-

New All-Time High

Posted by Eddy Elfenbein on December 15th, 2017 at 4:39 pm

The S&P 500 closed today at another new all-time high. The S&P 500 is now up 19.52% YTD (not including dividends).

Our Buy List is up 19.80% YTD (again, without divs). Four of our Buy List stocks are at new highs: AFLAC (AFL), Hormel Foods (HRL), Ingredion (INGR) and Microsoft (MSFT).

Express Scripts (ESRX) was up 3.67% today thanks to an upgrade from Baird.

HEICO (HEI) was up 4.72% today after they announced their stock split and dividend increase.

-

Stock Split and Dividend Hike for HEICO

Posted by Eddy Elfenbein on December 15th, 2017 at 11:05 amHeico announced that it will be splitting its stock 5-for-4. In other words, you’ll get one extra share for every four you currently own.

Also, the company’s semi-annual dividend will rise from 8 cents to 8.75 cents. After the split, the new dividend will be 7 cents per share.

Remember that HEICO split 5-for-4 in April.

-

CWS Market Review – December 15, 2017

Posted by Eddy Elfenbein on December 15th, 2017 at 7:08 am“They say you never go broke taking profits. No, you don’t. But neither do

you grow rich taking a four-point profit in a bull market.” – Jesse LivermoreThis week, the Federal Reserve decided once again to raise interest rates. True, interest rates are still quite low, but a lot of folks thought these hikes were a long way off (including me). Now they’ve really happened.

The Fed also released its economic projections for the next few years. They see more rates coming next year (call me a cautious doubter on that). Remember, the environment for stocks will remain favorable as long as rates don’t get too high. We’re not there yet, so stocks are still good.

Speaking of which, the S&P 500 touched another all-time high this week. This continues to be a very good environment for stocks. Strangely, a lot of investors have left the stock market and tried their hands at crypto-currencies. I’ll give you my thoughts on bitconmania.

Reminder: Next week, I’ll unveil the 2018 Buy List. Millions of investors all over the world are eagerly awaiting our new list. I can barely contain my excitement. Stayed tuned! But first, let’s look at what the Federal Reserve decided to do this week.

The Federal Reserve Raises Rates

On Wednesday, the Federal Reserve again raised interest rates. The new range for the Fed funds rate is 1.25% to 1.50%. This was the third increase this year and the fifth for this cycle. As I’ve said before, I think it was a mistake to raise rates, but I can’t say it’s a terrible, horrible, no good, very bad mistake. Two FOMC members agreed with me and dissented from this decision.

In the Fed’s statement, they noted the good economic news. They said “job gains have been solid” and “economic activity has been rising at a solid rate.” (I think “solid” was the word of the month.)

The Fed also noted that inflation has trended lower in recent months, but they think it will rise to 2%, which is their target rate. I’m not so sure about that. This week, we got the inflation report for November and inflation is still well behaved. For November, headline inflation rose by 0.39%, and the “core rate,” which excludes food and energy, rose by just 0.12%. In the last 12 months, headline inflation is running at 2.20% while the core rate is at 1.71%. In fact, the year-over-year core rate has barely moved in the last six months. Maybe the Fed is right and low inflation will pass, but I see no signs of it yet.

The Fed also released its economic projections for the next few years. The Fed members are more optimistic on economic growth for next year. In September, they saw GDP rising by 2.1% next year. Now they see it rising by 2.5%. I hope that’s right.

The members project three more rate increases for next year. After that, they see two more hikes in 2019 and another one or two in 2020. I should caution that the range of estimates is very diffuse for 2019 and 2020. I don’t put much faith in forecasts that far out.

If the Fed’s near-term forecasts are right, that will mean that real short-term rates will finally be positive sometime next year. It will probably happen sometime in June. That will end 10 years of negative real rates.

The Fed is right to be optimistic for the economy. This week, we got a very good report on retail sales for November. Hopefully, that’s an omen for strong holiday sales. Thursday’s initial claims report came very close to being the lowest in more than 44 years.

To sum up: Things are looking very good right now. I’m not worried about stocks, especially our Buy List. The Fed will eventually screw this up, but not for a while.

