-

Carriage Services Earns 59 Cents per Share

Posted by Eddy Elfenbein on April 24th, 2018 at 5:10 pmCarriage Services (CSV) just posted Q1 earnings of 59 cents per share. CEO Mel Payne said, “We got off to a good start in 2018 by setting numerous historical first quarter performance records.”

Revenue rose 7.7% to $73.4 million, and EBITDA was up 5.8%. The downside is that they’re lowering their guidance. They gave three reasons for the lower guidance; an acquisition that didn’t close in Q4 as expected, rising interest costs on their floating rate debt, and a higher share count related to convertible debt and recent increase in share price.

For the rolling four quarters ending in March 2019, Carriage expects revenue of $274 to $277 million and earnings of $1.80 to $1.85 per share. That’s a decrease of 20 cents per share at both ends. The decrease in the midpoint of the revenue range is just 2.5%.

-

Earnings from Wabtec and Sherwin-Williams

Posted by Eddy Elfenbein on April 24th, 2018 at 11:13 amWe have three Buy List earnings reports scheduled for today. Wabtec (WAB) and Sherwin-Williams (SHW) were this morning, and Carriage Services (CSV) will be after the close.

Wabtec reported Q1 earnings of 92 cents per share. That was a two-cent beat.

The best news is that Wabtec reaffirmed their full-year guidance. They expect revenue of $4.1 billion and earnings of “about” $3.80 per share, excluding restructuring costs.

The CEO said:

Our first-quarter results exceeded our expectations slightly and represent a solid start to the year. With a record backlog and the positive indicators we’re seeing in our core markets, we are well positioned to meet our financial targets in 2018. Our transit business delivered improved margins in the quarter and maintained a record backlog. In freight, we are seeing a meaningful pick-up in the aftermarket. We continue to make progress on the integration of Faiveley Transport and remain ahead of our synergy targets. As we focus on short-term performance, we are investing in our long-term growth strategies and are confident we can deliver improved earnings, margins and cash flow in the future.

The shares are up about 3.4% this morning, and they touched a nine-month high. It’s now an open secret on Wall Street that GE is looking to sell their transportation business to WAB. Expect more details soon.

The earnings report from Sherwin-Williams is a bit complicated. The company had Q1 earnings of $3.57 per share, but there are some accounting issues related to the Valspar acquisition.

The $3.57 figure includes 24 cents per share in transaction costs and 71 cents per share in “accounting impact” costs. On the plus side, Valspar added $1.08 per share in net income. The net debt charge from Valspar was 40 cents per share.

For earnings, the $3.57 per share is the number to go with, and that beat Wall Street’s consensus of $3.16 per share. That’s good news and the CEO said he expects Sherwin to increase core net sales by “mid-to-high single digits” compared with last year.

Sherwin now expects 2018 earnings of $14.95 to $15.45 per share, but that includes $3.40 to $3.50 per share related to Valspar. So without that, Sherwin see full-year EPS of $18.35 to $18.95. But this new figure includes 40 cents per share “related to an expanded customer agreement primarily impacting Valspar operations.” Wall Street had been expecting $19.14 per share.

So they beat earnings but lowered full-year guidance by 40 cents per share. The shares are currently off by about 3%.

-

The 10-Year Breaks 3%

Posted by Eddy Elfenbein on April 24th, 2018 at 11:00 amFor the first time since 2014, the 10-year broke above 3%. For some context, on July 5, 2016, the 10-year yielded 1.37%. Some folks in Europe might find this news amusing. In Germany, their 10-year is going for 0.647%.

The big phrase today is “first time since 2014,” which I just used as well. But there’s a little more to it. Back then, the 10-year barely made it to 3%. The 10-year closed on or above 3% six times in very late 2013 or very early 2014. The highest yield was 3.04%. Before that, we have to go back to July 2011.

So if we get a little more, then we can say that the yield reached a six-plus year high.

-

Morning News: April 24, 2018

Posted by Eddy Elfenbein on April 24th, 2018 at 7:42 amXi Ready to Respond as China Rattled by Trade, Debt Risks

The Chinese Car Invasion Is Coming to America

Oil Breaches $75 on Risk to Iran Deal

In Brexit, Economic Reality Competes With Nostalgia For Bygone Days

After Weeks of Chaos, U.S. Throws Aluminum Industry Lifeline

Net Neutrality Is All But Officially Dead. Now What?

