-

CWS Market Review – May 26, 2017

Posted by Eddy Elfenbein on May 26th, 2017 at 7:08 am“The single greatest edge an investor can have is a long-term orientation.”

– Seth KlarmanOn Thursday, the S&P 500 closed at yet another all-time high. The index is already up 7.8% this year, and we’re still in the merry month of May. Last week, the market had a slight jitter, and I thought the recent quiet period might be coming to an end.

Not so.

On Wednesday, in fact, the S&P 500 was on track for one of its narrowest days (meaning the difference between the daily high and low) in decades, but an afternoon surge put that off. Last week, Wall Street was alarmed when the Volatility Index jumped above 16. But once again, the index collapsed. On Thursday, the VIX closed at 9.99. That’s only the seventh sub-10 close in the last 20 years.

It’s as if the low-volatility, slowly upward-trending market is reasserting itself after a momentary disruption. No matter what happens, we keep returning to a market of micro changes that are mostly rising.

In this week’s issue, we’ll look at two of our recent Buy List earnings reports, from HEICO and Hormel Foods. Even though the report from HEICO was quite good, and the report from Hormel was mediocre, both stocks fell. Such is Wall Street. I’ll have more on that in a bit.

But first, I want to discuss this week’s Fed minutes and what the central bank plans to do with its enormous balance sheet. I still think the Fed is making a big mistake by raising interest rates next month. Let’s hope cooler heads prevail.

What Will Happen to the Fed’s $4.5 Trillion Balance Sheet

On Wednesday, the Federal Reserve released the minutes of its last meeting. The minutes revealed largely what Wall Street had expected and what I had feared. The Fed acknowledged the weak spots in the economy, but it still sees the need for another rate hike. I just don’t get it.

If the rate hike happens, and I’m afraid it will, this would be the fourth hike of this cycle. The Fed seems to believe that the sluggishness in the economy during the first quarter will soon pass. I sincerely hope they’re right, but I haven’t seen the evidence just yet. I think the Fed has become overly concerned about the idea of being “behind the curve.” Chairwoman Yellen has said that if we don’t raise rates beforehand, then we’ll require faster rate increases later. What’s so awful about that?

I should be clear that one rate hike probably won’t sink the economy. Even after a fourth hike, real interest rates will still be quite low by historical standards. The facts are clear: wage growth is iffy, inflation isn’t a problem, and there are few signs of an economy overheating.

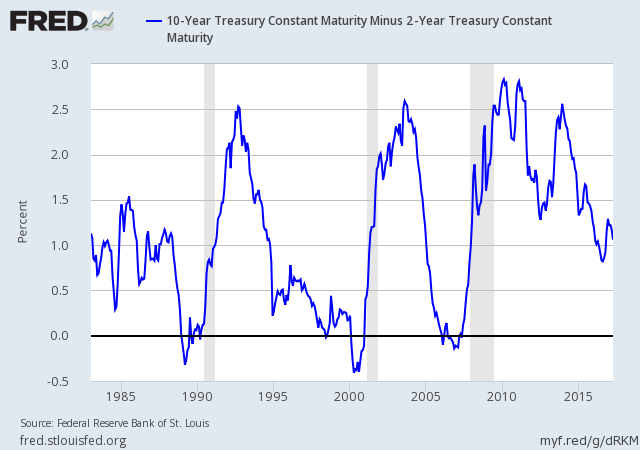

I like to keep an eye on the spread between the two- and ten-year Treasury yields. Over the last 30 years, whenever the spread turns negative, the economy has soon gotten bad. The current spread suggests the Fed can raise rates four more times. That would be three after a rate hike in June. I suspect that means that a rate increase wouldn’t hurt the economy, but it decreases our breathing room for further hikes.

What was interesting about these Fed minutes is that they give us a preview of what the Fed intends to do with its massive balance sheet. Let me rephrase that: the Fed’s gigantic, massive, world-devouring, $4.5 trillion balance sheet. The central bank has been reinvesting the proceeds of its bond holdings into still more bonds. The plan presented at the FOMC meeting is to pull the plug on all that reinvesting. In other words, just let the current holdings mature.

According to Binyamin Appelbaum at the New York Times, the Fed “would begin by keeping a fixed amount of the monthly proceeds and then increase the cap every three months until proceeds were no longer being reinvested.” What’s the downside of this? Probably not much, assuming the economy avoids a recession. That’s even more reason why the Fed should hold off raising interest rates next month. Now let’s take a look at this week’s Buy List earnings reports.

