-

Jobless Claims Hit 44-1/2-Year Low

Posted by Eddy Elfenbein on October 19th, 2017 at 4:01 pmFrom Reuters:

The number of Americans filing for unemployment benefits dropped to its lowest level in more than 44-1/2 years last week, pointing to a rebound in job growth after a hurricane-related decline in employment in September.

The labor market outlook was also bolstered by another report on Thursday showing a measure of factory employment in the mid-Atlantic region racing to a record high in October. The signs of labor market strength could cement expectations that the Federal Reserve will raise interest rates in December.

“It doesn’t take one hundred PhD economists at the Fed to figure out that the labor market is on the tight side of normal,” said John Ryding, chief economist at RDQ Economics in New York. “At this point, we would expect a sharp bounce-back in employment growth in October.”

Initial claims for state unemployment benefits fell 22,000 to a seasonally adjusted 222,000 for the week ended Oct. 14, the lowest level since March 1973, the Labor Department said. But the decrease in claims, which was the largest since April, was probably exaggerated by the Columbus Day holiday on Monday.

-

30 Years Ago Today

Posted by Eddy Elfenbein on October 19th, 2017 at 1:33 pm

Thirty years ago today, shares of $AAPL plunged from $1.72 to $1.30 (adjusting for splits). Today, they’re at $155. Berkshire Hathaway fell from $3,890 to $3,170. Today, it’s at $280,000. The 30-year Treasury was yielding 10.25%. Now it’s at 2.83%.

Here’s FNN from that day.

Here’s that weekend’s Wall $treet Week.

-

Morning News: October 19, 2017

Posted by Eddy Elfenbein on October 19th, 2017 at 7:05 amCould the 1987 Stock Market Crash Happen Again?

Zhou Warns China Should Defend Against Threat of ‘Minsky Moment’

Europe’s Fastest-Growing Economy Could Be Headed for Trouble

British Retail Sales Slip Amid Household Income Squeeze

Trump Selects Washington Lawyer Joe Simons to Head FTC

Everyone’s Mad at Google and Sundar Pichai Has to Fix It

F.D.A. Approves Second Gene-Altering Treatment for Cancer

Want a Piece of Ford’s $28 Billion Hoard? Don’t Hold Your Breath

Blue Apron Says It Cut 6% of Workforce for ‘Future Growth’

Here’s the $30 Billion Startup You’ve Probably Never Heard Of

Why Spam Is Now Under Lock-And-Key At Oahu Stores

Nissan Suspends Local Car Production for Japan for Two Weeks

Does Ken Chenault Deserve a Better Sendoff Than Jeff Immelt?

Roger Nusbaum: Indexing: Valid But Flawed

Cullen Roche: Cryptocurrencies Are Non-Financial Collective Equity, Financial Wisdom Part Deux – Factor Investing, Financial Wisdom Part Three – Funny Money

Be sure to follow me on Twitter.

-

Finding an Undiscovered Factor

Posted by Eddy Elfenbein on October 18th, 2017 at 1:24 pmHere’s the latest entry in Tadas Viskanta’s Blogger Wisdom:

Question: Assume you have discovered an equity return factor that is both previously unknown and uncorrelated with other factors. What would you do to monetize that insight?

Here’s a sampling of answers:

Ben Carlson, A Wealth of Common Sense, @awealthofcs, author of Organizational Alpha: How to Add Value in Institutional Asset Management:

Setting up a hedge fund and leveraging that factor would seem to make sense but that just opens you up to competition. I guess the best thing to do would be to set up an index and license it out to all of the smart beta ETF and mutual fund providers and be the gatekeeper on it.

Eddy Elfenbein, Crossing Wall Street, @eddyelfenbein:

Discovering the factor is just one step. That doesn’t mean it has a trend of any sort, either up or down. Plus, if it’s truly uncorrelated, then it’s only value is at the service of diversification. Personally, I would build an index or ETF to monetize it.Morgan Housel, Collaborative Fund, @morganhousel:

First I’d double check my math. Then I’d give it to the 10 smartest people I know and ask them to rip it apart. Cherry picking is rife in the backtest world. -

Anthem Goes It Alone

Posted by Eddy Elfenbein on October 18th, 2017 at 1:19 pmIt’s finally happened, and I didn’t think it would. Anthem has broken with Express Scripts decided to start its own drug plan.