Google Beat Revenue Targets But Didn’t Ease Wall Street’s Biggest Worries

Chinese Ride-Hailing Giant Didi Hits Accelerator on Talks for IPO

Sears CEO Offers to Buy Kenmore, Other Units

United Airlines CEO to Skip Bonus, Chairman Will Step Aside

Sing It From the Mountains, the iPhone Supercycle Is Dead

This Start-Up Says It Wants To Fight Poverty. A Food-Stamp Giant Is Blocking It

Nick Maggiulli: Be Careful What You Choose

Roger Nusbaum: Markets Don’t Close 4/20 On a High

Howard Lindzon: The Best Time To Invest…NOW!

Be sure to follow me on Twitter.

-

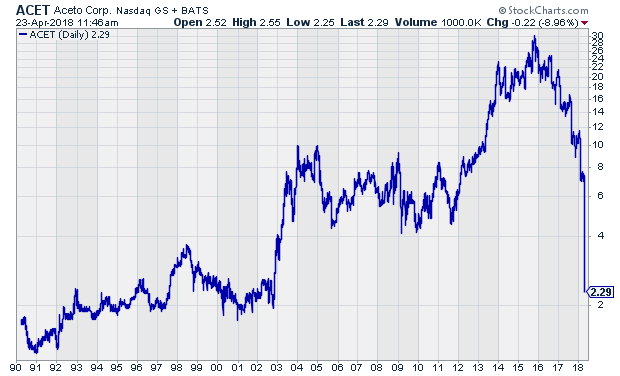

Aceto Plunges

Posted by Eddy Elfenbein on April 23rd, 2018 at 11:55 amAceto (ACET), a New York-based chemical company, was a big winner for many years, but the stock has collapsed in the last three years.

The details of Aceto’s demise are unpleasant but it’s a good reminder of an old lesson: even the strongest companies can be undone. The market changes quickly and it can be unforgiving. ACET has dropped from $30 to $2 in three years.

-

The Narrowing Yield Curve

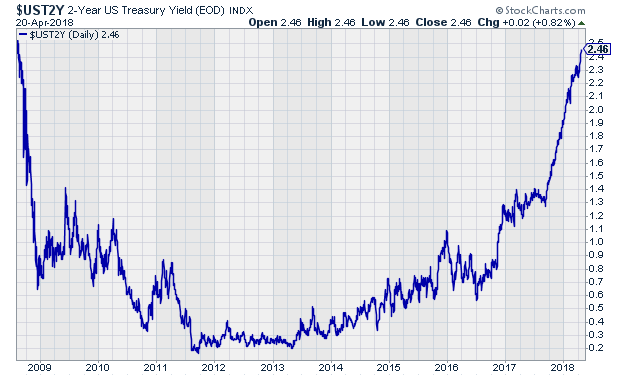

Posted by Eddy Elfenbein on April 23rd, 2018 at 8:28 amOn Friday, the one-, two- and three-year treasuries all closed at their highest yields since August 2008.

The six-month yield did the same but it came on Thursday, and the three-month’s came on Monday. The one-month yield’s long-term high came last month.

Here’s a look at the two-year yield since August 2008:

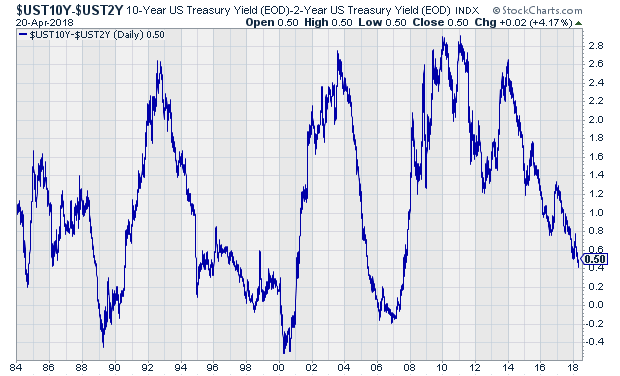

None of this is a big surprise. The early part of the yield curve is rising, and that’s what higher rates from the Fed is all about. But what about the long end? Earlier this year, the 10-year yield looked like it was about to bust through 3%…but it never could.