HEICO Earns 53 Cents per Share

After the bell on Tuesday, HEICO (HEI) reported fiscal Q2 earnings of 53 cents per share. That was three cents better than Wall Street’s estimate. The details look pretty good. Net sales rose 5% to $368.7 million. For the first half of the year, net sales are up 8%. I was pleased to see HEICO’s operating margin edge up from 19% a year ago to 20.8% for this year’s Q2.

Laurans A. Mendelson, HEICO’s Chairman and CEO, commented on the Company’s second-quarter results, stating, “We are very pleased to report record quarterly results in consolidated net sales, operating income and net income driven by record net sales and operating income at both operating segments. Our outstanding performance principally reflects increased demand and operating efficiencies within both of our operating segments, as well as the excellent performance of our well-managed and profitable fiscal 2016 acquisition.”

Best of all, HEICO raised its full-year guidance. This was the second increase this year. Unfortunately, the company doesn’t guide for EPS, but they do for a few other metrics.

HEICO now sees net sales rising this year by 8% to 10%. The previous forecast was 6% to 8%. For net income, HEICO projects growth of 12% to 14%, up from 9% to 11%. HEICO also projects cash flow from operations of $270 million. That’s up $10 million from the previous forecast.

Last year, HEICO earned $1.86 per share. If we assume no change in shares outstanding, that implies 2017 EPS of $2.08 to $2.12. Wall Street had been expecting $2.05 per share.

Unfortunately, shares of HEICO dropped 3.4% on Wednesday. I listened to the earnings call, and it seemed fine to me. Perhaps some folks were expecting more. I can’t complain too much about the share price, considering HEI hit a new high on Tuesday. Perhaps the drop was due to some price jitters. I’m lifting my Buy Below on HEICO to $75 per share.

Shares of Hormel Drop on Turkey Issues

On Thursday morning, Hormel Foods (HRL) reported fiscal second-quarter earnings of 39 cents per share. That was a penny below expectations. The culprit is apparently an oversupply of turkeys. Hormel’s Jennie-O Turkey Store saw its volume drop 6% and sales fell 8%.

Turkey prices are near a seven-year low. The issue is that some folks were afraid of another outbreak of avian flu. As a result, they ramped up production. To their credit, Hormel acknowledged the problem and was careful to explain that it’s not a long-term one.

This was, by no means, a lousy quarter for Hormel. Their grocery-products division did quite well, as did their international business. I often tell people that Hormel is a lot more than Spam. Well, it’s a lot more than turkey as well. Most importantly, the company is standing by its full-year forecast of $1.65 to $1.71 per share. However, they now say they expect results to be at the low end of that range.

Shares of Hormel got dinged for a 6.4% loss on Thursday. I’m not bailing out at all. This is still one for the long term, but I will lower my Buy Below on Hormel Foods down to $35 per share.

Buy List Updates

One of the lessons of investing is that periodically, the market freaks out. Sometimes the reasons are good; many times, they’re not.

Last September, shares of Cognizant Technology Solutions (CTSH) plunged after the company said that an internal investigation revealed that the company may have violated the U.S. Foreign Corrupt Practices Act. Cognizant notified the SEC and DOJ. The same day, the company’s president resigned.

That day, the stock got crushed. At one point, CTSH dropped down to $45.44, which was a loss of 17.4% for the day. By the closing bell, the stock had shed 13.3%.

The good news is that we waited the mess out, and on Thursday, CTSH is at a new 52-week high. The stock is up 47% from its post-plunge low.

To quote Warren Buffett, “the stock market is designed to transfer money from the active to the patient.”

I also wanted to highlight the surge in Stryker (SYK). This company doesn’t make a lot of news, but it’s been a steady winner for us. The shares have rallied 32% since mid-November. The company has turned out good earnings reports, plus we got a dividend increase. The shares just closed at another 52-week high.

Shares of Alliance Data Systems (ADS) got a nice boost on Thursday after Signet Jewelers said it was selling ADS $1 billion worth of prime accounts. That represents 55% of Signet’s credit portfolio. The two companies agreed on a seven-year deal in which ADS will become the primary credit source for Signet’s business. Shares of ADS rallied 3.3% on Thursday.

