-

CWS Market Review – March 2, 2018

Posted by Eddy Elfenbein on March 2nd, 2018 at 7:05 am“Your margin is my opportunity.” – Jeff Bezos

The S&P 500 went 94 straight days without a 1% day either up or down. Now it’s happened 15 times in the last 24 sessions including the last five in a row (first two, up; last three, not up).

I cautioned investors that the ruckus hasn’t yet passed. Three weeks ago, the S&P 500 bounced off its 200-day moving average, and it will likely “test” that support level again. Financial markets don’t walk away from a mess like we had so easily. Fear of the market gods is clean, enduring forever.

Let’s remember that the broad economic climate is quite good. This week’s initial jobless claims report showed figures at their lowest level since the 1960s. Thursday’s ISM Manufacturing report was the best one in 13 years, and consumer confidence is now at a 17-year high.

So what’s bugging Wall Street? This week, investors got a bit spooked by fears of a trade war. President Trump proposed steep tariffs on steel and aluminum. I thought it was interesting that on Thursday, stocks of big steel consumers like Ford and GM fell hard. Our own Snap-on (SNA) was down 3.3%.

Frankly, I’m skeptical that these plans will be implemented. Within the business community, the opposition to steep tariffs is nearly overwhelming. Also, a lot of the big steel exporters are good friends of the United States. Perhaps President Trump is sending a message to China. As usual, I’ll steer clear of the politics, but I’ll comment on the policy’s impact. Wall Street will not like a trade war.

I wanted to do something a bit different this issue. I recently asked readers for some feedback on the newsletter, and I got very constructive suggestions. A number of readers wanted to hear more in-depth reasons for why I like a particular stock.

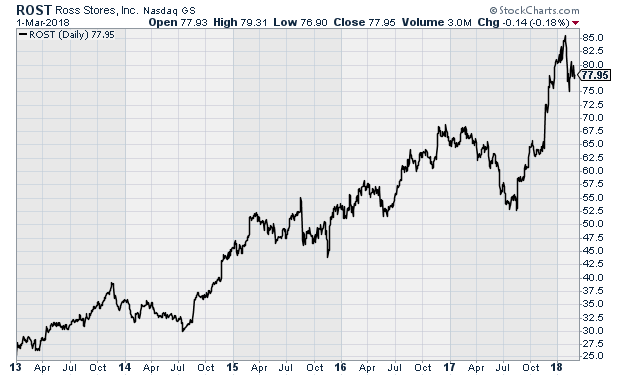

Since there wasn’t a whole lot of news this week (Jay Powell made some hawkish comments on interest rates on Capitol Hill), instead I thought I would focus on one our favorite Buy List stocks: Ross Stores (ROST). This is a good time to highlight Ross because the deep discounter will report fiscal Q4 earnings after the close on Tuesday.

Why I Like Ross Stores

I like Ross Stores a lot. This is the sixth year the company has been on our Buy List. We added the stock at the beginning of 2013 when it was going for $27 per share (that’s adjusting for one 2-for-1 split in 2015). Now it’s at $78 per share. The stock is up 188% for us in a little over five years. It’s had a few nasty dips along the way, but I’m glad we’ve stuck with it.

Our return has been even better when we include dividends. When we added Ross, the quarterly dividend was 8.5 cents per share. Now it’s 16 cents per share, and they’ll probably raise it again on Tuesday.

The upcoming earnings report will be for ROST’s fiscal fourth quarter. I have to explain that many retailers, Ross included, like to use a January fiscal year so they don’t have to break up the holiday shopping season between quarters. Also like other retailers, Ross prefers to use a 13-week reporting period rather than a three-month one. Thanks to Pope Gregory XIII, this means that every so often Ross will have a 14-week quarter. As luck would have it, this past Q4 was a 14-weeker.

The important thing to understand about Ross’s business is that they’re a retailer. That means it’s a low-margin business. In fact, it’s even more so for Ross because they compete as a deep-discount alternative to other stores. There are several ways a business can implement its competitive advantage. Some companies offer something that no else does. In Ross’s case, they’re competitive on price. What Ross tries to do is squeeze every penny out of its costs and pass the savings to its customer base.

When we look at any business for an investment opportunity, we have to ask, “What makes you different? What’s so special about you?” What impresses me about Ross is how they’re able to maintain relatively high profit margins compared with similar businesses.