Health insurer Anthem Inc. plans to set up its own pharmacy benefits management unit, signaling a final break with Express Scripts Holding Co. after accusing it of overcharging by billions of dollars.

The move means Express Scripts will not only lose its biggest client but also face a new rival. Anthem’s new unit, called IngenioRx, will grow its own business with a “full suite” of services, the insurer said in a statement on Wednesday.

Anthem said it had also secured a five-year agreement with CVS Health Corp. — the operator of a pharmacy benefits manager that is Express Scripts’ biggest competitor — that goes into effect after its current contract with Express Scripts expires at the end of 2019.

The pharmacy benefit management business has been under pressure from all sides. Lawmakers in Washington have been asking how PBMs — which act as middlemen administering complex drug contracts and negotiating prices — make their profits. Drugmakers have blamed PBMs for consumer outrage over the high cost of medicine in the U.S. And analysts have speculated that Amazon.com Inc. is eyeing the industry as ripe for disruption.

Express Scripts said it has already been taking steps to mitigate the fallout from Anthem’s exit. The news is “not unexpected, but is disappointing,” said Brian Henry, an Express Scripts spokesman.

Shares of ESRX are up about 2.5% today.

-

Morning News: October 18, 2017

Posted by Eddy Elfenbein on October 18th, 2017 at 7:03 amEU Air Safety Body Urges Halt on Use of Kobe Steel Products

Whatever the Rule, Investors See Taylor Turning Fed Hawkish

White House Push to Help Workers Through Corporate Tax Cut Draws Skepticism

US Authorities Charge Rio Tinto With Fraud & Rio Tinto’s Scramble for Africa

Taiwan Ministry Expresses ‘Deep Concern’ About Qualcomm’s Antitrust Fine

IBM Roars In Premarket Trading After Blowout Q3 Cloud Sales

J.P. Morgan to Buy Payments Firm WePay in First Major Fintech Acquisition

How the Frightful Five Put Start-Ups in a Lose-Lose Situation

Self-Driving Cars Could Come to Manhattan

Nordstrom Shelves Its Months-Long Plan to Go Private

J&J Wins Reversal of First St. Louis Talc-Cancer Verdict

George Soros Transfers Billions to Open Society Foundations

Josh Brown: Just Own The Damn Robots.

Ben Carlson: Risk Perception vs. Risk Profile

Howard Lindzon: The Nikkei and The 1987 Crash – A Historical Market Week

Be sure to follow me on Twitter.

-

September Industrial Production +0.3%

Posted by Eddy Elfenbein on October 17th, 2017 at 2:24 pmThis morning, the Fed reported that industrial production rose by 0.3% last month. They also revised August up to -0.7%. The Fed said that number for September was dinged by 0.25% due to the hurricanes.

-

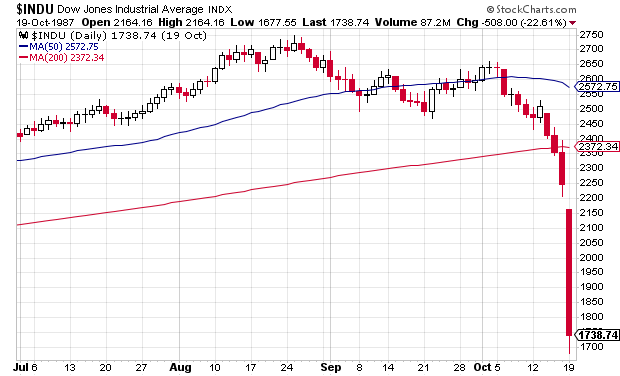

What Caused the 1987 Crash?

Posted by Eddy Elfenbein on October 17th, 2017 at 1:02 pmSo what caused the big crash 30 years ago? The official answer was program trading. But Gary Alexander at Navellier Market Mail says it was political mistakes.

On October 19, 1987, 30 years ago, the stock market fell 22.6% in one day – almost twice the decline of the previous worst day on Wall Street, which was Monday, October 28, 1929 – the now-forgotten Black Monday between Black Thursday (October 24) and Black Tuesday (October 29). What caused this crash?