The board of directors at Cerner (CERN) approved a $500 million share-buyback plan. At the current price, the plan represents 2.3% of CERN’s outstanding shares. CEO Marc Naughton said, “Given our strong balance sheet and expected strong cash flow, we are well positioned to continue investing in growth while also returning value to shareholders through share repurchases.”

Over the weekend, Barron’s highlighted Ingredion (INGR). The stock is a favorite of David Anguilm, a portfolio manager:

One favorite is Ingredion (INGR), which makes sweeteners and nutrition ingredients, like ones that make crackers crisper, and pharmaceutical products like intravenous solutions. The stock has pulled back amid concerns about changes in foreign trade. Anguilm sees demand rising from a growing middle class in emerging markets and aging populations in the developed world.

Ingredion “generates strong and consistent cash flows, has a healthy balance sheet, and has a history of returning cash to shareholders,” he says. Ingredion yields 1.7% but has grown its dividend by 170% over the past five years. Its payout ratio is 26% of earnings, “which we believe will allow for attractive dividend growth in the years ahead,” says Anguilm, who recently added to the fund’s position.

That’s all for now. The stock market will be closed on Monday for Memorial Day. I’m taking some time off, so there will be no issue next week. The Memorial Day weekend traditionally marks the beginning of summer. On Tuesday, we’ll get the latest reports on personal income and spending. On Thursday, we’ll get the ADP payroll report plus the ISM report for May. Then Friday is Jobs Day when we’ll get the latest employment figures for May. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: May 26, 2017

Posted by Eddy Elfenbein on May 26th, 2017 at 7:03 amMoody’s: China’s Reforms Not Enough to Arrest Mounting Debt

Japan’s Big Insurers Expand Their Appetite for U.S. Treasuries

Goldman Warns OPEC Faces Test as Spectre of U.S. Shale Looms

Trump Blasts ‘Very Bad’ German Carmakers Over U.S. Sales

‘Mnuchin Rule’ Against Wealthy Tax Cuts Comes Back to Bite Him

Retailers Cheer GOP Retreat on Ending Debit Card Fees Limit

Pretty Soon Electric Cars Will Cost Less Than Gasoline

GM Accused in Owner Lawsuit of Using VW-Like Defeat Devices

Microsoft to Buy Cyber Security Firm Hexadite for $100 Million

Where Nestlé Guzzles Water, Michigan Neighors Take Exception

This Secretive Billionaire Makes The Cheese For Pizza Hut, Domino’s And Papa John’s

Judge Orders UPS to Pay $247 Million for Illegally Shipping Cigarettes

Advanced Micro Devices, Inc.: The Worst Performing Stock In The S&P 500

Cullen Roche: In Defense of Vanguard

Jeff Miller: A Fresh Look at Healthcare and Biotech

Be sure to follow me on Twitter.

-

Morning News: May 25, 2017

Posted by Eddy Elfenbein on May 25th, 2017 at 7:05 amOPEC Poised for ‘Safe Bet’ of Nine-Month Extension of Oil Cuts

4 Reasons Why Moody’s Is Wrong About China

Bitcoin Is Up Over 400% In The Past Year—What’s Stopping It From Going Mainstream?

Trump’s Toxic Budget Is a Cheap Win With the Right People

Fed Sounds Cautious Note But Doesn’t Deter Forecast of Rate Increase

Why Wall Street Is Betting on Ford’s New CEO

SoftBank Reportedly Amasses $4 Billion Stake in NVIDIA

Facebook Signs BuzzFeed, Vox, Others For Original Video Shows

Sears Posts First Quarterly Profit in Nearly Two Years on Cost Cuts

Google’s A.I. Program Rattles Chinese Go Master as It Wins Match

Teenagers Everywhere Don’t Understand Money

Howard Lindzon: Body Slamming the Bears…

Josh Brown: What We’re Telling Clients About European Stocks

Be sure to follow me on Twitter.