The 10-year recently fell below 2.75% but has now made another run at 3%. On Friday, the 10-year closed at 2.96%. The 3% line has been very difficult for the 10-year to break. The highest yield for the 10-year since mid-2011 is 3.04%. In other words, we’re very close to a multi-year high.

This week, the 2/10 spread got as low at 41 basis points. That got a lot of attention. As readers know, I’ve been a fan of the 2/10 spread for a long time, so it’s odd for me to see it get so much attention recently.

That’s why I feel like I have to remind investors that the 2/10 spread is still a long way from indicating danger. Put it this way: in the last cycle, the 2/10 spread hit 41 basis points in May 2005. That was 2-1/2 years before the recession started. Remember, a negative 2/10 is not a tripwire. It’s a warning signal.

-

Morning News: April 23, 2018

Posted by Eddy Elfenbein on April 23rd, 2018 at 7:05 amThe SEC Wants Wall Street to Treat Clients Better. What’s at Stake?

Stocks Stumble as U.S. Yields Near the 3% Barrier

Oil Holds Near $68 as Rising U.S. Drilling Counters OPEC Curbs

How Windmills as Wide as Jumbo Jets Are Making Clean Energy Mainstream

Zelle, the Banks’ Answer to Venmo, Proves Vulnerable to Fraud

Tencent Music Plans IPO; Valuation Could Exceed $25 Billion

Facebook Faces Defamation Charges Over Fake Ads

Walmart Closes In On India’s Flipkart

Akorn Slumps After Fresenius Abandons $4.3 Billion Takeover Bid

China’s Tech Stocks Struggle Under ZTE Ban, IPhone Sales

Hasbro Blames Toys ‘R’ Us as Sales Sink

Korean Air Chairman Fires Two Daughters Over Rage Incidents

Joshua Brown: The Best and Worst State Economies

Jeff Miller: The Costly Quest for Fresh Fears

Jeff Carter: Innovation Theatre

Be sure to follow me on Twitter.

-

CWS Market Review – April 20, 2018

Posted by Eddy Elfenbein on April 20th, 2018 at 7:08 am“To achieve satisfactory investment results is easier than most people realize; to achieve superior results is harder than it looks.” – Benjamin Graham

Earnings season is upon us, and so far, things are looking good. We’ve had five Buy List earnings reports this week, and all five beat Wall Street’s consensus. You can always check out our latest Earnings Calendar.

In this issue, I’ll run though all of our reports. I’ll also profile seven more earnings reports coming our way next week. Remember, things can get much more volatile for individual stocks after their earnings reports, so don’t be scared by a little more action.

Fortunately, the stock market has been more buoyant recently. At one point, the S&P 500 rallied eight times in 11 sessions, and on Wednesday, the index closed at a four-week high. But don’t be complacent. I still think there’s a good chance the market will test the lows.

If you’re into numbers, I can remind you that the closing low from February 8 was 2,581.00, and the one from April 2 was 2,581.88. That’s how close we came to a new low. This tells me that the bears haven’t been scared off. More on that later. For now, let’s look at some earnings.

This Week’s Five Buy List Earnings Reports

We had five of our Buy List stocks report earnings this week. I’m happy to say that all five beat estimates. However, not all five got a lift from the news. Let’s run through the reports.

Torchmark (TMK) led off earnings season for us after the bell on Wednesday. The insurance company reported Q1 earnings of $1.47 per share. That was two cents more than estimates. For last year’s Q1, Torchmark made $1.15 per share. This one is as steady as they come.

One of the key stats for Torchmark is Return on Equity that excludes unrealized gains on fixed income. That’s kind of a mouthful, but it’s one of the best ways to measure the company’s performance. For Q1, this metric came in at 14.6%, which is quite good. The company is experiencing healthy growth across its different business units.

In the earnings release, Torchmark said they see 2018 EPS coming in between $5.93 and $6.07 per share. That’s probably a tad low. I think TMK can hit $6.10 per share, but I won’t quibble with their guidance; we’re still early in the year. The guidance implies the stock is going for a decent valuation. Shares of TMK gained 1.8% in Thursday’s trading. I’m pleased with this news, and I’m raising our Buy Below on Torchmark to $91 per share.