The answer seems like “settled science.” Investopedia says, “The cause of the stock market crash of 1987 was primarily program trading.” Barron’s (“Computers in Control,” October 16, 2017) says the culprit was “portfolio insurance, a quantitative tool designed to use futures contracts to protect against market losses.” This, they said, creates “a poisonous feedback loop as automated selling begat more of the same.”

I beg to differ. Saying that a market crash is caused by computerized trading is like saying the California wildfire was caused by a localized fire that spread fast. But what sparked the fire and fueled its growth?

Let me offer a longer-term, three-stage explanation – using three “P” words. In chronological order, the core cause of the crash was Prosperity (rapid GDP growth and a huge 50% market surge in the previous year), exacerbated by Politics (a series of bone-headed mistakes, mostly by Congress, a Secretary of State, and a rookie Fed Chairman), and then Panic, when fear stalked the market floor, creating a selling frenzy.

Blaming computers focuses only on the final panic day, paying no attention to what caused the record declines in two of three previous trading days (October 14/16) and what made Monday much worse.

In short, the market crashed in mid-October 1987 because it had risen too far too fast, based on rising prosperity caused by two major tax cuts, the 1981-82 Kemp-Roth tax cuts and a major 1986 tax rate cut.

The first thing to remember about historic panics is that they generally follow parabolic increases during “manic” episodes of over-hyped greed. In the biggest crashes last century, namely 1907, 1929, 1987, and 2000, the market was already too high, but then it shot 50% higher in a year or so. Back in 1985 and 1986, the market was rising to all-time highs almost every month. Then it took off in a hockey-stick rise:

On October 22, 1986, a year before the crash, President Reagan signed the Tax Reform Act of 1986 into law. The top rate was cut dramatically from 50% to 28%, giving us the closest thing to flat taxes we’ve seen in the last century. The Dow Jones index was 1805 on October 21, 1986, but it rose 50.8% in 10 months, to 2722 on August 25, 1987, based in part on the euphoria over those drastic tax rate cuts.

Going back further, the Dow had risen 250% in five years after the first Reagan tax cuts. The GDP was soaring each year in the mid-80s, starting with a huge 7.8% real gain in 1983. After a deep recession in 1981-82, real GDP rose 25 years in a row (1983-2007) with the mid-80s (1983-88) averaging +4.8%.

Political Mistakes – not Economic Fundamentals – Panicked the Market

When the market crashed in 1987, there was no fundamental reason for the crash. There was no recession in sight; earnings were strong, and inflation was under control, but the rapid rise in stock prices had created fears of an exploding bubble. Specifically, there were widespread fears of a recession, slower earnings, and rising inflation, when there was virtually no evidence for any one of those three major fears.

Right before the market peak, on August 11, 1986, economist Alan Greenspan was sworn in as Chairman of the Federal Reserve Board. Within a month, on September 4, Mr. Greenspan made a rookie mistake, firing a pre-emptive strike against relatively tame inflation by raising the Discount Rate 50 basis points. The Dow fell 62 points on that news, while the Prime Rate rose from 8.25% to 9.25% by early October.

Then, another political blunder emerged on Wednesday, October 14, 1987, when a tax bill was introduced in the House Ways and Means Committee that would severely limit tax deductions for interest paid on debt used to finance mergers or hostile takeovers (which had been running rampant throughout 1987).

Bonds had already fallen 13% in the previous six months, but the bond market got hit particularly hard that week. On Friday, Treasury bond rates rose to over 10% and contributed to Friday’s record down day.

On Saturday, U.S. Secretary of the Treasury James Baker III told the Germans to “either inflate your mark, or we’ll devalue our dollar.” Then, Baker went on some of the Sunday morning talk shows to say the U.S. “would not accept” the recent German interest rate increase. An unnamed Treasury official added that we would “drive the dollar down” if necessary. This led European markets to fall on Monday.

In summary, blunders by two political appointees caused the 1987 crash. First, the rookie chairman of the Federal Reserve Board, Alan Greenspan, made it his first order of business to announce his presence by raising the Discount Rate. Then, Secretary of the Treasury James Baker talked tough to the Germans about the dollar, causing global markets to crash. Between Baker’s currency wars, Greenspan’s tight money, a new tax bill that punished businesses, and more threats of protectionist legislation, the problem was too much, not too little, federal government intervention in a fairly smoothly-running economy.