-

Morning News: May 24, 2017

Posted by Eddy Elfenbein on May 24th, 2017 at 6:51 amOPEC, Non-OPEC Hold Informal Talks To Nail New Oil Cuts

Moody’s Downgrades China Credit Ratings For First Time in 30 Years As Debt Mounts

Net Neutrality Ideals Are Already Dead

Obama’s Fiduciary Rule, After a Delay, Will Go Into Effect

The U.S. Wins the G7 Unemployment-Improvement Race

Trump’s Path to a Balanced Budget Paved With Accounting Gimmicks

Economists See Little Magic in Tax Cuts to Promote Growth

Fiat Chrysler Stumbles Into U.S. Regulatory Crosshairs Again

Biggest Threat to Ford? Not GM, but Silicon Valley

Amazon Sets Up Shop in the Heart of the Publishing Industry

Uber to Repay Millions to Drivers, Who Could Be Owed Far More

Startup Carmaker Faraday Future Says It’s Unaffected By Job Cuts At Partner LeEco

‘Food Revolution’: Megabrands Turn To Small Start-Ups For Big Ideas

Ben Carlson: Barriers to Entry in the Markets

Jeff Carter: Risk and Startups

Be sure to follow me on Twitter.

-

HEICO Earns 53 Cents per Share

Posted by Eddy Elfenbein on May 23rd, 2017 at 5:34 pmAfter the bell, HEICO (HEI) reported fiscal Q2 earnings of 53 cents per share. That was three cents better than Wall Street’s estimate. The details look pretty good. Net sales rose 5% to $368.7 million. For the first half of the year, net sales are up 8%. I was pleased to see HEICO’s operating margin edge up from 19% a year ago to 20.8% for this year’s Q2.

Laurans A. Mendelson, HEICO’s Chairman and CEO, commented on the Company’s second quarter results stating, “We are very pleased to report record quarterly results in consolidated net sales, operating income and net income driven by record net sales and operating income at both operating segments. Our outstanding performance principally reflects increased demand and operating efficiencies within both of our operating segments, as well as the excellent performance of our well managed and profitable fiscal 2016 acquisition.

Best of all, HEICO raised their full-year guidance. This was the second increase this year. Unfortunately, the company doesn’t guide for EPS, but they do for a few other metrics.

HEICO now sees net sales rising this year by 8% to 10%. The previous forecast was 6% to 8%. For net income, HEICO projects growth of 12% to 14%, up from 9% to 11%. HEICO also projects cash flow from operations of $270 million. That’s up $10 million from the previous forecast.

Last year, HEICO earned $1.86 per share last year. If we assume no change in shares outstanding, that implies 2017 EPS of $2.08 to $2.12. Wall Street had been expecting $2.05 per share.

-

The Rebound in Cognizant

Posted by Eddy Elfenbein on May 23rd, 2017 at 3:07 pmOne of the lessons of investing is that periodically, the market freaks out. Sometime the reasons are good, many times, they’re not.

Last September, shares of Cognizant Technology Solutions (CTSH) plunged after the company said that an internal investigation revealed that the company may have violated the U.S. Foreign Corrupt Practices Act. Cognizant notified the SEC and DOJ. The same day, the company’s president resigned.

That day, the stock got crushed. At one point, CTSH dropped down to $45.44, which was a loss of 17.4% for the day. By the closing bell, the stock had shed 13.3%.

We waited the mess out, and today CTSH is at a new 52-week high. Today’s high was $66.30 per share.

To quote Warren Buffett, “the stock market is designed to transfer money from the active to the patient.”

-

Morning News: May 23, 2017

Posted by Eddy Elfenbein on May 23rd, 2017 at 7:11 amOPEC on Verge of 9-Month Cuts Extension After Iraq Gives Backing

Merkel’s Weak-Euro Complaint Has Two Goals

Greek Deal on Debt Relief Founders as Talks Stretch to June

Supreme Court Limits Locations of Patent Lawsuits

The Case That Could Doom Elizabeth Warren’s Wall Street Watchdog

CEOs Of Target, ADM To Square Off On U.S. Border Tax At Hearing

Ford Taps Former Office Furniture Executive To Be New CEO

Here’s Why Tesla’s Elon Musk Just Called Himself an ‘Idiot’ on Twitter

Puma Biotech Shares Are Roaring On An FDA Review. Here’s What Could Still Go Wrong

The Future of Whole Foods Isn’t About Groceries

Apple and Nokia Settle Patent Dispute And Sign New Deal

Even Harley-Davidson Can’t Resist the Tug of Overseas Factories

Cullen Roche: Why I Am An Optimist

Roger Nusbaum: Political Volatility Catches Up To Markets (Kind Of)

Be sure to follow me on Twitter.

-

The Quants Are Taking Over

Posted by Eddy Elfenbein on May 22nd, 2017 at 3:43 pmThe WSJ runs a story today on the emergence of quant funds:

Up and down Wall Street, algorithmic-driven trading and the quants who use sophisticated statistical models to find attractive trades are taking over the investment world.