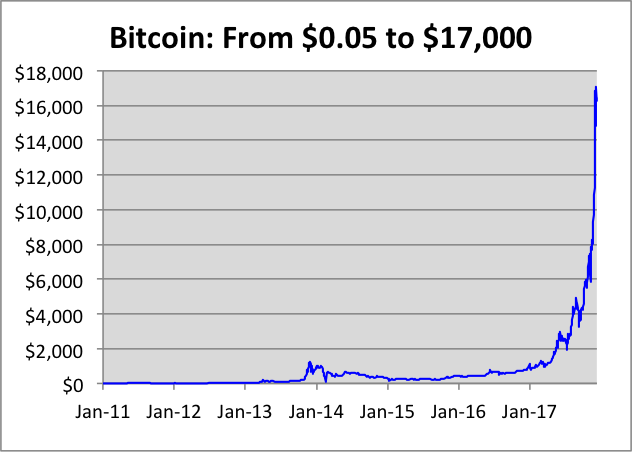

My Thoughts on Bitcoin

A number of investors have asked me for my opinion on bitcoin. It seems to be the topic of the season. This week, bitcoin futures were unveiled on Wall Street.

I haven’t commented much on bitcoin for the simple reason that I don’t know much about it. Unlike too many people in finance, I prefer to limit my comments on topics I’m familiar with.

With that caveat, let me offer some thoughts on investing in bitcoin. I would summarize my position as ranging between agnostic to intrigued on the future for bitcoin as an instrument, yet I’m very negative on the idea of bitcoin’s place in a sound portfolio.

I want to make it clear that I’m not anti-bitcoin in any sense. I welcome the idea of a stateless cyber currency. We need disruption. Bitcoin, and its many competitors, have made truly impressive gains.

I do have a few concerns. At the top is the currency’s dramatic volatility. Bitcoin routinely gaps up or down by 10% or more in a trading session. Until that slows down, I think it will limit bitcoin’s acceptance in regular daily use.

A currency needs to be two things: a store of value and a medium of exchange. Bitcoin is really good at the former but not so hot at the latter. This needs to change. I’m also concerned about the amount of fraud and theft. Of course, this can happen with any currency, but the problem seems especially acute with bitcoin. Also, a lot of these shady initial coin offerings won’t end well. Make no mistake—a lot of crypto-heads understand the challenges and they’re working to solve them. We’re still early in this game.

I think there’s a very good chance that bitcoin will eventually fall by the wayside as rivals, like Etherium, prove to be more durable. Emergent technologies tend to invite intense competition followed by extreme consolidation. Bitcoin is no different.

Now I want to turn to the idea of investing in bitcoin. I have no issue if someone wants to buy a few BTC to be part of the phenomenon. Sure, why not? What I mean to address is the idea of bitcoin’s place in a serious investment portfolio. That’s nuts.

We have to be up front with the fact that bitcoin is in a very big bubble. Like all bubbles, it feeds on itself and you never know where it will end. I often tell investors that true bubbles are rare. A rising stock market probably isn’t a bubble. A bubble is when an asset soars for many times what it could possibly be worth. Bitcoin will pop. I just don’t know when.

To show you how bananas things are, a biotech company recently changed its name to Riot Blockchain. The shares went from $7 last to month to as high as $33 this week. Now that’s a mania. A bubble is when something is soaring for no other reason than that it’s been soaring. The mania feeds upon itself as investors are afraid of being left behind. That’s what’s going on now.

I’m staying far away from bitcoin. It’s a new game, and I admit I don’t know the rules (nor does anyone else). Around here, we approach investing like it’s a business because that’s what it is. When we look at a company, we analyze real things like sales and earnings, but with bitcoin, there’s nothing. It’s guessing at the breeze. I don’t see how anyone can estimate where the price should be right now.

I wish bitcoin well, but it has no part of a long-term investment portfolio.

Buy List Updates

We have a Buy List earnings report next week. After the close on Monday, December 18, HEICO (HEI) is due to report its fiscal Q4 earnings. That’s for the quarter ending on October 31. A conference call will come on Tuesday morning.