Let’s look at some financials. I promise not to get too mathy. Last fiscal year, Ross Stores had total sales of $12.7 billion. Major expenses fall into two categories: the cost of the stuff they sell and the cost of running the business. What’s left is the operating profit. For Ross, last year saw an operating profit of $1.9 billion with an operating profit margin of 14%. For a retailer in Ross’s business, that’s quite good. Think of it this way. For every $1 of sales, 71 cents went to the cost of the clothes, and 15 cents went to running the store. They’re left with 14 cents.

There are two items left. The company had interest expenses on their borrowing of $16.5 million. That’s tiny—about 0.13% of sales. Finally, there’s Uncle Sam. Last year, Ross paid about 37% of its pre-tax income to the government. This gives us a net income of $1.1 billion and a net margin of 8.7% which works out to $2.83 per share.

(As a side note, the recent tax reform helps domestic retailers more than other businesses. Large tech companies can use all sorts of fancy methods to shovel their cash around the world. With retailing, that option is very limited. )

Here’s an important reason why I like Ross. Their net profit margin is actually higher than most apparel retailers including The Gap, Nordstrom and Urban Outfitters. Ross’s margins are also higher than TJX’s, their closest rival. Strong relative margins tell us two key things. One is that there’s a good chance of superior management. Secondly, it means the company has pricing power. Even with Ross’s low prices, they can go lower if they need to. (Note this week’s epigraph, courtesy of Mr. Bezos.)

The thing about the retailing business is that it’s more accurately termed the inventory-management business. Next time you’re in a Walmart, try to find an empty shelf. You’ll probably find Bigfoot first. That’s what efficient retailing is all about—keeping the merchandise flowing in and quickly flowing out. Ross does it as well as anybody.

Ross Stores Doesn’t Compete Directly with Amazon

Whenever we talk about retailing, the discussion always turns to Amazon. This is a key point about Ross Stores, and it’s something many critics don’t get: Ross doesn’t compete against Amazon. Ross is not at all like Borders or Barnes & Noble.

Let me explain the difference. Ross’s customers enjoy going to the physical stores. Many of their devoted fans go more than once a week. They enjoy the “treasure hunt” experience of shopping in the store, and you can’t easily recreate that online.

Another benefit of Ross’s business is what’s called “packaway.” This means the company can buy off-season stuff for cheap and lock it away for later. Other retailers can’t do that so easily. Let’s say the winter is unusually warm. That’s no big deal for Ross. They’ll just save their inventory for a later day. Other retailers are expected to always have current fashions. Ross can play by different rules because they’re playing a different game.

TJX is a good business, but I happen to like Ross more. They’re similar in many ways, but TJX has some stores outside the U.S. while Ross does not. TJX also sells some upscale items that you won’t find at Ross.

By the way, I should touch on an important point. Some investors are skittish about investing in a business that caters to lower-income consumers. Please, don’t let that bother you at all. Lower-income consumers are often one of the best, and most loyal, customer groups. Ross’s fans love the company, and there’s nothing wrong with giving the people what they want at a fair price. Sure, Tiffany draws some first-class shoppers, but around here, we care about stocks, and ROST has creamed TIF.

What to Expect on Tuesday

For the first three quarters of this fiscal year, Ross’s sales are up 7.6% while net income is up 11.6%. The higher net margin was helped by lower interest expenses. Thanks to fewer shares outstanding, Ross’s earnings-per-share is up by 14.6% so far this year. The company is gobbling up its own shares at an impressive rate.

In November, Ross said they expect Q4 earnings (remember this is for 14 weeks) of 88 to 92 cents per share. For the entire year, that works out to $3.24 to $3.28 per share. Ross estimates that the extra week works out to an extra eight cents per share. Here’s my take: The Q4 estimate is probably a little low, but not by much. I’ll say they made about 95 cents per share, give or take.

More importantly, on Tuesday, Ross will probably give a forecast for the coming fiscal year. I’ll caution you that Ross loves to lowball its initial estimates. That means they can raise it later on. Their first estimate for last year was $3.02 to $3.15 per share, which they later raised three times. Realistically, Ross should be able to earn around $4 per share this year. However, I expect them to go on the record with something like $3.75 to $3.85 per share. I’ll also be curious to hear about the impact of tax reform.

What about the quarterly dividend? It’s currently at 16 cents per share. I think they’ll raise it to 20 cents per share. That will give them an even 80 cents for the year which is around 20% of their profits.

Last August, when it was at $55 per share, I said Ross was “a good value.” Now it’s at $78 per share. It’s not the bargain it was, but it’s still worth owning. Ross is going for 19.5 times forward earnings which isn’t unreasonable especially considering tax reform, a higher dividend and the improved economy. Ross Stores is a buy up to $81 per share.