On Thursday morning, we got four more Buy List earnings reports. I had been a little nervous coming into the earnings report for Alliance Data Systems (ADS). The stock has plunged since the last earnings report. Alliance reported Q1 core earnings of $4.44 per share. The good news is that that easily topped Wall Street’s estimate of $4.23 per share. The bad news is that the estimate had been severely pared back over the last several weeks. Not too long ago, the Street had been expecting over $5.10 per share for Q1. Quarterly revenue rose to $1.88 billion which was a little bit below forecasts.

Alliance’s CEO, Ed Heffernan, said, “This quarter’s pro-forma revenue growth of 4 percent and core EPS growth of 13 percent should reflect our softest quarter of the year. Specifically, higher reserve levels required to cover the transitory impacts of the internal recovery investment was an approximate $0.60 hit to core EPS for the first quarter. Moving forward, recovery rates should move in our favor.”

ADS reiterated its full-year guidance of $22.50 to $23 per share with revenue of $8.35 billion. I was pleased to see that. Still, the shares dropped 4.5% at Thursday’s open, but then they regained their composure later in the day and only closed off by 0.9%. Just to be safe, I’m dropping my Buy Below down to $232 per share.

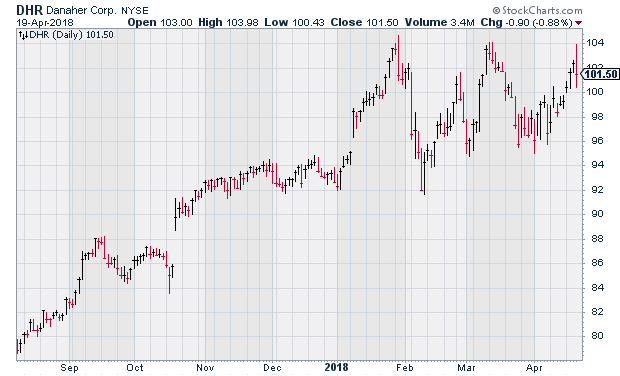

Danaher (DHR) had a very good report for Q1. The company made 99 cents per share. If you recall, they initially provided Q1 guidance of 90 to 93 cents per share. DHR later said they’ll beat that thanks to strong results from their Life Sciences and Diagnostics platforms, “specifically at Cepheid.”

For Q2, Danaher sees earnings of $1.07 to $1.10 per share. Wall Street had been expecting $1.08 per share. The best news is that Danaher raised its full-year guidance. The old range was $4.25 to $4.35 per share. The new range is $4.38 to $4.45. Last year, DHR made $4.03 per share. Danaher remains a buy up to $105 per share.

Also on Thursday, Signature Bank (SBNY) reported Q1 earnings of $2.69 per share. That was two cents better than estimates. Signature’s results for Q1 are a bit distorted because they took a big write-down for their taxi medallion loans.

Let’s look at some metrics. Deposits rose 4.1% to $34.82 billion. Net interest margin was 3.01%. Thanks to the medallion loans, Signature’s efficiency ratio rose to 42.2%. This measures a bank’s net interest expense as a share of its total income. The lower, the better.

Excluding the medallion loans, Signature is doing just fine. The problem for the last few quarters was that that’s a hard thing to exclude. Fortunately, SBNY is moving beyond that. I still think SBNY can earn $11 per share this year. The shares lost 3.1% on Thursday. I still like SBNY. This week, I’m dropping my Buy Below to $142 per share.

Our big winner this week is Snap-on (SNA). On Thursday, the company reported Q1 earnings of $2.79 per share. I’ve been concerned by weakness in their tool group, and that’s still an issue. For Q1, organic sales rose by just 0.8%. The good news is that their other business units are picking up the slack.

I think this is a case of Wall Street expecting the worst. When the worst didn’t come, the stock rallied. By the closing bell, shares of SNA had gained 6.2%. It was the second-best performer in the S&P 500 for the day. I’m keeping our Buy Below at $167 per share. Now let’s take a look at some of next week’s reports.