In August, HEICO raised its guidance for full-year earnings. They previously expected full-year net income growth of 12% to 14%. They now expect net income growth of 14% to 16%.

HEICO doesn’t provide per-share guidance, so we need a little math. By my numberifying, the new guidance implies Q4 earnings of 55 to 59 cents per share and full-year earnings of $2.08 to $2.12 per share. The stock is a 48% winner for us this year.

This week, Express Scripts (ESRX) gave an upbeat forecast for Q4 and for 2018. The pharmacy benefits manager said they see EPS for next year ranging between $7.67 and $7.87. Wall Street had been expecting $7.65 per share. That’s good to see.

Express also raised its 2017 forecast to $7.00 to $7.08 per share. That’s a three-cent increase at both ends. Through the first three quarters of this year, Express has earned $4.94 per share. That means the new range implies Q4 earnings of $2.06 to $2.14 per share.

Before I go, I want to raise my Buy Below prices on two of our Buy List stocks. I’m raising our Buy Below on Ingredion (INGR) to $146 per share. I’m also raising AFLAC (AFL) to $93 per share. The duck stock hit a new all-time high this week.

That’s all for now. There are a few economic reports to look out for next week. On Wednesday, we’ll get the existing home sales report. The last one was quite good. Then on Thursday, we’ll get the second update on Q3 GDP growth. The initial estimate was for 3.0% growth which was later revised up to 3.3%. Let’s see if it goes any higher. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: December 15, 2017

Posted by Eddy Elfenbein on December 15th, 2017 at 7:03 amNet Neutrality Is Gone. Feel The Freedom Coursing Through Your Veins.

What the World’s Central Banks Are Saying About Bitcoin

JPMorgan Sees S&P 500 Hitting 3,000, Warns on Tech Stocks

How America’s Inequality Is Sending the Dow Soaring

Big Data and a Bullet Train Drive Ties Between India and Japan

China’s HNA Keeps Striking Foreign Deals as Banks Wince and Investors Flee

Labor Board Reverses Ruling That Helped Workers Fight Chains

No Sequel to ‘Massacre at the Shopping Mall’ This Year

Disney Makes $52.4 Billion Deal for 21st Century Fox in Big Bet on Streaming

Murdoch Solves Empire Succession by Getting Rid of the Empire

Airbus Board Triggers Shake-Up to End Succession Row

1 Red Flag on Tesla’s Balance Sheet, Made Even Worse By the Red Flag on Its Cash Flow Statement

Jeff Carter: The Common Mistake

Be sure to follow me on Twitter.

-

Retail Sales Rose 0.8% Last Month

Posted by Eddy Elfenbein on December 14th, 2017 at 3:24 pmAs the holiday shopping season ramps up, we got a look at the retail sales report for November. Last month, retail sales rose by 0.8%. The number for October was bumped up from growth of 0.2% to growth of 0.5%.

If we look at “core” retail sales, which doesn’t include cars, gas, building materials or food services, then retail sales rose by 0.8%. This suggests the consumer is in a good mood.

We also got the initial claims report, which dropped to 225,000. That’s very close to a multi-decade low. Eight weeks ago, we got down to 223,000. That was the lowest since March 31, 1973.

-

Express Scripts Gives Upbeat Forecast

Posted by Eddy Elfenbein on December 14th, 2017 at 11:23 amShares of Express Scripts (ESRX) are doing well this morning after the company gave an optimistic forecast for 2018:

Express Scripts said it expected adjusted full-year 2018 earnings of $7.67 to $7.87 per share, above analysts’ average expectation of $7.65, according to Thomson Reuters I/B/E/S.

The company said it estimated that eviCore would have adjusted earnings before income, tax, depreciation and amortization of $265 million to $285 million in 2018.

Express Scripts’ shares were up 1.8 percent at $69.83 in pre-market trading.

The company said the forecast also included the sale of its United Biosource unit to Avista Capital Partners, which was announced last month.