That’s all for now. There are some key economic reports coming next week. On Monday, we’ll get the ISM non-manufacturing report. Wednesday is the ADP payroll report. Then Friday is jobs day. The Labor Department will release the employment report for February. Wall Street estimates that 200,000 new jobs were created. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Syndication Partners

I’ve teamed up with Investors Alley to feature some of their content. I think they have really good stuff. Check it out!

How to Profit from the Death of Oil

In the latest annual energy outlook from BP PLC (NYSE: BP), it was the first time the company forecast oil demand would eventually peak and then steadily decline. BP put the date for peak oil demand in the late 2030s.

And the cause is one I’ve told you about quite often in my articles – the rise of electric vehicles. BP said there would be 300 million electric vehicles on the road by 2040, up from about 3 million today. BP says electric vehicles will account for only 15% of the roughly 3 billion cars on the road in 2040. But they will account for 30% of all passenger car transportation, as measured by distance traveled, because so many of them will be shared vehicles, à la Uber.

BP’s outlook also envisaged renewable power growing from just 4% of global energy consumption today to 14% in 2040.

Add all of that up and you can surmise that a lot of changes are ahead for the oil industry. Yet only some of the world’s major oil companies are preparing for what the future will hold.

How to Get Your Cut of Apple’s Money Coming Back to the US

Financial risks can seemingly come out of nowhere. Think about how many on Wall Street were caught off guard by the 2008-09 financial crisis or even the volatility of a few weeks ago. Yet the potential risk emanating from the packaging of bad mortgages was in plain sight, but ignored.

Today, there is another financial risk lurking in plain sight. It lies in the vast overseas holdings of technology giants like Apple, Alphabet, Microsoft and many others. I discussed this topic to my subscribers in the October issue of Growth Stock Advisor. But since there is so much misunderstanding about the roughly $1 trillion (or possibly as high as $2 trillion) in funds held overseas by U.S. multinationals, I wanted to clear it up for you.

I know there is much misunderstanding about this subject just from gleaning the comments section on several recent articles published by The Wall Street Journal. Apparently, Americans are under the impression that this $1 trillion is just sitting in bank accounts overseas and that both the overseas banks and host countries don’t want to lose control of this money. Nothing could be further from the truth. Let me explain…

-

Morning News: March 2, 2018

Posted by Eddy Elfenbein on March 2nd, 2018 at 7:02 amTrump Says Trade Wars Are ‘Good, and Easy to Win’

Trade Worries Hit Stocks in Europe and Asia

Bank of England Governor Mark Carney: Bitcoin is Heading For a ‘Pretty Brutal Reckoning’

The Saudis Can’t Just Throw Their Bond Market Weight Around

Equifax Clears Q4 Earnings Bar Despite More Bad News

Twitter CEO Jack Dorsey Gives Blunt Assessment of the Company’s Failures

Toyota Announces New Company Devoted to Self-Driving Cars

China’s HNA Group to Sell Stake in Hilton Spinoff Park Hotels & Resorts

REI Halts Orders From Vista Outdoor Over Its Response to Parkland Shooting

Smith & Wesson Gun Sales Are in Free Fall

DoorDash Raises $535 Million To Fuel Food Delivery War

Krueger & Catalano: Mailbox Money Math

Mark Hines: Do You Trade the 50-Day Moving Average?

Jeff Carter: Why ICO Petitions Came From the SEC & Pay Your Bitcoin Taxes, Don’t Whine About It

Howard Lindzon: There is No Such Thing as an Overnight Success…The Story of Ring

Be sure to follow me on Twitter.

-

Unemployment Claims Lowest Since the 1960s

Posted by Eddy Elfenbein on March 1st, 2018 at 12:00 pmThis morning the unemployment claims report came in at 210,000. This number tends to bounce around a lot so economists prefer to look at the four-week moving average. That number is down to 220,500 which is the lowest since December 27, 1969. For the raw number, it’s the lowest since December 6, 1969.

(Yeah, I know. I said lowest since the 1960s, but I’m technically right.)

We also learned that the ISM manufacturing index for February rose to 60.8. Expectations were for 58.6. That’s the highest since 2004.

I like the ISM report because it comes out on the first business day of the month. The day after the GDP report we get the personal income and spending report for the prior month. Since the GDP was revised yesterday, this morning we get personal income and spending for January. Personal income rose by 0.4% in January while spending increased by 0.2%.