Seven Buy List Earnings Reports Next Week

Next week is going to be another crowded week for earnings. Here’s a rundown.

On Tuesday, April 24, three Buy List stocks are ready to report. Carriage Services (CSV) may be a dark-horse winner for us this year. The stock is already our third-best performer so far. The funeral-home company had a rough year in 2017, but things seem to have turned the corner. The last earnings report was a good one. Carriage also increased its earnings guidance.

Only two analysts on Wall Street follow the stock, so I really can’t say there’s an earnings consensus. I’m expecting Q1 earnings around 50 to 52 cents per share. The stock is going for an attractive valuation.

For Q4, Sherwin-Williams (SHW) gave us an earnings dud. I’m hoping this won’t become a habit. The problem is that they’re still adjusting to their big merger with Valspar. Some headaches are to be expected. In the long run, this deal should pay off. For 2018, Sherwin expects earnings in the range of $16.05 to $16.45 per share. Wall Street is looking for $3.16 per share for Q1.

Wabtec (WAB) had a strange time during its last earnings report. The shares dropped when the company released preliminary results, but then they snapped back just before the actual results. For Q1, Wabtec said they’re expecting similar results as Q4. Since they made 90 cents per share for Q4, I’m assuming 90 cents or so for Q1. For all of 2018, Wabtec is looking for earnings of “about” $3.80 per share. The stock has been acting better in recent weeks.

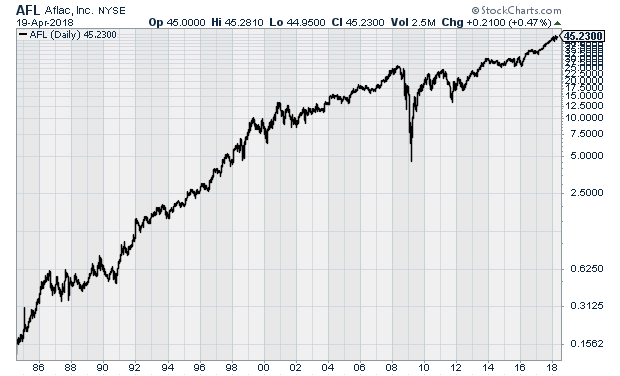

On Wednesday, AFLAC (AFL) is due to report Q1 earnings. I’m a big fan of the duck stock. Check out this 34-year log chart of AFLAC.

For 2018, AFLAC is looking for earnings to range between $3.73 and $3.88 per share ($7.45 and $7.75 pre-split). That assumes a yen/dollar rate of 112.16 which was the average for 2017. For Q1, Wall Street is looking for earnings of 97 cents per share.

Also on Wednesday, Check Point Software (CHKP) is due to report. The company had a very good report three months ago. For Q1, Check Point sees earnings between $1.25 and $1.30 per share on revenues of $440 to $460 million. For the full year, they see EPS of $5.50 to $5.90 on revenue of $1.9 to $2.0 billion.

On Thursday, Stryker (SYK) will report earnings. They previously said they expect Q1 earnings between $1.57 and $1.62 per share. For the full year, Stryker expects earnings of $7.07 to $7.17 per share. The stock has been holding up well. SYK is within 3% of its all-time high. The company has raised its dividend every year since 1993.

Moody’s (MCO) is set to report on Friday, April 27. The credit-ratings agency is our second-best performer this year with a gain of 12.3%. I like this company a lot. They’re looking for 2018 earnings of $7.65 to $7.85 per share. They made $6.07 per share in 2017. For Q1, Wall Street expects earnings of $1.80 per share.

That’s all for now. Still more earnings reports are to come next week. We’ll also get a few key economic reports. On Monday will be existing-home sales. Then on Tuesday, we’ll see new-home sales. On Friday, we’ll get our first look at Q1 GDP. The last three quarters have been close to 3% growth. Let’s see if that trend continues. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Syndication Partners

I’ve teamed up with Investors Alley to feature some of their content. I think they have really good stuff. Check it out!

3 Stocks for Profits from People Playing Video Games All Day

According to PricewaterhouseCooper (PwC), the global e-sports market was worth $327 million in 2016. One reason for its smallish size compared to say the NFL is that e-sports is a collection of different game titles across different game genres, with different intellectual property holders that, to date, have not bargained together for TV (and streaming) rights and sponsorship deals.

