including lower volumes as expected given strong pre-buy activity in advance of our January 1, 2018 price increase and poor weather for our regions. Our ability to improve gross margins while overcoming a tightening freight and labor market reflects our sharp focus on operating discipline and our low cost highly efficient assets” stated Jay Bachmann, President and Chief Executive Officer.

Mr. Bachmann continued, “We delivered strong quarterly earnings of $0.36 per share. In addition to the benefits of tax reform and the accretive benefit of our stock repurchase plan, we believe this is a direct result of our Bison Way continuous improvement efforts and the payback we are already receiving from high-return capital projects. As we look forward to the balance of the year, we are encouraged by the pace of wallboard demand in our markets, which supports our unchanged outlook for full year 2018. At the same time, we remain focused on deploying our strong cash flow to improve our cost position through further investments in high-return capital projects while continuing to repurchase shares as a key avenue to return value to shareholders.”

First Quarter 2018 Results vs. First Quarter 2017

Wallboard sales volumes decreased to 615 million square feet (MMSF) for the first quarter 2018, compared to 650 MMSF in the prior year quarter. Net sales were down 3.2% to $116.8 million, compared to $120.6 million in the prior year quarter, primarily due to a 5.4% decrease in wallboard volumes attributable to strong customer pre-buy activity during the fourth quarter 2017 in anticipation of a previously announced January 1, 2018 price increase, partially offset by an increase in average mill net price compared to the prior year quarter.

Operating income was $20.8 million, compared to $21.7 million in the prior year quarter. This decrease was primarily attributable to lower wallboard volumes. SG&A expense was $9.4 million compared to $9.3 million in the prior year quarter, or 8.1% of net sales compared to 7.7% in the prior year quarter.

Interest expense decreased 6.7% to $2.7 million, compared to $2.9 million in the prior year quarter, reflecting higher investment income and capitalized interest partially offset by the rise in LIBOR.

Net income for the first quarter 2018 increased 11.6% to $13.6 million, or $0.36 per share, compared to $12.2 million, or $0.31 per share, in the prior year quarter. The $1.4 million increase in net income is primarily a result of the decrease in provision for income taxes under the new tax rates effective for 2018.

Balance Sheet and Cash Flow

As of March 31, 2018, the Company had cash on hand of $63.8 million and total outstanding borrowing under the term loan agreement of $270.9 million. During the first quarter 2018, the Company generated cash flows from operations of $13.7 million and deployed $6.4 million in capital investments.

In February 2018, the Company’s Board of Directors authorized an expansion of its stock repurchase program from up to $200 million to up to $300 million. The program’s expiration date was also extended from the end of 2018 to the end of 2019. During the first quarter 2018, the Company repurchased 530,600 shares of its common stock under its repurchase program at an aggregate purchase price of $14.6 million, representing 1.4% of its outstanding shares as of December 31, 2017. As of March 31, 2018, against the expanded program, the Company has repurchased $117.9 million of our common stock at an average price of $21.84 per share and had a remaining capacity of $182.1 million for future repurchases.

Forward-Looking Outlook For the Full Year 2018

SG&A is expected to be in the range of $39 – $40 million

Cost of goods sold inflation per unit is expected to be at 3% to 5% partly offset by approximately $5 million of savings from high return capital projects

Total capital expenditures are expected to be in the range of $30 – $35 million

Maintenance capital spending is expected to be approximately $15 million

High-return capital spending is expected to be in the range of $15 – $20 million

Depreciation and amortization is expected to be in the range of $43 – $46 million

Effective tax rate is expected to be in the range of 22% – 24%Four More Earnings Reports this Morning

Posted by Eddy Elfenbein on May 3rd, 2018 at 8:52 amWe have five Buy List earnings reports today, and four of them came this morning.

Becton, Dickinson (BDX) earned $2.65 per share for Q1 which was two cents better than expectations. The company is also raising its full-year guidance by five cents per share at both ends. BDX now sees 2018 coming in between $10.90 and $11.05 per share.

Ingredion (INGR) reported $1.94 per share for Q1. That was five cents ahead of expectations. They cut their 2018 range to between $7.90 and $8.20 per share. The previous range was $8.10 to $8.50.

Church & Dwight (CHD) had earnings of 63 cents per share. That was two cents better than estimates. They reaffirmed full-year guidance of $2.24 to $2.28 per share. CHD increased their expected sales growth to 9%.

Intercontinental Exchange (ICE) earned 90 cents per share. Wall Street had been expecting 88 cents per share.

Continental Building Products (CBPX) will report after the close.

Morning News: May 3, 2018

Posted by Eddy Elfenbein on May 3rd, 2018 at 7:07 amU.S. Weighs Curbs on Chinese Telecom Firms Over National-Security Concerns

Fed Holds Rates Steady, but Indicates Increases Will Continue

Amazon Threatens Seattle Over New Tax That Would Help the Homeless

Tesla’s Elon Musk Turns Conference Call Into Sparring Session

In IPO Letter, Xiaomi CEO Explains Innovation at `Honest’ Prices

Coming to a Yard Sign Near You: Warren Buffett’s Berkshire Hathaway

Fitbit Earnings: ‘Stepped Up Our Game,’ Says CFO

Apple CEO Tim Cook Is ‘Very Optimistic’ About U.S.-China Relations

Spotify’s Loss Narrows but Misses Expectations

Bitcoin Will Hit $20K in 2018. Here’s Why Ethereum Is a Better Bet, Says Reddit Cofounder

China Shunning U.S. Soybeans on Trade Tensions, Bunge CEO Says

The Cautionary Tale of Zynga’s Founder and His Potential Redemption

Michael Batnick: $100,000,000,000

Jeff Carter: The State of Private Investing

Ben Carlson: Larry Kudlow’s Strong Dollar is Easier Said Than Done & Micro Bubbles

Be sure to follow me on Twitter.

- Tweets by @EddyElfenbein

-

-

Archives

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His