-

Morning News: March 1, 2018

Posted by Eddy Elfenbein on March 1st, 2018 at 6:59 amWhy an Unpleasant Inflation Surprise Could Be Coming

Trump Expected to Announce Stiff Steel, Aluminum Tariffs

Powell Shoots for Soft Landing That’s Eluded Seasoned Fed Chiefs

Exxon Abandons Russian Projects Brokered by Tillerson

Walmart, Dick’s Say They Will Stop Selling Guns to Those Under 21

Lowe’s Update: After 25% Surge, Discount To Home Depot Narrowed Dramatically

Best Buy to Close Mobile-Phone Stores

Spotify Is Getting Paid to Save the Music Industry

World’s Biggest Ad Agency Suffers Worst Stock Drop Since 1999

Cryptocurrency Firms Targeted in SEC Probe

Is Bitcoin a Waste of Electricity, or Something Worse?

Bill Ackman Surrenders in His Five-Year War Against Herbalife

Cullen Roche: Tremors Was a Very Bad Movie

Roger Nusbaum: Game Planning Another Lost Decade

Ben Carlson: Questions For the Next Bear Market & The Closet Indexer

Be sure to follow me on Twitter.

-

The MOAT ETF

Posted by Eddy Elfenbein on February 28th, 2018 at 3:13 pmThere’s an ETF which focuses on competitive advantages, otherwise known as moats. The VanEck Vectors Morningstar Wide Moat ETF has the symbol MOAT.

I don’t own any shares in it but their strategy is close to what we do with our Buy List. MOAT currently has 44 stocks while we have just 25.

Here are the MOAT holdings as of January 31:

AMAZON AMZN

TWENTY-FIRST CENTURY FOX FOXA

LOWE’S LOW

EXPRESS SCRIPTS ESRX

AMERISOURCEBERGEN ABC

VEEVA SYSTEMS VEEV

SALESFORCE.COM CRM

EMERSON ELECTRIC EMR

UNITED TECHNOLOGIES UTX

VISA V

CARDINAL HEALTH CAH

VF VFC

BRISTOL-MYER SQB BMY

TRANSDIGM GROUP TDG

WELLS FARGO WFC

WALT DISNEY DIS

WESTERN UNION WU

L BRANDS INC LTD

PFIZER INC PFE

MONDELEZ INTERNATIONAL INC-A MDLZ

MONSANTO CO MON

MCKESSON CORP MCK

AMGEN INC AMGN

ZIMMER HOLDINGS INC ZMH

STARBUCKS CORP SBUX

MEDTRONIC PLC MDT

ELI LILLY & CO LLY

MERCK & CO. INC. MRK

STERICYCLE INC SRCL

COMPASS MINERALS INTERNATION CMP

BIOGEN IDEC INC BIIB

CVS CAREMARK COR CVS

ALLERGAN PLC AGN

GENERAL ELECTRIC CO GE

SCHWAB (CHARLES) SCHW

CBRE GROUP INC – A CBG

MICROSOFT CORP MSFT

GUIDEWIRE SOFTWARE INC GWRE

NIKE NKE

BANK OF NEW YORK MELLON BK

GILEAD SCIENCES GILD

WILEY (JOHN) & SONS JW-A

MICROCHIP TECHNOLOGY MCHP

POLARIS INDUSTRIES PII

AMERICAN EXPRESS AXP

PATTERSON PDCOI can’t say I like all these names, but I see several former Buy Listers here. It’s interesting how similar strategies can yield different names.

I couldn’t find a precise methodology for the fund. Judging what’s a long-lasting competitive advantage must involve some human guesswork.

-

Morning News: February 28, 2018

Posted by Eddy Elfenbein on February 28th, 2018 at 5:22 amStock Selloff Widens After Powell Boosts Expectations of Rate Rises

Senate Democrats Push for Support to Reinstate Net Neutrality

Amazon Acquires Ring, Maker of Video Doorbells

Papa John’s Is No Longer the NFL’s Official Pizza

Takata Airbag Scandal: Australia Recalls 2.3 Million Cars

Baidu’s Netflix-Style App Marks Bumper Year for China Tech IPOs

Comcast’s Roberts Has Anti-Murdoch Card to Play in Bid for Sky

Bill Gates Says Cryptocurrency is `A Rare Technology That Has Caused Deaths in a Fairly Direct Way’

Macy’s Just Confirmed the End of Department Stores as We Know Them

Weight Watchers Looking to Expand Beyond Dieting

How Defective Guns Became the Only Product That Can’t Be Recalled

In N.R.A. Fight, Delta Finds There Is No Neutral Ground

Cullen Roche: Here’s a (Not So) Pretty Picture – Buffett vs the S&P 500

Joshua Brown: Where the S&P 500 Will Spend Their Cash This Year

Michael Batnick: Why Doesn’t More Money Make Us Happy?