Express Scripts also increased its full-year 2017 adjusted earnings per share outlook to $7 to $7.08, from its earlier estimate of $6.97 to $7.05.

Express has earned $4.94 per share through the first three quarters, so the new range implies Q4 earnings of $2.06 to $2.14 per share. Wall Street had been expecting $2.06 per share.

-

Morning News: December 14, 2017

Posted by Eddy Elfenbein on December 14th, 2017 at 7:04 amOil Trades Below $57 After IEA Says OPEC May Not See Happy 2018

Russia Wins in Arctic After U.S. Fails to Kill Giant Gas Project

Europe’s Central Bank, Lagging Its Counterparts, Faces Eventful 2018

Why the Fed Raised Rates (For a Fifth Time)

Yellen Isn’t Buying Trump’s Tax Cut Talk of an Economic Miracle

Federal Communications Commission Set to Reverse Net Neutrality Rules

Bitcoin Trading Thrives Wherever Regulators Crack Down Most

Ripple Price Surges 84% In A Day To New Record High. Is XRP The Next Crypto Rocket ‘To The Moon’?

Target to Buy Shipt for $550 Million in Challenge to Amazon

Disney’s Fox Acquisition Means the End of Hulu As We Know It

2017 Was Bad for Facebook. 2018 Will Be Worse.

Howard Lindzon: A 2018 Prediction – More Fintech

Roger Nusbaum: A 64% Decline? Really?

Be sure to follow me on Twitter.

-

The Latest Fed Projections

Posted by Eddy Elfenbein on December 13th, 2017 at 2:18 pmHere are the latest economic projections from the Fed. The median forecast calls for three more rate hikes next year. After that, it’s two more in 2019 plus one or two in 2020.

This means that the real Fed funds rate will finally get up to 0% by the second rate hike next year (June, maybe). It will take four rate hikes for the Fed funds rate to match the current 10-year yield.

-

The Fed Hikes Again

Posted by Eddy Elfenbein on December 13th, 2017 at 2:12 pmThe Fed raised rates. There were two dissents. Here’s the statement:

Information received since the Federal Open Market Committee met in November indicates that the labor market has continued to strengthen and that economic activity has been rising at a solid rate. Averaging through hurricane-related fluctuations, job gains have been solid, and the unemployment rate declined further. Household spending has been expanding at a moderate rate, and growth in business fixed investment has picked up in recent quarters. On a 12-month basis, both overall inflation and inflation for items other than food and energy have declined this year and are running below 2 percent. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations are little changed, on balance.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. Hurricane-related disruptions and rebuilding have affected economic activity, employment, and inflation in recent months but have not materially altered the outlook for the national economy. Consequently, the Committee continues to expect that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace and labor market conditions will remain strong. Inflation on a 12‑month basis is expected to remain somewhat below 2 percent in the near term but to stabilize around the Committee’s 2 percent objective over the medium term. Near-term risks to the economic outlook appear roughly balanced, but the Committee is monitoring inflation developments closely.

In view of realized and expected labor market conditions and inflation, the Committee decided to raise the target range for the federal funds rate to 1-1/4 to 1‑1/2 percent. The stance of monetary policy remains accommodative, thereby supporting strong labor market conditions and a sustained return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. The Committee will carefully monitor actual and expected inflation developments relative to its symmetric inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

Voting for the FOMC monetary policy action were Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; Patrick Harker; Robert S. Kaplan; Jerome H. Powell; and Randal K. Quarles. Voting against the action were Charles L. Evans and Neel Kashkari, who preferred at this meeting to maintain the existing target range for the federal funds rate.

-

Inflation Is Still Tame

Posted by Eddy Elfenbein on December 13th, 2017 at 1:21 pmThe Fed’s policy decision is coming out later today. Just in time, we got the inflation report for November this morning. Not surprisingly, inflation is still very low.

Headline inflation rose by 0.39% last month. Some of that was caused by energy prices. The “core rate,” which excludes food and energy, rose just 0.12%.

In the last 12 months, headline inflation is running at 2.20% while the core rate is at 1.71%. In fact, the year-over-year core rate has barely moved over the last six months.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His