But now e-sports is moving into the ‘major league’ of sports. They will be added as a medal event in the 2022 Asian Games. That’s not surprising considering that South Korea is the hot spot for these sports, with other Asian countries also joining in. The backers of e-sports are pushing too for it to be added as an official event in future Olympics too.

Any future Olympics boost will only add to the growth already occurring. PwC estimates that the e-sports market will expand at a compound annual growth rate (CAGR) of 21.7% through 2021 into an $874 million market. Other forecasts are even more bullish. For example, the Dutch research firm Newzoo says e-sports will be a $1.6 billion industry by 2021.

Whatever forecast you believe, the bottom line is that the e-sports industry is growing in leaps and bounds. Here are three to stocks to buy from companies profiting off people playing video games all day.

Buy These 2 Stocks Benefitting from Trump’s Tax Reform Law

With this year’s tax filing deadline date just past, it’s a good as time as any to take a look at a few special situations whose stock prices were hit because of recent changes in tax policies.

The first company I want to tell you about is one that has become a real life example of the law of unintended consequences…

Congress changed the way American corporations are taxed on their overseas earnings. Previously, firms were taxed at the 35% rate. But most companies avoided that by booking their income overseas and then keeping the money there.

So Congress came up with GILTI (Global Intangible Low-Taxed Income), which was set at 10.5%. Its main target was the tech and pharma companies that transferred their trademarks and patents overseas to avoid paying tax on them.

But this new tax intended to tax overseas income earned by U.S. technology and pharmaceutical firms and their trademarks and patents has hit closer to home. Click here to see which stocks are impacted.

-

Morning News: April 20, 2018

Posted by Eddy Elfenbein on April 20th, 2018 at 7:04 amCrude Set for Weekly Gain as Saudis Flag Need for More Spending

U.S. Sorghum Armada U-turns At Sea After China Tariffs

Trade Wars Don’t Faze This U.S.-China Investor

Hedge Fund Titans Pull Money From Funds to Pay Massive Tax Bills

American Hustle: ZTE’s Surprise U.S. Success, Now Under Threat

Wells Fargo Dropped by Teachers Union Over Ties to Gun Industry

What General Electric Shareholders Should Do Now

AT&T Chief Hits Foes of Time Warner Deal

Chipmakers’ Rout Widens After TSMC Ignites Smartphone Fears

In Vietnam, A Mega Casino Rises With the Help of a Macau Junket Company

‘Fearless Girl’ Will Be Moving to NYSE After Spending a Year Staring Down ‘Charging Bull’

Barclays Chief Executive Staley Fined Over Whistle-Blower Scandal

Blue Harbinger: How Do You Filter Out Noisy Trade Signals?

Ben Carlson: The Tyranny of Benchmarking

Michael Batnick: This Tells You Nothing

Be sure to follow me on Twitter.

-

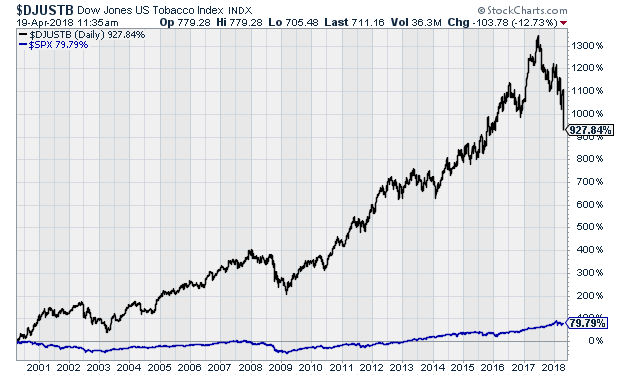

“MARGIN CALL FOR PHILIP MORRIS!!!!”

Posted by Eddy Elfenbein on April 19th, 2018 at 11:38 amTobacco stocks are getting smoked today. Philip Morris is down about 16%, but this comes after years of creaming the market.

Here’s the Dow Jones U.S. Tobacco Index in black. It’s been so strong that the S&P 500, the blue line, looks flat in comparison.

- Tweets by @EddyElfenbein

-

-

Archives

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His