Be sure to follow me on Twitter.

-

Four Rate Hikes this Year

Posted by Eddy Elfenbein on February 27th, 2018 at 7:27 pmAccording to the futures market, the odds of the Fed raising interest rates four times this year is 33.5%. That’s up from 25% a week ago. In my opinion, it’s closer to 5%. Alas, I’m not on the FOMC.

I also wanted to mention that HEICO (HEI), a former Buy List all-star, reported earnings after today’s close. I like this stock a lot but I don’t like the price.

As usual, the earnings report was very good. Q1 sales rose 18% to $404.4 million, and EPS hit 45 cents per share. That’s five cents more than estimates. Last month, HEICO also split its stock 5-for-4.

HEICO is raising its full-year forecast. Before, they saw net sales and income rising by 10% to 12%. Now they see net sales rising by 12% to 14% and net income rising by 30% to 32%. That’s thanks to tax reform.

HEI is up 3.1% after hours. I would love to have HEICO back on the Buy List, but it’s way too pricey.

-

“A 40% Chance”

Posted by Eddy Elfenbein on February 27th, 2018 at 11:13 amRolfe Winkler and Justin Lahart have a biting piece in today’s WSJ on how market gurus go about making their claims non-falsifiable.

This is one of my pet peeves. You can see my Buy List all the time. My track record goes back more than a decade. Yet there are lots of famous market gurus who weasel their way out of one terrible call after another. Peter Schiff and Nouriel Roubini are prime examples.

Winkler and Lahart say that when in doubt, claim that your forecast had a 40% probability. That’s the sweet spot. If you’re right, you’re a genius. If you’re wrong, then you never said it was absolutely going to happen.

The nice thing about 40% is that you never have to say you were wrong, says Peter Tchir, a market strategist at Academy Securities. Say you predict the Dow Jones Industrial Average has a 40% chance of hitting 30000 before year-end.

“Get it right and you can say ‘See, I was telling everyone it could happen,’ ” he says. “Get it wrong and you can weasel your way out: ‘I didn’t say it was likely, I just said it was a strong possibility.’ ”

(…)

“Pundits and gurus master the art of going out on a limb without going out on limb,” says Philip Tetlock, a professor at the University of Pennsylvania who has made a career analyzing which people forecast well, and why. One of his pet peeves is how gurus use vague terms like “distinct possibility” instead of percentage odds when they describe probabilities. That makes it easy to wiggle out of, or take credit for a forecast, since it isn’t clear at all what a distinct possibility is.

But one drawback of percentage odds, Mr. Tetlock says, is that people are often unclear on what they actually mean.

(…)

Courageous contrarian calls are the best way forecasters capture the public’s attention, and get television time. New York University Professor Nouriel Roubini was dubbed “ Dr. Doom ” for correctly predicting the financial crisis. Then in 2010 he projected a 40% chance of a “double-dip recession” in the U.S. It didn’t happen.

Mr. Roubini says he doesn’t remember the projection, but that he takes pride in sticking his neck out, as with his latest call that Bitcoin is the biggest bubble in history and will go to zero.

“I would not rule out that I’ve committed the sin of the 40% rule,” said Prof. Roubini. “Everybody has done so.”

-

Powell Speaks and Durable Goods

Posted by Eddy Elfenbein on February 27th, 2018 at 11:01 amWe had two key economic reports this morning. The Case-Shiller Index said that home prices rose 6.3% in 2017. Also, orders for durable goods fell 3.7% compared with expectations of a 2% drop.

Orders for non-defense capital goods excluding aircraft, a closely watched proxy for business spending plans, dropped 0.2 percent last month after declining 0.6 percent in December.

That was the first back-to-back drop in these so-called core capital goods orders since May 2016. Economists polled by Reuters had forecast these orders rising 0.5 percent last month. Orders increased 8.0 percent on a year-on-year basis.

Shipments of core capital goods edged up 0.1 percent after an upwardly revised 0.7 percent rise in December. Core capital goods shipments are used to calculate equipment spending in the government’s gross domestic product measurement. They were previously reported to have increased 0.4 percent in December.