On many trading floors, quants are gaining respect, clout and money as investment firms scramble to hire mathematicians and scientists. Traditional trading strategies, such as sifting through balance sheets and talking to companies’ customers, are falling down the pecking order.

“A decade ago, the brightest graduates all wanted to be traders at Wall Street investment banks, but now they’re climbing over each other to get into quant funds,” says Anthony Lawler, who helps run quantitative investing at GAM Holding AG . The Swiss money manager last year bought British quant firm Cantab Capital Partners for at least $217 million to help it expand into computer-powered funds.

Guggenheim Partners LLC built what it calls a “supercomputing cluster” for $1 million at the Lawrence Berkeley National Laboratory in California to help crunch numbers for Guggenheim’s quant investment funds, says Marcos Lopez de Prado, a Guggenheim senior managing director. Electricity for the computers costs another $1 million a year.

Algorithmic trading has been around for a long time but was tiny. An article in The Wall Street Journal in 1974 featured quant pioneer Ed Thorp. In 1988, the Journal profiled a little-known Chicago options-trading firm that had a secret computer system. Journal reporter Scott Patterson wrote a best-selling book in 2010 about the rise of quants.

Prognosticators imagined a time when data-driven traders who live by algorithms rather than instincts would become the kings of Wall Street.

That day has arrived. In just one sign of their power, quantitative hedge funds are now responsible for 27% of all U.S. stock trades by investors, up from 14% in 2013, according to the Tabb Group, a research and consulting firm in New York.

Quants have almost caught up to individual investors, which outnumber quants and collectively have 29% of all stock-trading volume.

At the end of the first quarter, quant-focused hedge funds held $932 billion of investments, or more than 30% of all hedge-fund assets, estimates HFR Inc. In 2009, quant funds held $408 billion, or 25% of all hedge-fund assets.

Quants got $4.6 billion of net new investments in the first quarter, while the overall hedge-fund business saw withdrawals of $5.5 billion.

The computers are outperforming humans at picking investments. In the past five years, quant-focused hedge funds gained about 5.1% a year on average. The average hedge fund rose 4.3% a year in the same period.

This is a good article and I recommend you give it a read. My only quibble, and it’s a small one, is that it seems late by about ten years. These trends have been building for a long time.

-

New High Today for Stryker

Posted by Eddy Elfenbein on May 22nd, 2017 at 2:21 pmI noticed that Stryker (SYK) is at a new all-time high today. I added the stock to the Buy List in 2008. It promptly crashed with the bear market and underperformed for more than four years. We held on and have done quite well. Good investing takes patience.

-

Incentives Matter

Posted by Eddy Elfenbein on May 22nd, 2017 at 12:01 pmJosh Brown noticed that Steven Russolillo is winding down the WSJ‘s stock-picking column. Why? Simply put, hunting for cheap stocks has become a dying art.

Josh sees this as part of a long-term decline for active investing, and he highlights AllianceBernstein’s new incentive-based pay structure for active managers.

Later on, Josh talks about my venture into exchange-traded funds:

I gave some money to my old friend Eddy Elfenbein when his Crossing Wall Street ETF launched last fall. He did well and I will probably give him some more.

He’s got the first actively-managed ETF with a variable management fee built into it (his product was launched through Noah Hamman’s AdvisorShares fund family). He’s doing between 20 and 30 of his favorite stocks, which will either be very good or very bad in different market environments. But overall, he’s not snuggling up to the Russell 3000 or the S&P 500. I have no way of knowing whether or not what he’s trying to do will work, I only know that it won’t look exactly like an index fund I can buy for approximately zero dollars.

Here’s Voss and Howard again on concentration:

Studies show that buy-side analysts are quite good at security selection: Take, for example, the high levels of accretive alpha of their highest conviction/largest positions, as measured by ex-ante relative portfolio weights. Moving down the relative weights, performance worsens, with holdings beyond the top 20 generating negative alpha. In other words, most portfolios are overdiversified and research shows that hurts performance.

What’s interesting is that, because Eddy doesn’t focus on the benchmark in terms of how he talks about his approach, I have never even once looked at CWS’s performance against it, only absolutely. There’s a benefit to this sort of reframing that I should probably think more deeply about.

There should be more attempts at innovation like what we’re seeing from Eddy and AB. Something will eventually click.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His