-

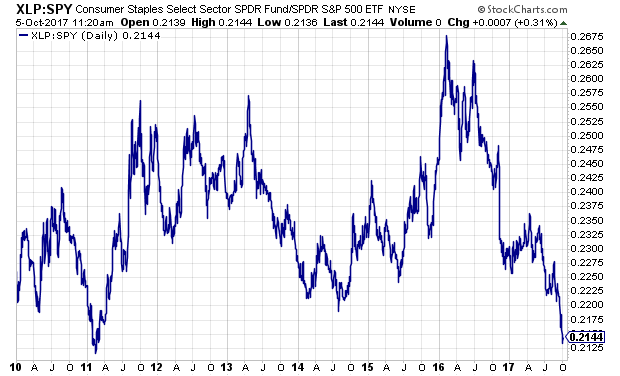

Lagging Staples

Posted by Eddy Elfenbein on October 5th, 2017 at 11:23 amHere’s the Consumer Staples Sector ETF (XLP) divided by the S&P 500. The staples have lagged the market for 18 months.

-

Signs of a Top

Posted by Eddy Elfenbein on October 5th, 2017 at 11:18 amA biotech company changes its name to Riot Blockchain and the shares double in a week:

Nasdaq-listed Bioptix, which previously had as its main business the development of a follicle-stimulating hormone for cows, horses and pigs, took a page out of the same playbook by changing its name to Riot Blockchain. Cryptocurrencies are hot stuff and the company is even investing in a Canadian trading platform for them.

Its shares went as high as $9.50 on Wednesday or more than double their price a week ago. Investors should make hay while the sun shines.

I think I know how this story ends.

-

Morning News: October 5, 2017

Posted by Eddy Elfenbein on October 5th, 2017 at 7:08 amBrexit Bridge Must Be Set by Christmas, Bank of England Official Says

Puerto Rico Is Running Out of Money

Yellen Says Fed Should Make Sure Bank Rules Aren’t Too Burdensome

The White House and Equifax Agree: Social Security Numbers Should Go

Former CEO Struggles to Defend Why Equifax Deserves $7 Million IRS Contract to Prevent Fraud

Foxconn Chooses Wisconsin Town For Its Factory

Adidas Brings the Fast Shoe Revolution One Step Closer

AT&T CEO Makes the Case For Acquiring Time Warner

Amazon Is Testing Its Own Delivery Service to Rival FedEx and UPS

Google’s New Gadgets Come With a Big Helping of A.I.

Saudi Aramco IPO on Track for 2018

Monsanto’s Roundup Faces European Politics and U.S. Lawsuits

Roger Nusbaum: Why Does Larry Swedroe Hate Dividends?

Jeff Carter: Evolution of Equities

Michael Batnick: Lost in The Shuffle

Be sure to follow me on Twitter.

-

ADP Jobs Report: +135,000

Posted by Eddy Elfenbein on October 4th, 2017 at 11:54 amThe big jobs report is this Friday morning. Every Wednesday before the jobs report, we get a preview from ADP, the payroll people. They release their employment report which only covers private sector jobs.

This morning, ADP said the US economy created 135,000 private sector jobs last month. That was 10,000 more than forecast. This was the worst month for new jobs since last October, but it was still better than expectations. Obviously, the recent storms had an impact.

Job growth was concentrated at larger firms, with businesses that employ 500 or more workers growing by 79,000. Smaller firms seemed to be hit the most by the storm damage, as companies that employ fewer than 50 workers saw their staffing decline by 7,000.

On the other side, goods-producing firms saw a sizable boost in hiring, gaining 48,000 positions thanks to a jump of 29,000 for construction as well as 18,000 new positions in manufacturing. Mining and natural resources also continued to grow, adding 1,000.

Not surprisingly, services accounted for the bulk of the job growth at 88,000 new jobs. That was led by a gain of 51,000 in professional and business services. However, the sector was held back by a decline of 18,000 in the usually strong trade, transportation and utilities sector and a drop of 11,000 in information services.

Here’s the recent trend. The ADP report is the blue bar. The red bar is the government’s.

Note that the red bar isn’t the full NFP number but just the private sector.