We also learned this morning that consumer confidence hit a 17-year high.

Fed Chairman Jay Powell is testifying today on Capitol Hill. Here’s part of his testimony:

The U.S. economy grew at a solid pace over the second half of 2017 and into this year. Monthly job gains averaged 179,000 from July through December, and payrolls rose an additional 200,000 in January. This pace of job growth was sufficient to push the unemployment rate down to 4.1 percent, about 3/4 percentage point lower than a year earlier and the lowest level since December 2000. In addition, the labor force participation rate remained roughly unchanged, on net, as it has for the past several years–that is a sign of job market strength, given that retiring baby boomers are putting downward pressure on the participation rate. Strong job gains in recent years have led to widespread reductions in unemployment across the income spectrum and for all major demographic groups. For example, the unemployment rate for adults without a high school education has fallen from about 15 percent in 2009 to 5-1/2 percent in January of this year, while the jobless rate for those with a college degree has moved down from 5 percent to 2 percent over the same period. In addition, unemployment rates for African Americans and Hispanics are now at or below rates seen before the recession, although they are still significantly above the rate for whites. Wages have continued to grow moderately, with a modest acceleration in some measures, although the extent of the pickup likely has been damped in part by the weak pace of productivity growth in recent years.

Turning from the labor market to production, inflation-adjusted gross domestic product rose at an annual rate of about 3 percent in the second half of 2017, 1 percentage point faster than its pace in the first half of the year. Economic growth in the second half was led by solid gains in consumer spending, supported by rising household incomes and wealth, and upbeat sentiment. In addition, growth in business investment stepped up sharply last year, which should support higher productivity growth in time. The housing market has continued to improve slowly. Economic activity abroad also has been solid in recent quarters, and the associated strengthening in the demand for U.S. exports has provided considerable support to our manufacturing industry.

Against this backdrop of solid growth and a strong labor market, inflation has been low and stable. In fact, inflation has continued to run below the 2 percent rate that the FOMC judges to be most consistent over the longer run with our congressional mandate. Overall consumer prices, as measured by the price index for personal consumption expenditures (PCE), increased 1.7 percent in the 12 months ending in December, about the same as in 2016. The core PCE price index, which excludes the prices of energy and food items and is a better indicator of future inflation, rose 1.5 percent over the same period, somewhat less than in the previous year. We continue to view some of the shortfall in inflation last year as likely reflecting transitory influences that we do not expect will repeat; consistent with this view, the monthly readings were a little higher toward the end of the year than in earlier months.

After easing substantially during 2017, financial conditions in the United States have reversed some of that easing. At this point, we do not see these developments as weighing heavily on the outlook for economic activity, the labor market, and inflation. Indeed, the economic outlook remains strong. The robust job market should continue to support growth in household incomes and consumer spending, solid economic growth among our trading partners should lead to further gains in U.S. exports, and upbeat business sentiment and strong sales growth will likely continue to boost business investment. Moreover, fiscal policy is becoming more stimulative. In this environment, we anticipate that inflation on a 12-month basis will move up this year and stabilize around the FOMC’s 2 percent objective over the medium term. Wages should increase at a faster pace as well. The Committee views the near-term risks to the economic outlook as roughly balanced but will continue to monitor inflation developments closely.

-

Morning News: February 27, 2018

Posted by Eddy Elfenbein on February 27th, 2018 at 7:05 amDalio Says Central Banks Face Challenge After ‘Goldilocks’ Phase

After Anbang Takeover, China’s Deal Money, Already Ebbing, Could Slow Further

German Court Rules Cities Can Ban Vehicles to Tackle Air Pollution

In a Blow to AT&T, Federal Judges Have Rejected ‘The Loophole That Could’ve Swallowed the Internet’

5 Key Questions for New Fed Chair Powell That Will Be Crucial for Stocks

California Scraps Safety Driver Rules for Self-Driving Cars

Comcast Just Bid $31 Billion to Buy Sky Out From Under Rupert Murdoch and Fox

This Big Cryptocurrency Acquisition Could Create a Wall Street-Style Financial Giant

Qualcomm, Broadcom Drama Enters New Act

Sam’s Club Jumps Into Same-Day Grocery Delivery With Instacart’s Help

Howard Lindzon: The Market Does Not Care

Roger Nusbaum: Did Dennis Gartman Really Get Blown Up? & Hedging; Are You Doing It Wrong?

Be sure to follow me on Twitter.

- Tweets by @EddyElfenbein

-

-

Archives

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His