In the morning after the crash, Greenspan tried to undo all the damage he had helped to cause. He cut the Discount Rate to where it was before he took office. As a result, Tuesday, October 20, 1987 set a record for the largest single-day gain (102.27 Dow points) and a 55-year record for daily percentage gain (+6%). Both records were then decimated on Wednesday, October 21, with a 10.1% gain of 186.84 Dow points.

After the crash, Congress reversed itself on their corporate tax grab. They reduced the corporate income tax rate from 40% to 34%, giving business a firmer footing for their financial planning, resulting in stronger earnings growth and net GDP growth the following year. For all of 1987, the Dow actually rose 2.2% and we reached a new all-time high within two years – as if the crash had never happened.

In 1987, Wall Street feared a drying up of corporate profits, but corporate profits soared in 1988 after the corporate tax rate was sliced from 40% to 34%. This can happen again. Applying all these lessons from 1987, we can (1) create a new boom by lowering personal tax rates (while repealing most deductions). We can also (2) avoid a crash by not punishing businesses for their success, and we can (3) revive a slow economy by reducing corporate taxes and regulations, giving businesses more reasons to expand and hire.

Could 1987 happen again? It’s not likely now, but a stock “melt-up” following a major tax reform bill this year or next could push the market up too fast. If the Dow rose to 27,000 or higher in a year, that would be too-far, too-fast, but we’re highly unlikely to see a major crash without seeing manic gains at record highs amidst a new wave of panic-buying and greed. We’re nowhere near those manic levels now.

-

Morning News: October 17, 2017

Posted by Eddy Elfenbein on October 17th, 2017 at 6:58 amU.K. Inflation Climbs to 5 1/2-Year High on Food, Transport

Why Investors Can’t Get Enough of Tajikistan’s Debt

Airbus Tie-Up With Bombardier Is Test for China’s Ambitions

Netflix’s Streaming Ambitions Don’t Come Cheap

SoftBank’s Deal to Invest in Uber ‘Very Likely’ In The Next Week, Arianna Huffington Says

London Eye Owner Merlin Plunges as Terror Threat Hits Growth

Ruby Tuesday Gets The Best Deal It Could Have

American Express Fee Accusations Get U.S. High Court Hearing

Justice Department Gets Involved in Kobe Steel Metal Scandal

It’s Time For Tesla To Stop Paying SolarCity’s Debts

Patents for Restasis Are Invalidated, Opening Door to Generics

T-Mobile, Sprint Plan Merger Without Selling Assets

Cullen Roche: Moneyness, Utility & Network Effects

Roger Nusbaum: FOMC Divergence

Michael Batnick: Advice For Aspiring Traders

Be sure to follow me on Twitter.

-

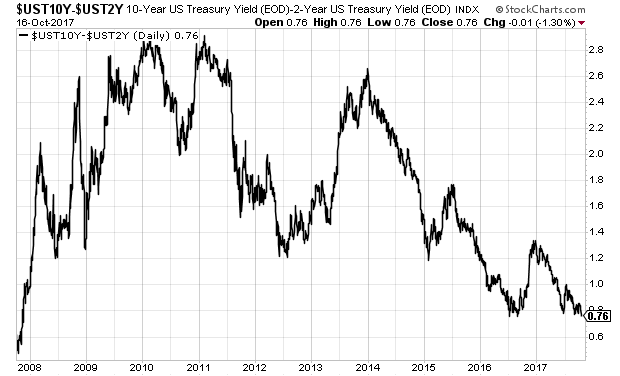

2/10 Spread Near 10-Year Low

Posted by Eddy Elfenbein on October 16th, 2017 at 9:43 pmI like to keep an eye on the spread between the two- and ten-year Treasury bonds. It’s hardly perfect, but it has a decent track record of going negative before recessions.

Today, the 2/10 spread closed at 0.76%. That’s tied for the narrowest spread in nearly ten years. We’re not in the danger zone yet, but we are getting closer. I think this means the Fed can only hike rates a few more times.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His