-

RPM International Earns 86 Cents per Share

Posted by Eddy Elfenbein on October 4th, 2017 at 11:27 amThis morning, RPM International (RPM) reported Q1 earnings of 86 cents per share. That was two cents above expectations.

“We derived significant benefits from the nine acquisitions made in fiscal 2017, along with our selling, general and administrative (SG&A) cost reduction actions taken last year. Rising raw material costs negatively impacted gross profit margins. As a result, we instituted price increases, which began to take effect late in the quarter. After three years of foreign currency headwinds attributable to the strengthening U.S. dollar, currency translation was essentially neutral this quarter,” stated Frank C. Sullivan, RPM chairman and chief executive officer.

This was for their fiscal Q1 which ended in July. Previously, RPM said they see Q1 earnings ranging between 83 and 85 cents per share and between $2.85 and $2.95 per share for the fiscal year. At the time, that disappointed investors. Wall Street had been expecting 89 cents per share for Q1 and $3 per share for the fiscal year.

The company reiterated their full-year forecast of $2.85 to $2.95 per share. With hindsight, we can see that the disappointment wasn’t far below Wall Street’s original take. The shares are currently down about 1.5%.

-

Morning News: October 4, 2017

Posted by Eddy Elfenbein on October 4th, 2017 at 7:06 amDesperate Medicine for Indian Markets

E.U. Targets Amazon and Apple in Tax Avoidance Campaign

EU Takes Ireland to Court For Not Claiming Apple Tax Windfall

Here’s Who Really Holds Power at the Fed

Trump Vows to Wipe Out Puerto Rico’s Debt. Can He Do That?

Equifax And Wells Fargo Apologize To Congress; Lawmakers Not Buying It

Forget Mac vs PC, or iPhone vs Android — The Next Great Battle is Between Google and Amazon

Ford’s Plan For More Smart Vehicles And Services Won’t Work If It Doesn’t Fix Its Business Today

Uber’s Board Reduces Kalanick’s Clout, Backs SoftBank Investment

All 3 Billion Yahoo Accounts Were Affected by 2013 Attack

Nestlé Can Head Off a Fight With Dan Loeb

Mylan Surges as its Generic of Teva’s Copaxone Gets FDA Nod

Ben Carlson: Financial News Doesn’t Rhyme But It Does Repeat Itself

Cullen Roche: Goldman Sachs: No Signs of Recession

Howard Lindzon: Global Synchronized Growth …Momentum Monday (Wednesday Edition)

Be sure to follow me on Twitter.

-

Even With/Due To

Posted by Eddy Elfenbein on October 3rd, 2017 at 1:51 pmI noticed this headline at TheStreet:

Even With Stocks at Records, Volatility Sits at Multi-Year Lows

This gets it backwards. More accurately, the headline should read “Due to Stocks at Records, Volatility sits at Multi-Year Lows.”

-

Warren Buffett on the Fed

Posted by Eddy Elfenbein on October 3rd, 2017 at 1:41 pmBuffett was asked today if investors need to pay attention to who becomes the next Fed chair. His answer:

I don’t spend time thinking about it. It wouldn’t do me any good to think about it. I wouldn’t know the answer in the end. Most of the time, the Fed is not that important. Occasionally, it’s everything. It’s the only game in town.

Warren Buffett: Don’t pay much attention to the Fed from CNBC.

-

Warren Buffett: Stock valuations make sense right now

Posted by Eddy Elfenbein on October 3rd, 2017 at 1:29 pmWarren Buffett: Stock valuations make sense right now from CNBC.

-

Market Updates at 11:30

Posted by Eddy Elfenbein on October 3rd, 2017 at 11:34 amShares of Sherwin-Williams (SHW) are up about 3% this morning. I suspect it has to do with Lennar’s earnings report. The homebuilder beat expectations, and this may suggest that the damage from the storms wasn’t as bad as expected. SHW is up to a new high today. The stock is now up 38% YTD for us.

Shares of HEICO (HEI) are trading lower today. I think that’s due to a downgrade from Zacks.

There were two good economic reports yesterday. The first was the very good ISM. The ISM for September came in at 60.8. That’s the strongest number since 2004. Wall Street had been expecting 58.0. This tells us that the manufacturing sector is still healthy.

Also, the Census Bureau said that construction spending rose 0.5% in August. Construction spending is up 2.5% in the last year.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His